ANZ Macro Daily(Beta Mode)

RBA Speeches Ahead, AUD Dips

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 9,200.90 | +0.03% |

| NZX 50 | 13,656.65 | -0.48% |

| AUD/USD | 0.71 | -0.16% |

| NZD/USD | 0.59 | -0.59% |

| AUD/NZD | 1.19 | +0.09% |

| BHP | 58.41 | +1.14% |

| Gold | 5,352.90 | +2.34% |

| Brent Crude | 79.28 | +9.38% |

| Bitcoin | 69,342.98 | +5.48% |

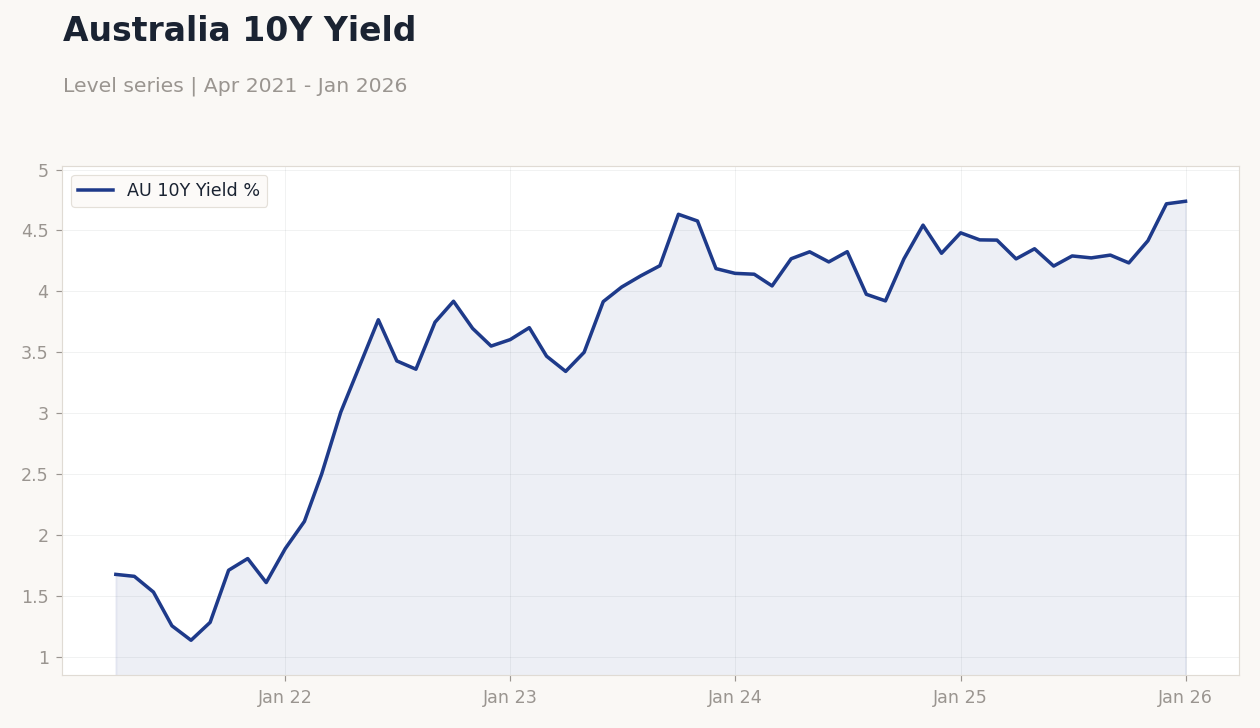

| Australia 10Y Govt Yield | 4.74% | +0.45% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| RBA Hunter Speech | - | - | - |

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| RBA Bullock Speech | - | - | 11:10 |

| Building Permits Month-over-Month Prel | -14.90 | 5.50 | 14:30 |

| Ai Group Industry Index | -12.30 | - | 12:00 |

| GDP Growth Quarter-over-Quarter | 0.40 | 0.60 | 14:30 |

| GDP Growth Year-over-Year | 2.10 | 2.10 | 14:30 |

| Trade Balance | 3,373m | 3,900m | 14:30 |

| RBA Hauser Speech | - | - | 08:30 |

- ASX 200 edges up slightly while NZX 50 declines amid mixed sentiment and commodity swings.

- AUD/USD and NZD/USD soften on USD strength tied to Middle East geopolitical risks.

- RBA Hunter speech underscores inflation persistence, paving way for key data and policy updates.

Yesterday's Recap

Australian equities displayed modest strength, with the ASX 200 closing at 9,200.90, up 0.03%, supported by mining sector gains including BHP at 58.41 with a 1.14% rise on commodity price increases. New Zealand's NZX 50 dropped to 13,656.65, down 0.48%, amid worries over dairy exports and broader risk aversion. Currencies faced pressure, with AUD/USD at 0.71 down 0.16% and NZD/USD at 0.59 down 0.59%, while AUD/NZD increased 0.09% to 1.19, highlighting Australia's commodity edge.

The RBA Hunter speech emphasized ongoing inflation challenges, consistent with recent rate discussions but offering no fresh signals. Australia's 10Y government yield rose to 4.74% up 0.45%, reflecting expectations of continued tight policy. New Zealand's short-term rate fell to 4.33%, down 9.60%, suggesting easing bets.

Commodities performed strongly, with gold at 5,352.90 up 2.34% and Brent crude at 79.28 up 9.38%, enhancing Australia's export prospects but heightening inflation concerns.

The Day Ahead

Attention turns to Australia's RBA Bullock speech at 11:10 ET, potentially shedding light on rate directions amid inflation talks. Building permits MoM preliminary at 14:30 ET is consensus 5.5% versus -14.9% previous, indicating housing trends. Tomorrow features Ai Group Industry Index at 12:00 ET, prior -12.3, gauging manufacturing.

High-impact GDP QoQ at 14:30 ET is expected at 0.6% against 0.4% prior, vital for growth assessment. GDP YoY at the same time is consensus 2.1% matching previous, shaping RBA views. Upcoming includes trade balance on March 4 and RBA Hauser speech on March 6, maintaining focus on policy and trade.

Other Economic Notes

Australia's growth relies on commodity exports such as iron ore and energy, with China's demand crucial amid global volatility. New Zealand's dairy and tourism industries contend with currency depreciation and travel disruptions from Middle East issues. Housing in both nations remains rate-sensitive, with Australian markets possibly firming if permits improve.