ANZ Macro Daily(Beta Mode)

ANZ Currencies Tumble, Stocks Slip

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,629.00 | -1.31% |

| NZX 50 | 13,199.29 | -0.71% |

| AUD/USD | 0.71 | -0.57% |

| NZD/USD | 0.59 | -1.14% |

| AUD/NZD | 1.21 | +0.59% |

| BHP | 50.83 | -2.17% |

| Gold | 5,100.50 | -1.29% |

| Brent Crude | 97.37 | +5.86% |

| Bitcoin | 70,480.76 | +0.39% |

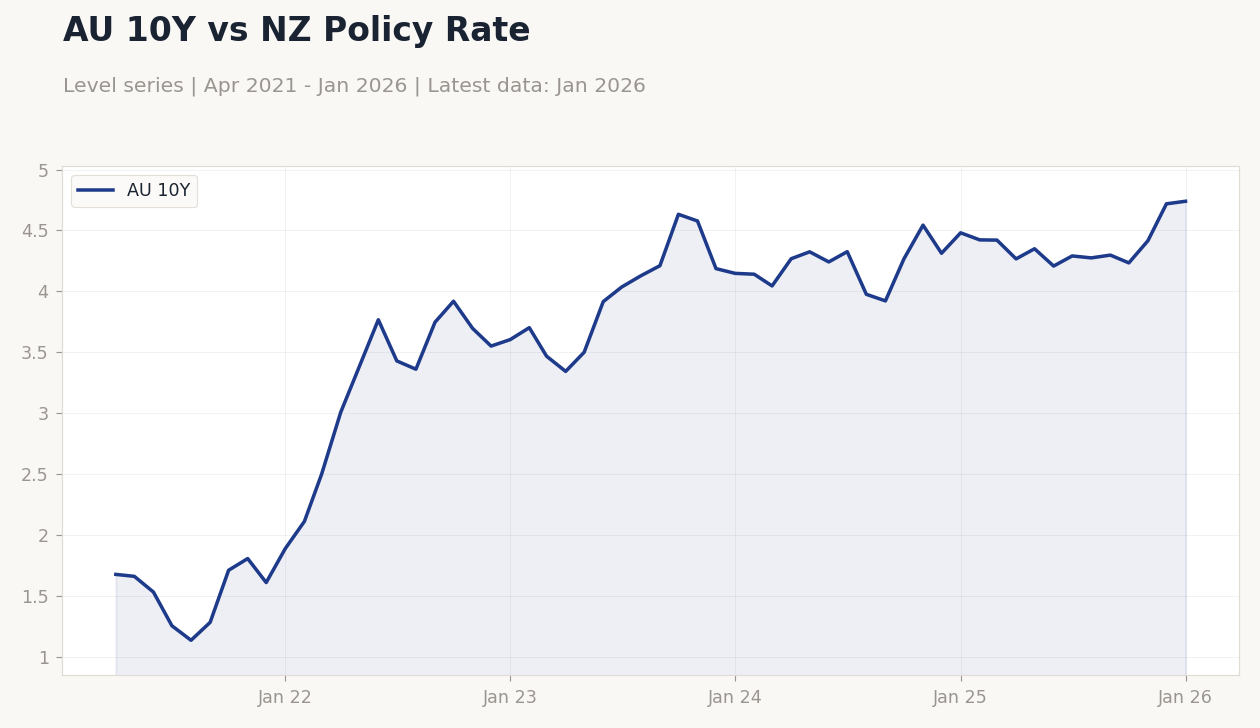

| Australia 10Y Govt Yield | 4.74% | +0.45% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

AU 10Y vs NZ Policy Rate | Type: macro_line | AU 10Y: 4.74 (2026-01-01) | Range: 1.135–4.74 | Trend(6pt): 1.676,3.767,4.128,4.267,4.719,4.74

AU 10Y vs NZ Policy Rate | Type: macro_line | AU 10Y: 4.74 (2026-01-01) | Range: 1.135–4.74 | Trend(6pt): 1.676,3.767,4.128,4.267,4.719,4.74

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Business NZ PMI | 55.20 | - | 17:30 |

| RBA Interest Rate Decision | 3.85 | - | 23:30 |

| RBA Press Conference | - | - | 00:30 |

| Current Account Balance | -8,370m | - | 17:45 |

| GDP Growth Quarter-over-Quarter | 1.10 | - | 17:45 |

| GDP Growth Year-over-Year | 1.30 | - | 17:45 |

| Employment Change | 17,800 | - | 20:30 |

| Full-Time Employment Change | 50,500 | - | 20:30 |

| Headline Unemployment Rate | 4.10 | - | 20:30 |

| Trade Balance | -519m | - | 17:45 |

- ANZ equities and currencies weakened amid global risk-off sentiment, with AUD/USD testing 0.7000 and NZD/USD nearing 0.5900.

- Commodity prices diverged, as Brent crude surged 5.86% while gold fell 1.29%, impacting Australia's export outlook.

- Bond yields rose slightly in Australia, signaling caution on RBA policy, while New Zealand rates eased sharply.

Yesterday's Recap

With no major data releases in Australia or New Zealand on March 11, markets focused on global risk aversion, leading to declines in key indices. Australia's ASX 200 fell 1.31% to 8,629.00, pressured by weakness in mining stocks like BHP, which dropped 2.17% to 50.83 amid volatile commodity signals. New Zealand's NZX 50 declined 0.71% to 13,199.29, reflecting broader caution in dairy and export sectors.

The AUD/USD slid 0.57% to 0.71, testing below the 0.7000 handle intraday, while NZD/USD tumbled 1.14% to 0.59, its lowest since late January. Cross-rate AUD/NZD rose 0.59% to 1.21, underscoring Australia's relative resilience. Australia's 10-year government yield edged up 0.45% to 4.74%, hinting at inflation persistence, while New Zealand's short-term rate dropped sharply by 9.60% to 4.33%.

Overall, these moves highlighted ANZ's vulnerability to external shocks, particularly from China-linked commodities.

The Day Ahead

Attention turns to New Zealand's Business NZ PMI release at 17:30 ET on March 12, with the previous reading of 55.2 signaling expansion; a dip could pressure NZD further amid softening manufacturing. Australia's RBA interest rate decision is slated for March 16 at 23:30 ET, following the current 3.60% cash rate, with markets eyeing any hawkish signals on inflation. This will be followed by the RBA press conference on March 17 at 00:30 ET, potentially clarifying policy divergence from global peers.

New Zealand's current account balance arrives on March 17 at 17:45 ET, after a prior -8.37 billion deficit, which could highlight trade vulnerabilities. GDP figures for New Zealand follow on March 18 at 17:45 ET, with previous QoQ at 1.1% and YoY at 1.3%, offering insights into growth momentum. Australia's employment data on March 18 at 20:30 ET, including a prior 17,800 job change and 4.1% unemployment rate, will be critical for RBA rate path assessments.

New Zealand's trade balance is due on March 19 at 17:45 ET, following a prior -519 million deficit.

Other Economic Notes

Australia's housing market remains a key concern, with high interest rates curbing affordability and construction activity, potentially weighing on consumer spending amid elevated commodity exports to China. (cont...)