Sector Research Observatory

Autos Weekly

June 22, 2026

"Covering the world's top automakers, from Detroit to Shenzhen."

Week in Review

China EV Pressure Squeezes Europe Carmakers

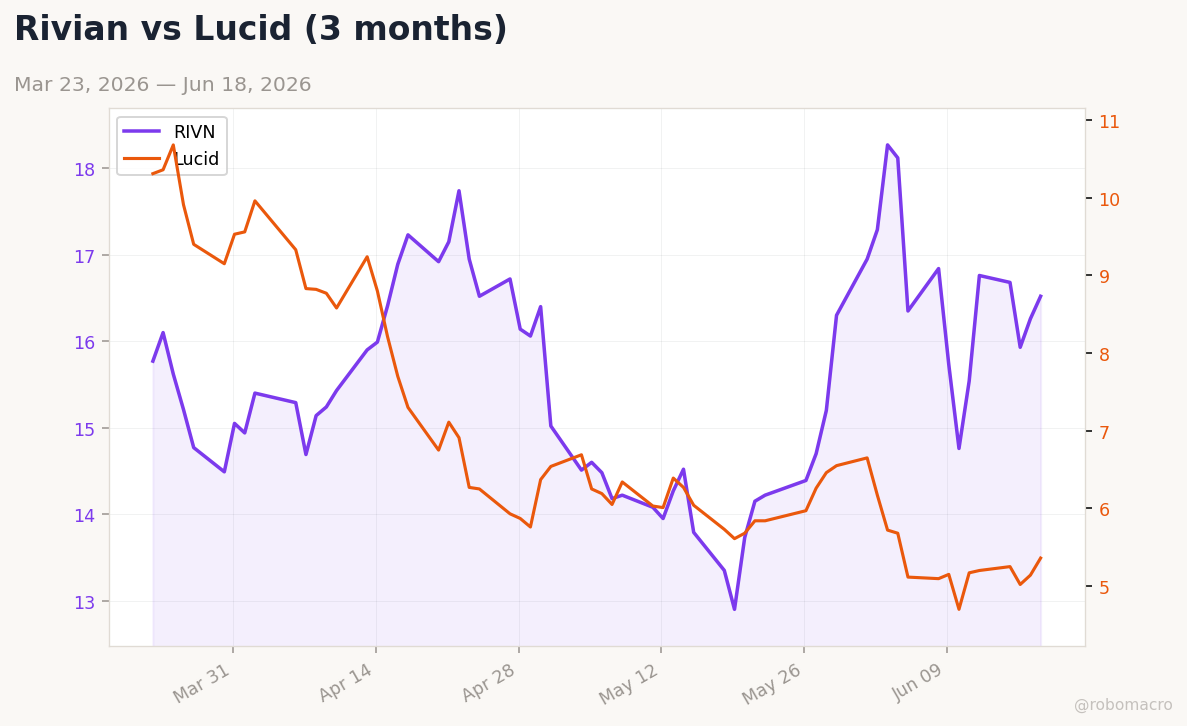

European automakers faced acute pressure this week as Chinese EV competition intensified, with BMW cutting its full-year automotive EBIT margin guidance to 1-3% from 4-6% amid accelerating China market decline. The move aligns with broader sector weakness, as Stellantis fell 2.01% to $6.34 while GM slipped 0.36% to $79.29; in contrast, U.S. EV names showed resilience with Lucid surging 4.28% to $5.36 and Rivian rising 1.60% to $16.52. Trade tensions added weight after German Chancellor Friedrich Merz signaled action on the €360B deficit with China.

Market Snapshot

Auto Industry Leaders & Key Commodities

| Company / Asset | Level | Change | Ticker |

|---|---|---|---|

| US & European OEMs | |||

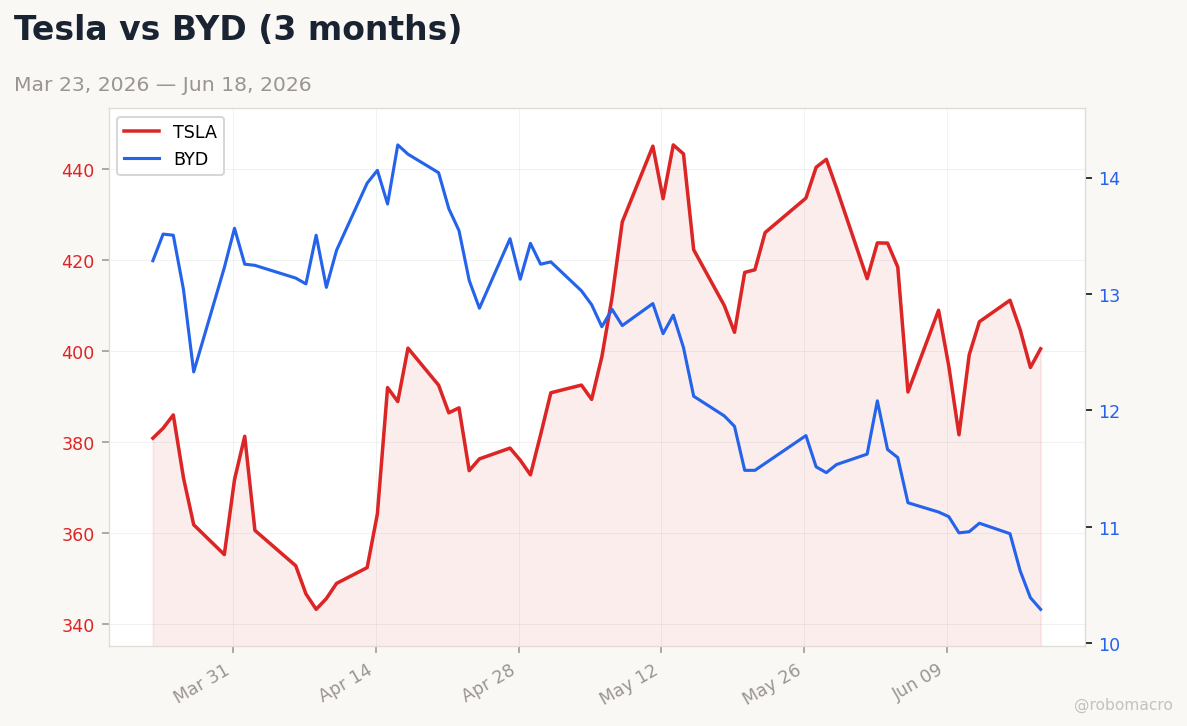

| Tesla | 400.49 | +1.04% | $TSLA |

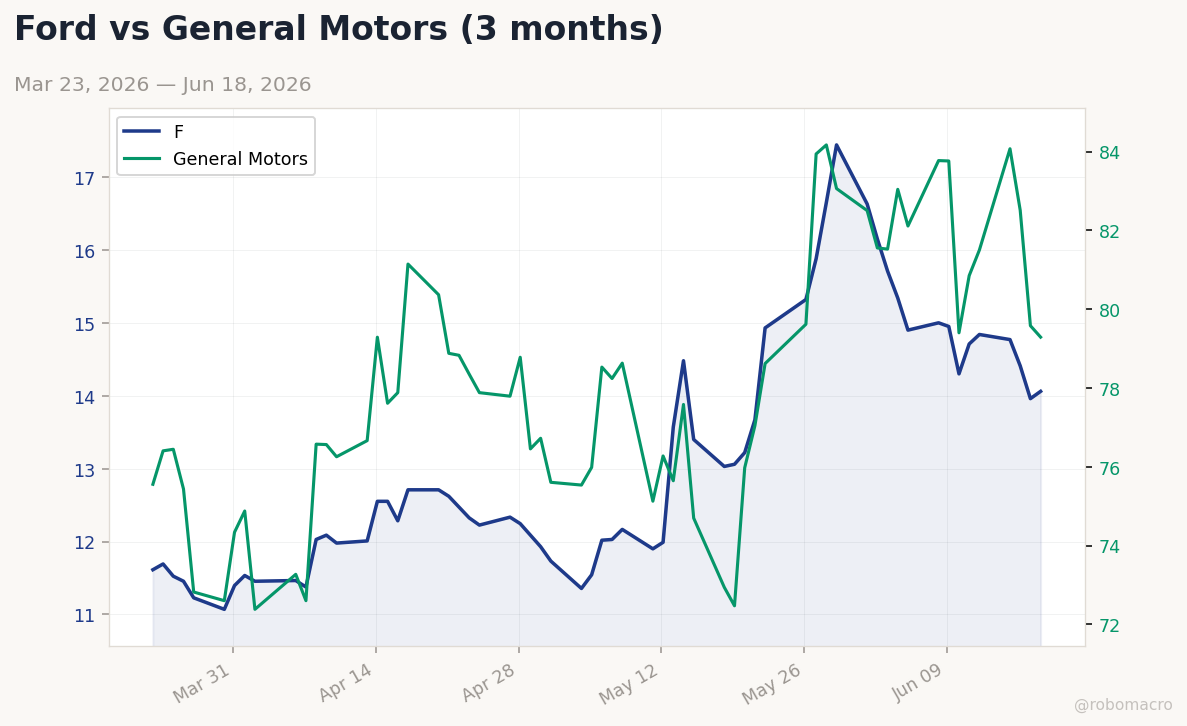

| Ford | 14.06 | +0.72% | $F |

| General Motors | 79.29 | -0.36% | $GM |

| Stellantis | 6.34 | -2.01% | $STLA |

| Rivian | 16.52 | +1.60% | $RIVN |

| Lucid | 5.36 | +4.28% | $LCID |

| Asian OEMs | |||

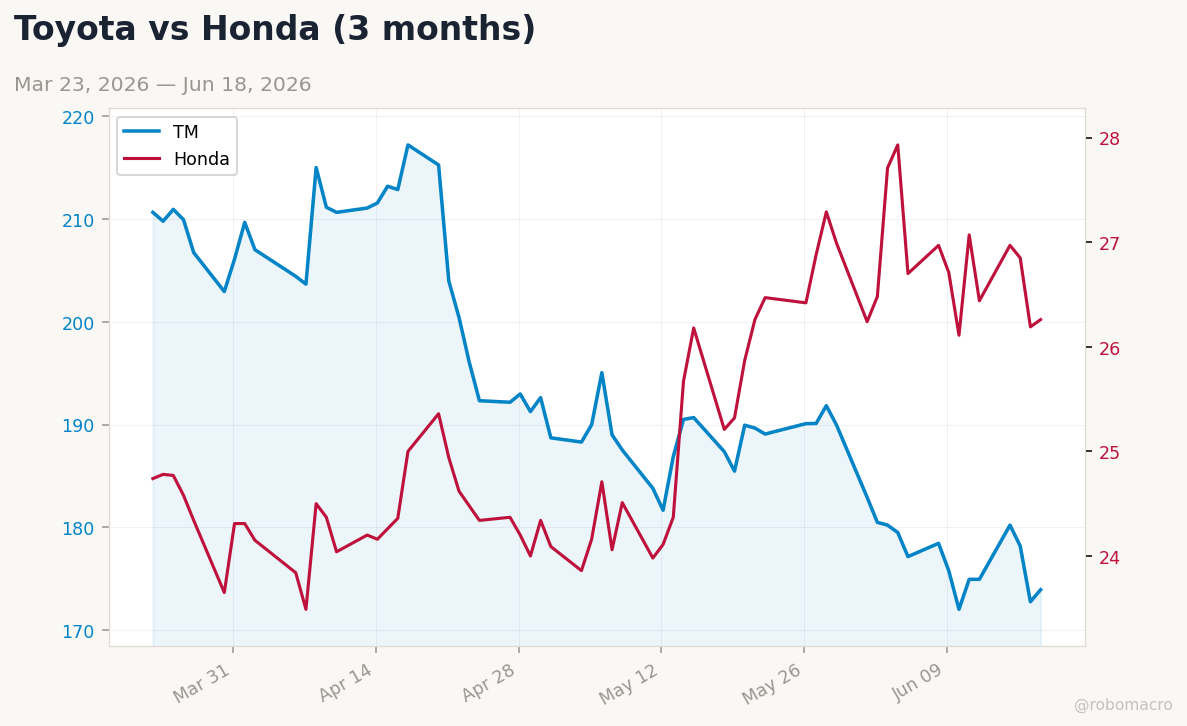

| Toyota | 173.94 | +0.68% | $TM |

| Honda | 26.26 | +0.27% | $HMC |

| BYD | 10.29 | -0.96% | $BYDDY |

| NIO | 5.02 | -0.59% | $NIO |

| XPeng | 13.21 | -1.71% | $XPEV |

| Li Auto | 13.21 | -2.72% | $LI |

| Supply Chain | |||

| Magna International | 65.35 | +0.71% | $MGA |

| Aptiv | 63.68 | +1.29% | $APTV |

| Commodities | |||

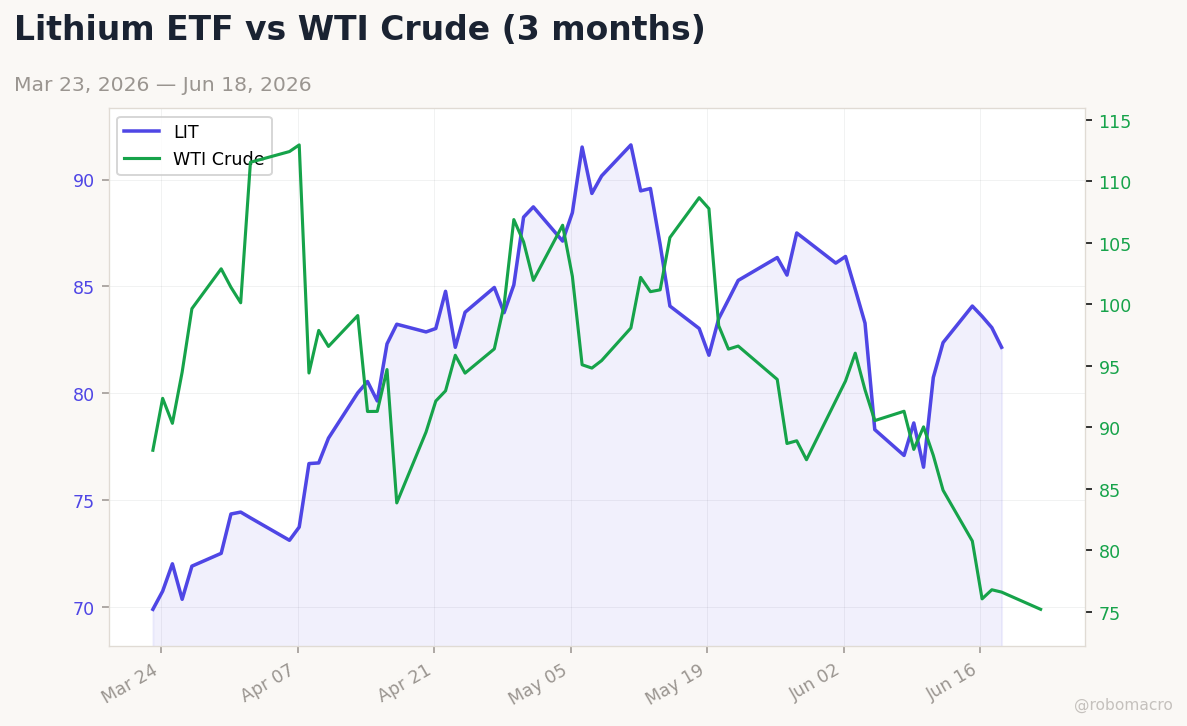

| WTI Crude | 75.10 | -1.96% | — |

| Brent Crude | 78.98 | -1.09% | — |

| Lithium ETF (LIT) | 82.15 | -1.11% | — |

Source: Market data via yfinance as of Jun 22, 2026. Tickers for reference only.

Spotlight Read

BMW Slashes Profit Outlook as China EV Rivals Intensify

BMW lowered its 2026 automotive EBIT margin target to 1-3% from 4-6%, citing rapid share loss in China to domestic EV makers. The revision underscores margin compression across European OEMs exposed to the world’s largest EV market. Investors will monitor whether cost cuts and new model launches can offset volume declines through year-end.

Latest Industry News

Ford Rolls Out Daily Engine Teardowns at All Plants

The program targets early defect detection to reduce recalls and improve quality metrics across Ford’s global manufacturing footprint. $F shares rose 0.72% to $14.06.

Source: Ibtimes.com.au

Reliance Triples Battery Ambition to 120 GWh

Backed by its oil-to-chemicals cash flow, Reliance is scaling cell production aggressively in India to capture domestic EV demand. The move positions the conglomerate as a major Asian battery supplier.

Source: BusinessLine

Tariffs Could Add $3,000 to North American Car Prices

Proposed U.S. tariffs on Canada and Mexico threaten integrated supply chains and raise vehicle costs for $GM, $F and Stellantis. Analysts flag margin and demand risks if enacted.

Source: financialpost.com

Pentagon Adds BYD to Chinese Military Companies List

Inclusion of $BYD alongside Alibaba and Baidu on the 1260H list raises compliance hurdles for U.S. investors and partners. $BYD shares fell 0.96% to $10.29.

Source: The Next Web

Tesla Submits Cybercab Certification Data to EPA

Documents reveal updated specs for the robotaxi while full autonomy timelines remain unclear. $TSLA gained 1.04% to $400.49 amid ongoing autonomy focus.

Source: New Atlas

Malaysia Urged to Move Up Auto Value Chain

Industry leaders called for greater technology development and regional solutions beyond assembly roles. The shift targets Southeast Asian growth amid evolving mobility demands.

Source: Paul Tan's Automotive News

German Auto Lobby Welcomes EU-US Trade Deal Approval

European Parliament backing provides clarity for German exporters, though tariffs continue to weigh on $BMW and Mercedes-Benz operations. Supply chain realignment remains a priority.

Source: Yahoo Entertainment

India to Launch Star Rating System for E-Two-Wheelers

The efficiency labeling aims to guide buyers and lower charging costs, supporting faster adoption of electric two-wheelers in the world’s third-largest auto market.

Source: Livemint

EV & Battery Watch

Electric Vehicle & Battery Technology Developments

Reliance Industries expanded its battery roadmap to 120 GWh, leveraging cash flow from its oil-to-chemicals business to fund gigafactory-style capacity in India. The move directly challenges Asian incumbents such as $CATL and $LG Energy Solution while supporting domestic EV makers including Tata Motors. Lower lithium prices, reflected in the LIT ETF’s 1.11% decline, could accelerate cell cost reductions and improve economics for new entrants.

Supply Chain & Trade

Global Supply Chain & Trade Policy

U.S. tariff threats on Canada and Mexico could raise vehicle costs by up to $3,000 and disrupt integrated North American production for $GM, $F and Stellantis. The measures coincide with the Pentagon’s addition of $BYD to its Chinese military companies list, complicating sourcing strategies for battery and component buyers. European firms are simultaneously navigating €360B trade imbalances with China that may trigger further policy responses.

Data Observatory

Auto Sector Charts

Week Ahead

Key Events for the Auto Sector

Market participants will track U.S. consumer confidence and manufacturing PMI releases for signs of demand resilience amid tariff uncertainty. European earnings from remaining German OEMs could reveal further China-related revisions, while India’s upcoming policy updates on EV incentives may influence $TATAMOTORS and Reliance execution timelines.

Subscribe to Autos Weekly and get each new issue delivered to your inbox.

Already a member? Visit robomacro.com to log in and manage subscriptions, or use Forgot Password to set a password.