ANZ Macro Daily(Beta Mode)

AU Sentiment Mixed, FX Gains Ground

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,692.60 | +1.09% |

| NZX 50 | 13,094.37 | -0.03% |

| AUD/USD | 0.71 | +2.24% |

| NZD/USD | 0.59 | +1.41% |

| AUD/NZD | 1.19 | +0.16% |

| BHP | 51.02 | +1.84% |

| Gold | 5,198.40 | +2.10% |

| Brent Crude | 88.08 | -10.99% |

| Bitcoin | 70,001.09 | +2.34% |

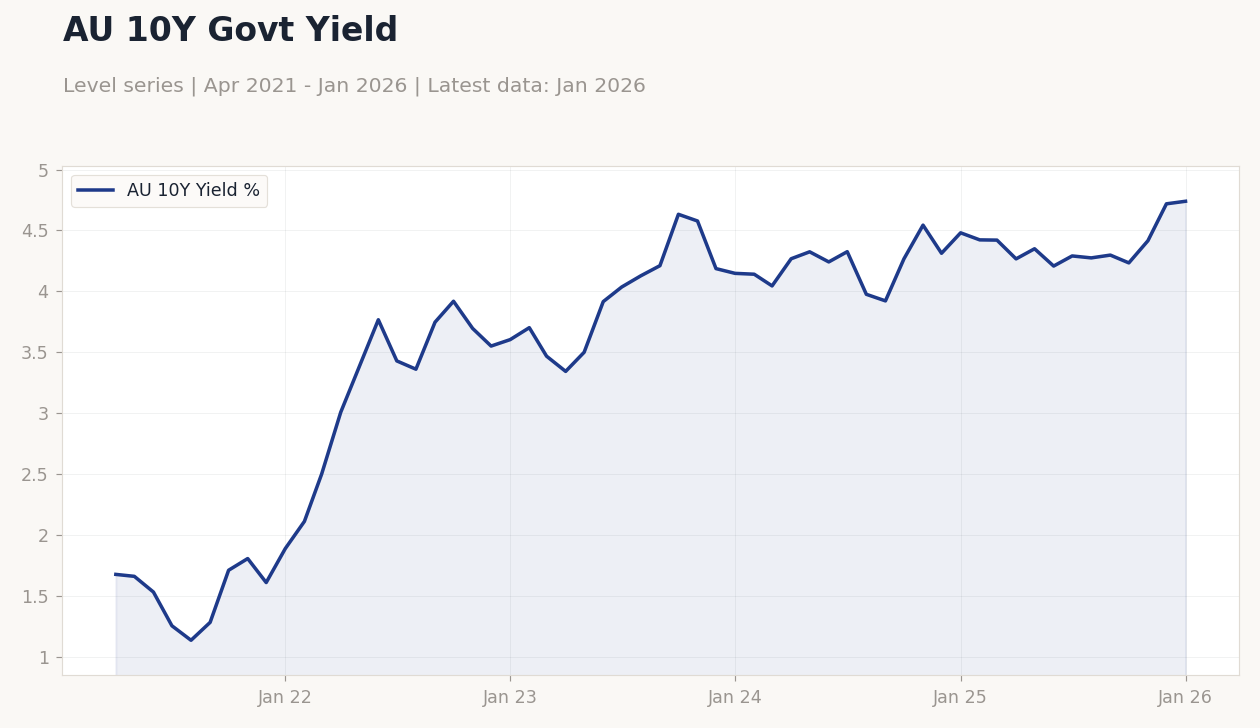

| Australia 10Y Govt Yield | 4.74% | +0.45% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Westpac Consumer Confidence Change | -2.60 | - | 1.20 |

| Westpac Consumer Confidence Index | 90.50 | - | 91.60 |

| NAB Business Confidence Index | 4 | - | -1 |

AU 10Y Govt Yield | Type: macro_line | AU 10Y Yield %: 4.74 (2026-01-01) | Range: 1.135–4.74 | Trend(6pt): 1.676,3.767,4.128,4.267,4.719,4.74

AU 10Y Govt Yield | Type: macro_line | AU 10Y Yield %: 4.74 (2026-01-01) | Range: 1.135–4.74 | Trend(6pt): 1.676,3.767,4.128,4.267,4.719,4.74

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Business NZ PMI | 55.20 | - | 13:30 |

- Australian consumer confidence improved modestly, while business sentiment softened amid global demand concerns.

- ASX 200 advanced on mining strength, NZX 50 dipped slightly; AUD and NZD rose versus USD despite risk-off news.

- RBA notes inflation drivers behind recent rate hike, potentially a one-off; NZ PMI eyed for manufacturing cues.

Yesterday's Recap

Australian data on March 9 showed mixed sentiment signals. Westpac Consumer Confidence Change rose to 1.2 from -2.6, with the Index climbing to 91.6 from 90.5, indicating slight household optimism linked to commodity price stability. However, NAB Business Confidence Index dropped to -1 from 4, highlighting worries over global demand slowdowns and China's economic outlook affecting exports like iron ore and coal.

New Zealand saw no key releases, with focus on dairy volatility and tourism trends. Equity markets varied: ASX 200 gained 1.09% to 8,692.60, led by BHP up 1.84% to 51.02 amid gold at 5,198.40 (+2.10%). NZX 50 fell -0.03% to 13,094.37, dragged by utilities and staples on softer demand.

Currencies strengthened, AUD/USD up 2.24% to 0.71 and NZD/USD +1.41% to 0.59, while AUD/NZD rose 0.16% to 1.19, reflecting Australia's export edge. Bond yields adjusted: Australia 10Y up 0.45% to 4.74%, New Zealand short-term rate down -9.60% to 4.33%, signaling differing policy outlooks.

The Day Ahead

Focus shifts to New Zealand's Business NZ PMI on March 12, previous at 55.2 showing expansion; a reading below 50 might indicate manufacturing contraction from dairy export weakness and China demand. No major Australian data today, March 10, giving markets time to absorb yesterday's figures and global developments. Watch for RBNZ remarks on housing ties, given recent construction softness.

ANZ calendar is quiet, but commodity shifts in iron ore and gold could sway Australian sentiment. ASX miners like BHP may track China updates, while NZX could respond to tourism signals.

Other Economic Notes

Australia's commodity exports bolster its economy, with gold gains offsetting Brent crude's -10.99% fall to 88.08, potentially lowering import costs but challenging LNG. New Zealand's dairy sector faces global risk aversion, as NZD/USD nears 0.5900 despite gains, with tourism recovery providing some offset. Housing in both nations is rate-sensitive: Australian prices steady on exports, New Zealand's building slows under higher costs.

Bitcoin at 70,001.09 (+2.34%) highlights crypto resilience, aiding tech areas in Australia.