ANZ Macro Daily(Beta Mode)

RBA Hike Looms, PMI Softens

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,617.10 | -0.14% |

| NZX 50 | 13,187.34 | -0.09% |

| AUD/USD | 0.70 | -2.04% |

| NZD/USD | 0.58 | -2.05% |

| AUD/NZD | 1.21 | -0.10% |

| BHP | 50.06 | -1.80% |

| Gold | 5,023.20 | -1.81% |

| Brent Crude | 103.36 | +2.89% |

| Bitcoin | 71,383.66 | +1.26% |

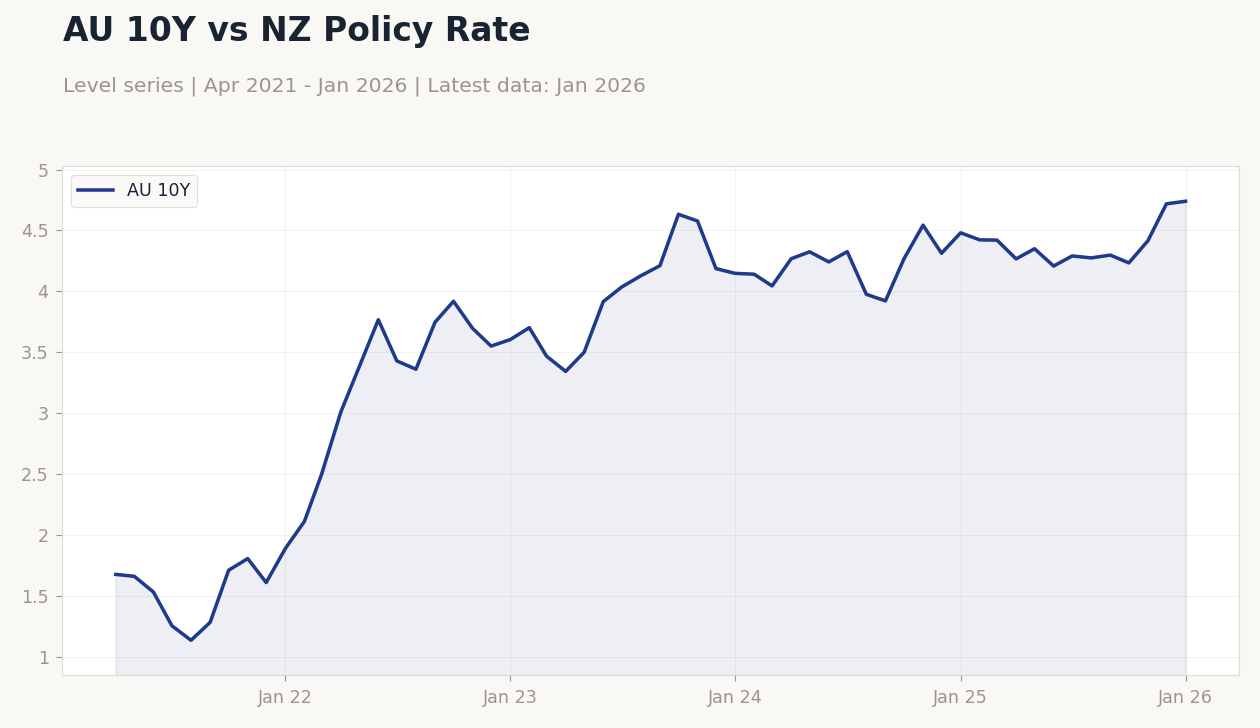

| Australia 10Y Govt Yield | 4.74% | +0.45% |

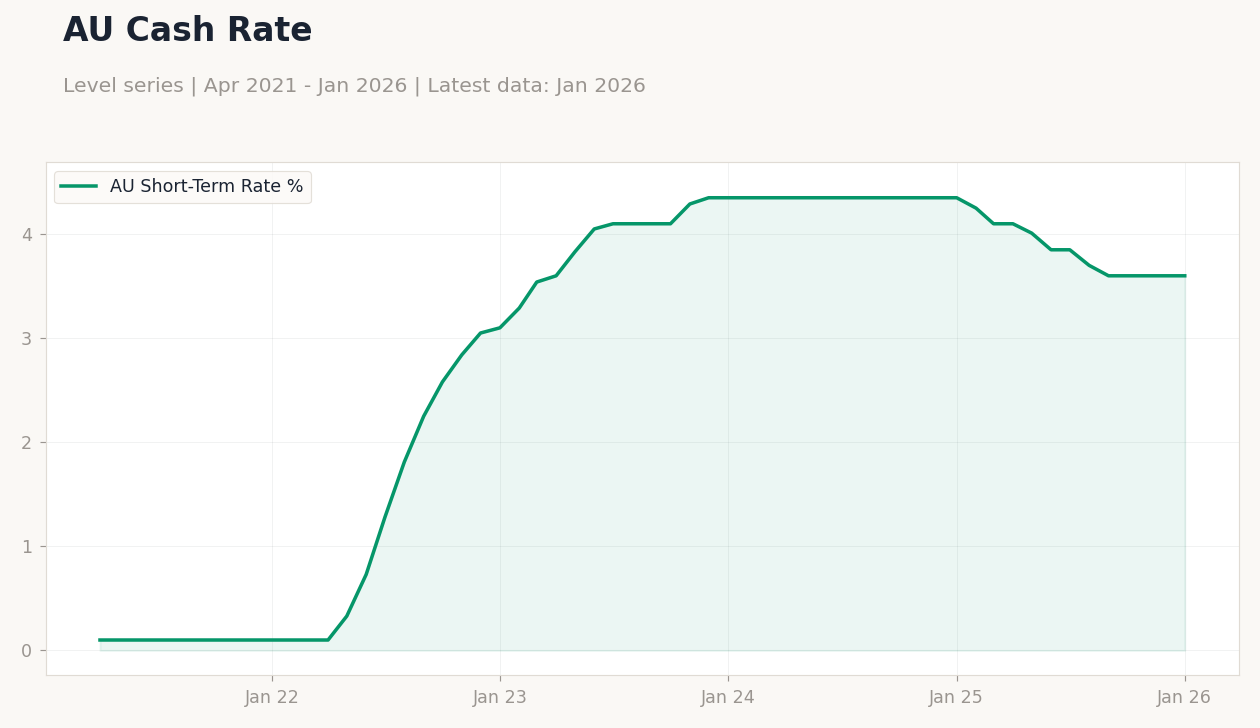

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Business NZ PMI | 55.10 | - | 55 |

AU 10Y vs NZ Policy Rate | Type: macro_line | AU 10Y: 4.74 (2026-01-01) | Range: 1.135–4.74 | Trend(6pt): 1.676,3.767,4.128,4.267,4.719,4.74

AU 10Y vs NZ Policy Rate | Type: macro_line | AU 10Y: 4.74 (2026-01-01) | Range: 1.135–4.74 | Trend(6pt): 1.676,3.767,4.128,4.267,4.719,4.74

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| RBA Interest Rate Decision | 3.85 | 4.10 | 23:30 |

| RBA Press Conference | - | - | 00:30 |

| Current Account Balance | -8,370m | -4,850m | 17:45 |

| GDP Growth Quarter-over-Quarter | 1.10 | 0.40 | 17:45 |

| GDP Growth Year-over-Year | 1.30 | 1.50 | 17:45 |

| Employment Change | 17,800 | 20,000 | 20:30 |

| Full-Time Employment Change | 50,500 | - | 20:30 |

| Headline Unemployment Rate | 4.10 | 4.20 | 20:30 |

| Trade Balance | -519m | - | 17:45 |

- New Zealand's Business NZ PMI dipped to 55.0 in February, indicating a mild slowdown in manufacturing amid global headwinds.

- ANZ equities edged lower, with ASX 200 down 0.14% and NZX 50 off 0.09%, weighed by commodity declines and RBA hike expectations.

- AUD and NZD fell over 2% against USD, driven by dollar strength, oil volatility, and inflation fears.

Yesterday's Recap

New Zealand's Business NZ PMI for February registered at 55.0, a slight drop from January's 55.1, reflecting ongoing but easing expansion in manufacturing due to dairy export challenges and softer global demand. Australia had no key data releases, but markets felt pressure from the impending RBA decision, resulting in a 0.14% decline in the ASX 200 to 8,617.10, driven by mining sector weakness with BHP down 1.80% to 50.06. The NZX 50 slipped 0.09% to 13,187.34, amid caution ahead of GDP and trade figures.

Currencies faced headwinds, with AUD/USD dropping 2.04% to 0.70 and NZD/USD falling 2.05% to 0.58, fueled by a robust U.S. dollar and Brent crude rising 2.89% to 103.36. The AUD/NZD cross eased 0.10% to 1.21, showing limited divergence between the pairs despite overall depreciation.

Gold declined 1.81% to 5,023.20, adding strain on exporters, while Australia's 10Y government yield increased 0.45% to 4.74%, betting on tighter policy. ANZ assets lagged due to Middle East geopolitical risks and RBA tightening concerns.

The Day Ahead

Focus shifts to Australia's RBA interest rate decision on March 16, with consensus for a rise to 4.10% from 3.85%, followed by a press conference on March 17 offering insights on inflation and housing. New Zealand's Q4 current account balance releases on March 17, expected at -4.85 billion NZD versus prior -8.37 billion. GDP data follows on March 18, with quarter-over-quarter forecast at 0.4% and year-over-year at 1.5%.

Australia's employment metrics arrive on March 18, including change projected at 20,000, full-time shifts, and unemployment rate anticipated at 4.2% from 4.1%. New Zealand's February trade balance is due on March 19, previous at -519 million NZD, influenced by dairy and tourism trends. These could shape RBNZ views, particularly if GDP deviates from expectations, alongside monitoring global oil impacts.

Other Economic Notes

ANZ economies are exposed to commodity fluctuations, with Australia's iron ore and LNG facing risks from China's slowdown and elevated freight costs due to war risks. New Zealand's dairy sector contends with weak global demand and lingering tourism recovery issues. (cont...)