Sector Research Observatory

Autos Weekly

March 09, 2026

"Covering the world's top automakers, from Detroit to Shenzhen."

Week in Review

Chinese EV Giants Gain Edge as Western Rivals Stumble

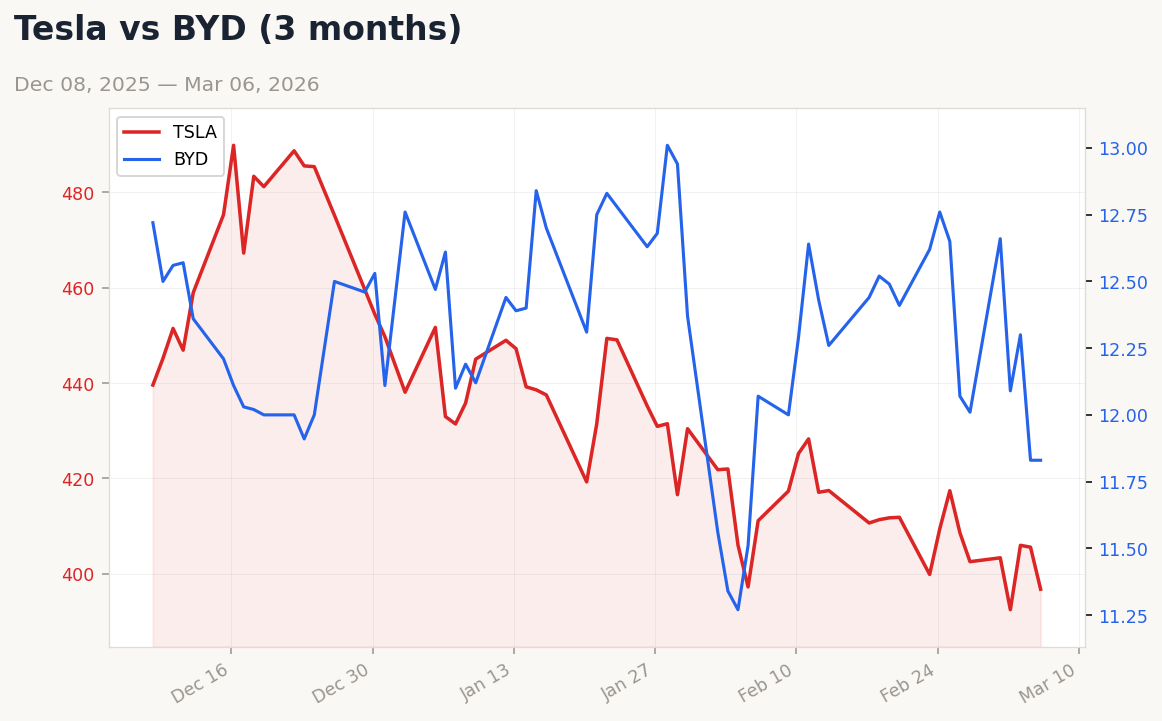

The automotive sector faced headwinds this week, with Tesla ($TSLA) shedding 2.17% to close at $396.73, reflecting broader concerns over slowing EV demand in Western markets. Chinese EV players, however, bucked the trend, with XPeng ($XPEV) surging 6.00% to $17.32 and Li Auto ($LI) gaining 1.66% to $17.16, fueled by a Rhodium Group report highlighting their structural cost advantages over Western automakers (CNBC). This disparity underscores a growing competitive gap, as Chinese firms leverage localized supply chains and aggressive overseas expansion into markets like Mexico and Brazil (GlobeNewswire).

Market Snapshot

Auto Industry Leaders & Key Commodities

| Company / Asset | Level | Change | Ticker |

|---|---|---|---|

| US & European OEMs | |||

| Tesla | 396.73 | -2.17% | $TSLA |

| Ford | 12.15 | -1.54% | $F |

| General Motors | 75.21 | -1.07% | $GM |

| Stellantis | 7.15 | -1.65% | $STLA |

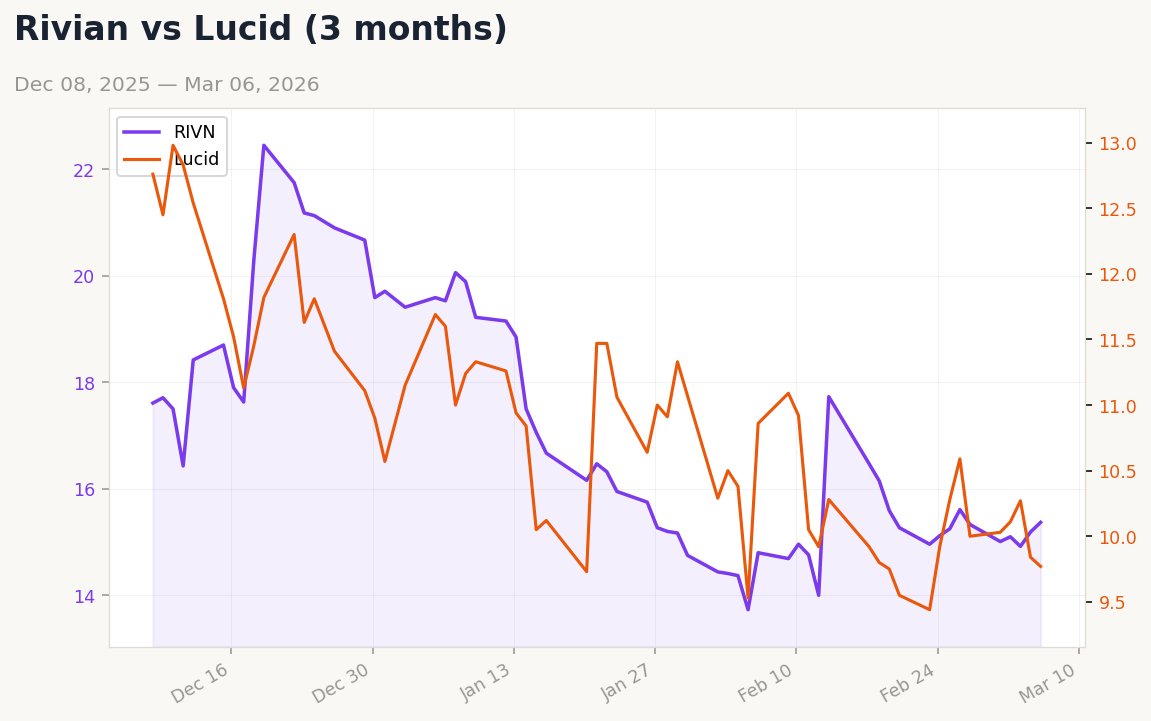

| Rivian | 15.37 | +1.18% | $RIVN |

| Lucid | 9.77 | -0.71% | $LCID |

| Asian OEMs | |||

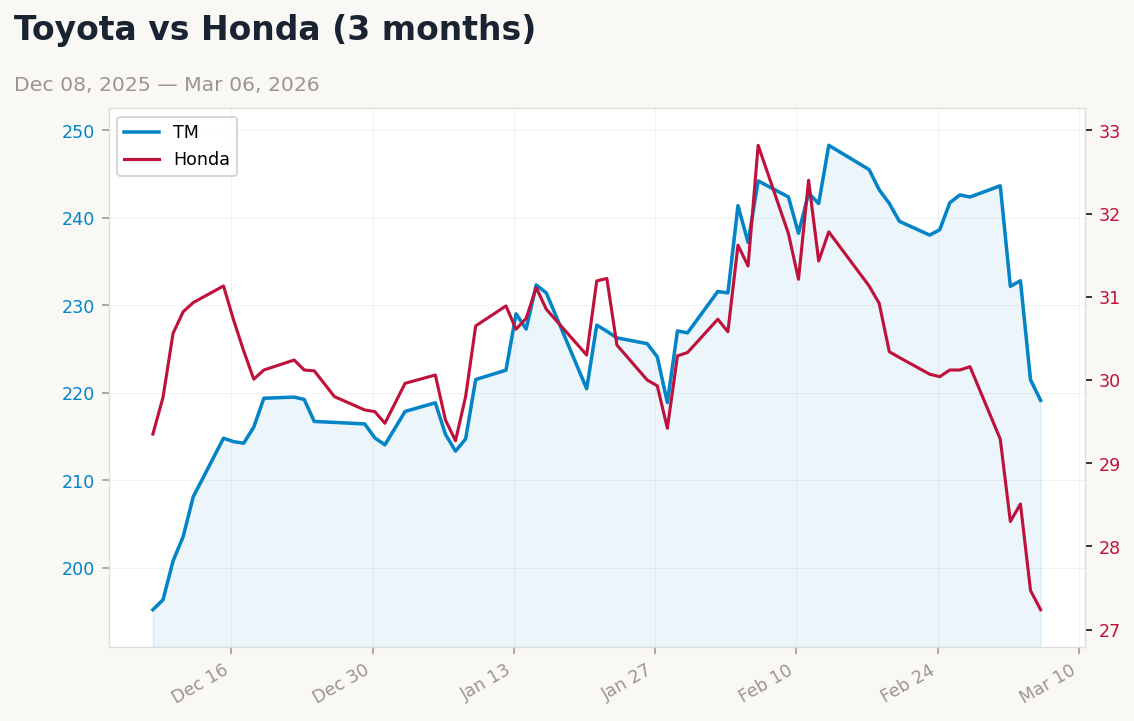

| Toyota | 219.14 | -1.06% | $TM |

| Honda | 27.24 | -0.84% | $HMC |

| BYD | 11.83 | +0.00% | $BYDDY |

| NIO | 4.78 | +1.27% | $NIO |

| XPeng | 17.32 | +6.00% | $XPEV |

| Li Auto | 17.16 | +1.66% | $LI |

| Supply Chain | |||

| Magna International | 58.85 | -3.37% | $MGA |

| Aptiv | 72.70 | +0.68% | $APTV |

| Commodities | |||

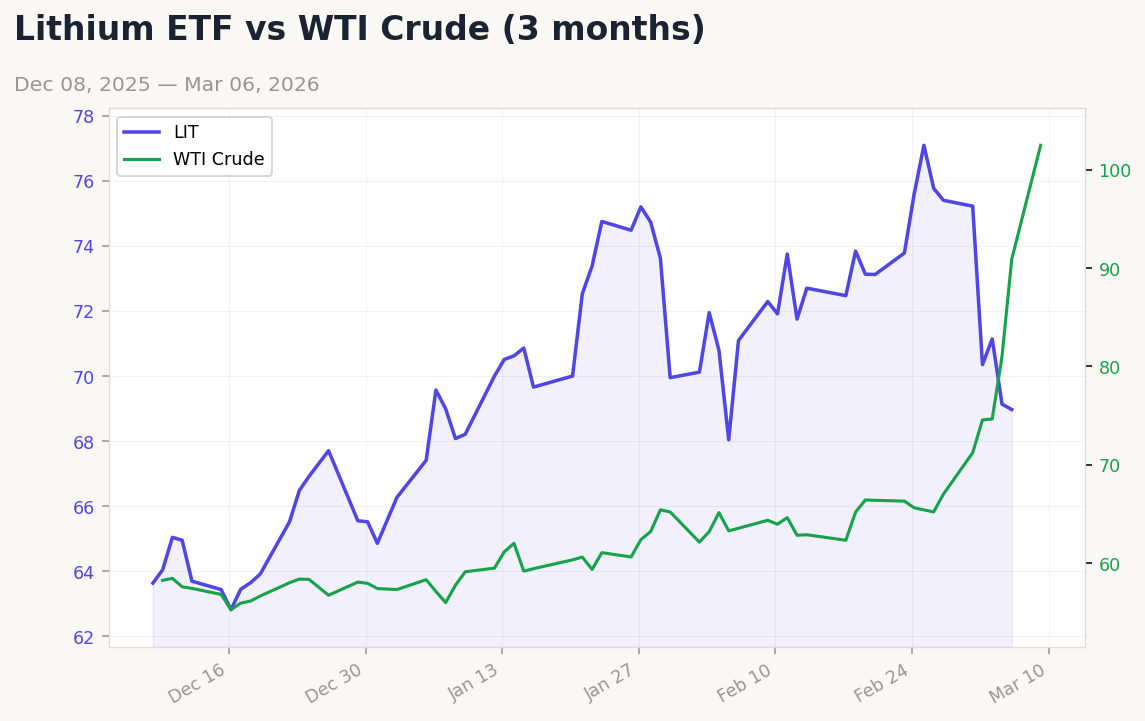

| WTI Crude | 102.46 | +12.72% | — |

| Brent Crude | 104.36 | +12.59% | — |

| Lithium ETF (LIT) | 68.97 | -0.25% | — |

Source: Market data via yfinance as of Mar 09, 2026. Tickers for reference only.

Spotlight Read

Chinese EV Makers Outpace Western Rivals with Cost Advantages

Chinese electric vehicle manufacturers are widening their lead over Western competitors, driven by structural cost efficiencies rather than just state subsidies, per a Rhodium Group report (CNBC). This advantage, seen in firms like BYD ($BYDDF) and XPeng ($XPEV), is amplified by localized supply chains and aggressive global expansion into emerging markets. With stock gains this week—XPeng up 6.00%—investors are taking note. This trend could pressure legacy automakers like Ford ($F) and GM ($GM) to rethink outsourcing strategies, potentially reshaping global market dynamics.

Latest Industry News

Ford Cancels F-150 Lightning, Triggers Layoffs at SK Battery

Ford ($F) axed its all-electric F-150 Lightning, leading to nearly 1,000 layoffs at SK Battery’s Georgia plant in the U.S. (Fortune). This move signals a retreat from EV ambitions amid policy shifts.

Source: Fortune

Chinese OEMs Accelerate Overseas Production Capacity

Chinese automakers are ramping up global production, targeting markets like Mexico and Brazil, with supply chains expanding alongside (GlobeNewswire). BYD ($BYDDF) stands to gain from this strategic push.

Source: GlobeNewswire

BMW Models Sweep Prestigious Awards in Europe

BMW ($BMWYY) secured multiple top awards for its model series in Germany and the UK, bolstering its premium brand strength (Bmwgroup.com). This reinforces its competitive edge in Europe.

Source: Bmwgroup.com

Auto Component Industry Growth Outpaces OEMs in India

India’s auto component sector is projected to grow 8-10% in FY27, driven by exports and localization, outpacing the broader auto sector’s 5-8% (BusinessLine). This benefits suppliers like Magna ($MGA).

Source: BusinessLine

EVgo Posts Record Q4 Revenue Growth in U.S.

EVgo Inc. reported a 75% revenue increase for Q4 2025, with charging network revenue hitting $64 million, signaling strong U.S. infrastructure demand (Financial Post).

Source: Financial Post

Software-Defined Vehicles Gain Traction with Eclipse SDV

The Eclipse Foundation’s Software-Defined Vehicle (SDV) initiative is revolutionizing open-source automotive tech, impacting firms like Aptiv ($APTV) with new architectures (Redmonk.com).

Source: Redmonk.com

Automotive Ethernet Market Set for $10.5B Growth

The global automotive Ethernet market is projected to exceed $10.5 billion by 2032, driven by software-defined architectures and supply chain diversification (GlobeNewswire). NXP ($NXPI) could see gains.

Source: GlobeNewswire

Intelligent Fragrance Systems to Hit 4M Units by 2030

China’s automotive fragrance market is poised for growth, with intelligent systems expected to surpass 4 million units by 2030, enhancing cockpit experiences (GlobeNewswire).

Source: GlobeNewswire

EV & Battery Watch

Electric Vehicle & Battery Technology Developments

Electric vehicle adoption continues to rise globally, though regional disparities persist. In Asia, China leads with robust sales growth, bolstered by companies like BYD ($BYDDF) and NIO ($NIO), which saw a 1.27% stock uptick to $4.78 this week, driven by localized supply chains (seekingalpha.com). In the Americas, however, policy rollbacks under the Trump Administration have led to cancellations like Ford’s ($F) F-150 Lightning, slowing EV momentum (Fortune). Meanwhile, in Europe, regulatory mandates for zero-emission vehicles sustain demand, pushing firms like Volkswagen ($VWAGY) to invest in battery tech despite market softness (GlobeNewswire).

Supply Chain & Trade

Global Supply Chain & Trade Policy

Semiconductor and battery material supply chains remain under strain, with geopolitical tensions in West Asia disrupting cargo flows and prompting exporters to withdraw shipments from key Indian ports (BusinessLine). In Europe, firms like Infineon ($IFNNY) and NXP ($NXPI) are navigating chip shortages by diversifying sourcing, while automotive Ethernet solutions gain traction as a $10.5 billion market by 2032 (GlobeNewswire). Trade policies, including potential tariffs in the U.S., could further complicate supply dynamics for automakers like Stellantis ($STLA), reliant on global networks.

Data Observatory

Auto Sector Charts

Week Ahead

Key Events for the Auto Sector

Investors should monitor upcoming earnings from key players like Toyota ($TM) and Hyundai-Kia, expected to provide insights into Asian market resilience amid rising oil costs. In Europe, regulatory updates on zero-emission mandates could impact Volkswagen ($VWAGY) and BMW ($BMWYY), with potential fines or incentives at stake. The Geneva International Motor Show, kicking off next week, will also showcase new EV models and tech from Tesla ($TSLA) and Rivian ($RIVN), offering a glimpse into competitive positioning.

Subscribe to Autos Weekly and get each new issue delivered to your inbox.

Already a member? Visit robomacro.com to log in and manage subscriptions, or use Forgot Password to set a password.