ANZ Macro Daily(Beta Mode)

Aussie GDP Beats, Markets Mixed

Market Snapshot

| Asset | Level | Change |

|---|---|---|

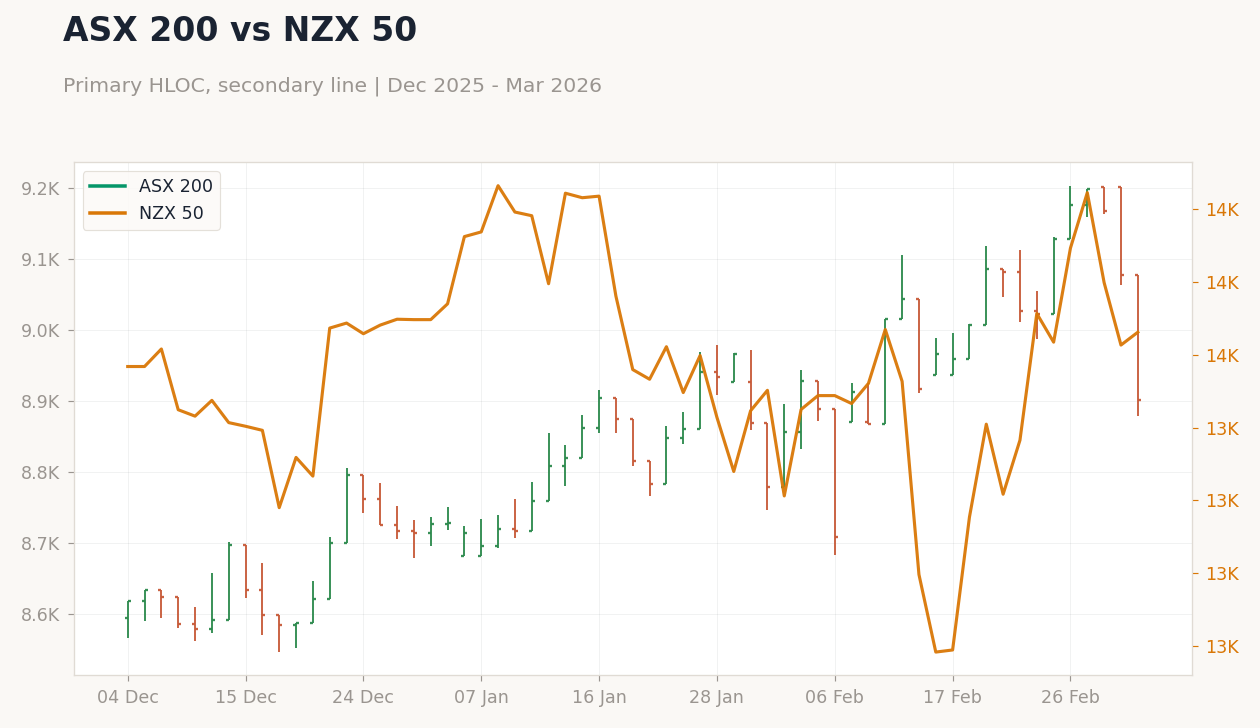

| ASX 200 | 8,901.20 | -1.94% |

| NZX 50 | 13,531.12 | +0.13% |

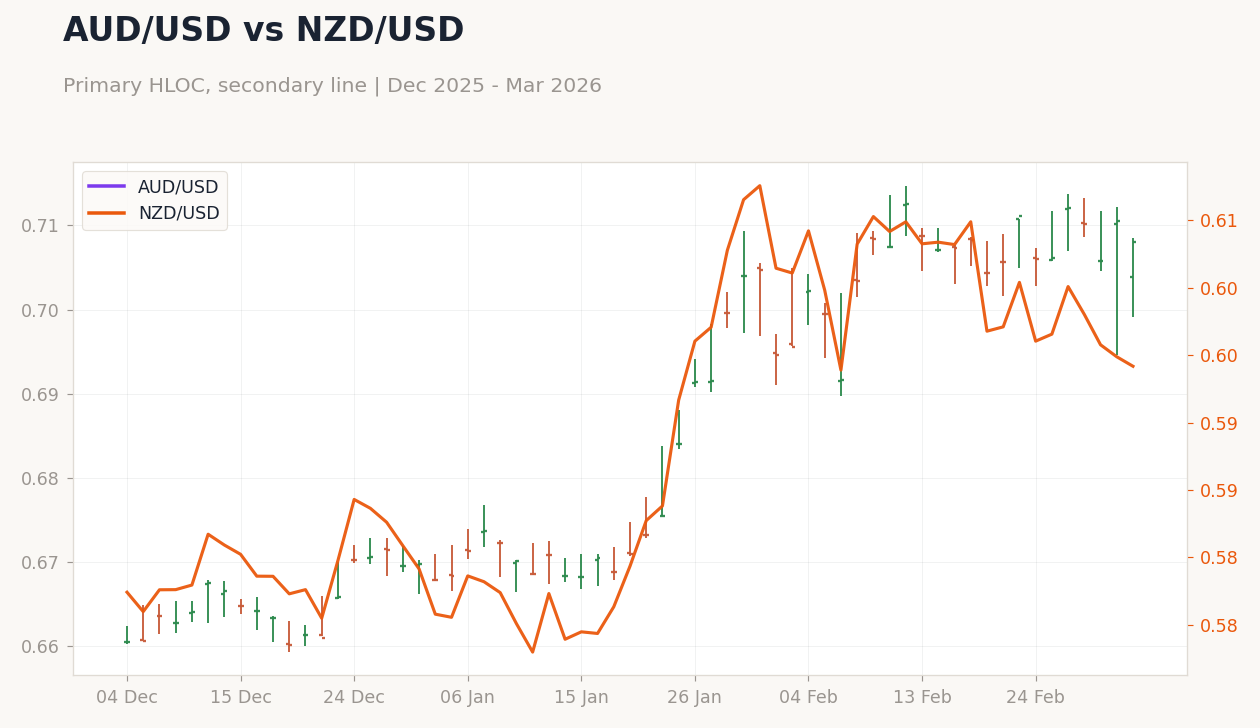

| AUD/USD | 0.71 | -0.35% |

| NZD/USD | 0.59 | -0.11% |

| AUD/NZD | 1.19 | -0.25% |

| BHP | 55.52 | -3.78% |

| Gold | 5,148.00 | +0.79% |

| Brent Crude | 81.81 | +0.50% |

| Bitcoin | 73,201.64 | +7.19% |

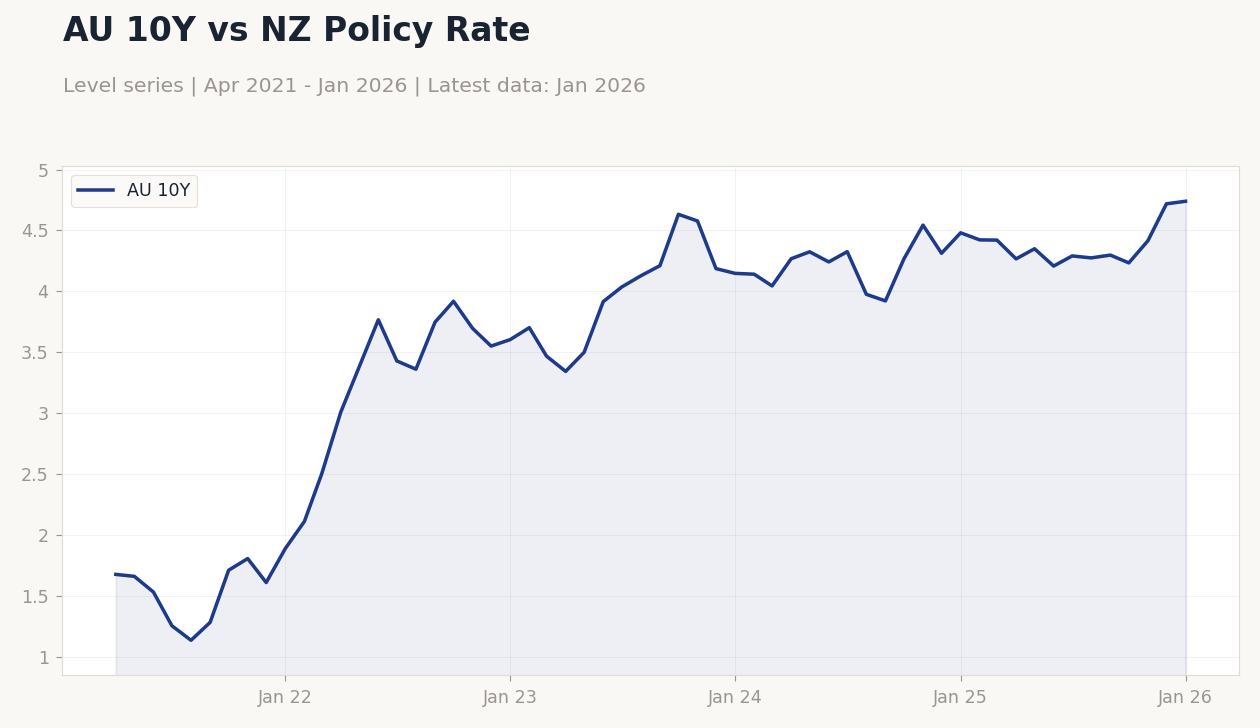

| Australia 10Y Govt Yield | 4.74% | +0.45% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| RBA Hunter Speech | - | - | - |

| RBA Bullock Speech | - | - | - |

| Building Permits Month-over-Month Prel | -14.90 | 5.50 | -7.20 |

| Ai Group Industry Index | -12.30 | - | -1.50 |

| GDP Growth Quarter-over-Quarter | 0.50 | 0.60 | 0.80 |

| GDP Growth Year-over-Year | 2.10 | 2.20 | 2.60 |

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Trade Balance | 3,373m | 3,900m | 14:30 |

| RBA Hauser Speech | - | - | 08:30 |

- Australian Q4 GDP growth exceeded expectations at 0.8% QoQ and 2.6% YoY, signaling resilient domestic demand amid global headwinds.

- Building permits in Australia fell unexpectedly by -7.2% MoM, highlighting ongoing housing sector weakness.

- ASX 200 dropped 1.94% on commodity pressures, while NZX 50 edged up 0.13% despite NZD weakness.

Yesterday's Recap

Australian economic data released yesterday showed mixed signals, with Q4 GDP growth surpassing consensus at 0.8% quarter-over-quarter (vs. 0.6% expected) and 2.6% year-over-year (vs. 2.2% expected), driven by robust household spending and exports.

However, Australia's building permits disappointed with a -7.2% month-over-month decline in the preliminary reading, against expectations of a 5.5% rise, underscoring persistent challenges in the construction sector amid high interest rates. The Ai Group Industry Index for Australia improved to -1.5 from -12.3 previously, indicating a moderation in manufacturing contraction. RBA officials, including Hunter and Bullock, delivered speeches, but no new policy signals emerged.

In New Zealand, no major data releases occurred, though the NZX 50 index rose modestly by 0.13% to 13,531.12, supported by gains in consumer sectors. Australian markets faced headwinds, with the ASX 200 falling 1.94% to 8,901.20, pressured by a 3.78% drop in BHP shares to 55.52 amid volatile iron ore prices. Currency movements were subdued, with AUD/USD slipping 0.35% to 0.71 and NZD/USD down 0.11% to 0.59, reflecting broader USD strength.

The Day Ahead

Australia's trade balance data for January is due today at 14:30 ET, with consensus expecting a surplus of AUD 3.9 billion, up from the previous AUD 3.373 billion, potentially influencing AUD sentiment amid China demand concerns. Attention will also turn to the upcoming RBA Hauser speech on March 6 at 08:30 ET, which could provide insights into the bank's inflation and growth outlook. No major New Zealand releases are scheduled for today or tomorrow, leaving markets to digest global cues.

Traders should monitor any spillover from U.S. data, as ANZ currencies remain sensitive to external risks. Overall, the focus remains on Australia's external sector, given its commodity export reliance.

Other Economic Notes

Broader ANZ economic themes highlight Australia's vulnerability to China slowdowns, with iron ore and coal exports under pressure from mixed PMI data out of Beijing. New Zealand's dairy-driven economy faces headwinds from global price softness and Middle East tensions impacting trade routes. (cont...)