ANZ Macro Daily(Beta Mode)

RBA Hikes to 4.1%, NZ Deficit Widens

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,640.60 | +0.31% |

| NZX 50 | 13,315.60 | +1.01% |

| AUD/USD | 0.70 | -0.45% |

| NZD/USD | 0.58 | -0.78% |

| AUD/NZD | 1.21 | -0.08% |

| BHP | 50.19 | +0.92% |

| Gold | 4,848.50 | -3.05% |

| Brent Crude | 104.91 | +1.44% |

| Bitcoin | 71,111.24 | -3.80% |

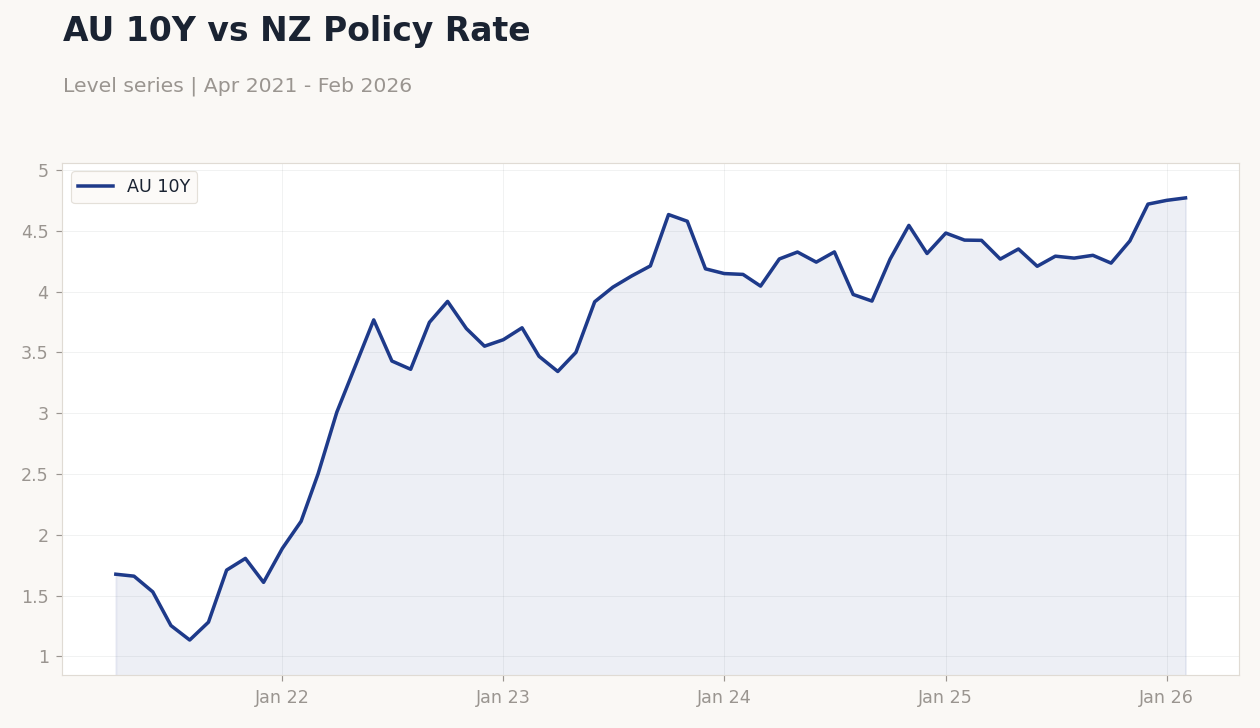

| Australia 10Y Govt Yield | 4.77% | +0.42% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| RBA Interest Rate Decision | 3.85 | 4.10 | 4.10 |

| RBA Press Conference | - | - | - |

| Current Account Balance | -8,360m | -4,750m | -5,980m |

AU 10Y vs NZ Policy Rate | Type: macro_line | AU 10Y: 4.77 (2026-02-01) | Range: 1.135–4.77 | Trend(6pt): 1.676,3.767,4.128,4.267,4.719,4.77

AU 10Y vs NZ Policy Rate | Type: macro_line | AU 10Y: 4.77 (2026-02-01) | Range: 1.135–4.77 | Trend(6pt): 1.676,3.767,4.128,4.267,4.719,4.77

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| GDP Growth Quarter-over-Quarter | 1.10 | 0.40 | 13:45 |

| GDP Growth Year-over-Year | 1.30 | 1.70 | 13:45 |

| Employment Change | 17,800 | 20,300 | 16:30 |

| Full-Time Employment Change | 50,500 | - | 16:30 |

| Headline Unemployment Rate | 4.10 | 4.10 | 16:30 |

| Trade Balance | -519m | -470m | 13:45 |

- RBA raised rates by 25bps to 4.1% in a hawkish move, citing persistent inflation and oil shocks, with a 5-4 vote split.

- New Zealand's current account deficit came in at -NZ$5.98B, worse than consensus -NZ$4.75B but improved from previous -NZ$8.36B.

- Markets mixed: ASX 200 and NZX 50 gained, AUD and NZD weakened vs USD; Brent up, gold and Bitcoin down.

Yesterday's Recap

The Reserve Bank of Australia (RBA) hiked its cash rate by 25 basis points to 4.1%, meeting consensus but delivering a hawkish tone in the statement and press conference, emphasizing persistent inflation and oil shocks. The decision came on a 5-4 vote split, providing initial support for the AUD, though AUD/USD closed down 0.45% at 0.70 amid USD strength. In New Zealand, the current account balance was -NZ$5.98 billion, missing consensus of -NZ$4.75 billion but better than the prior -NZ$8.36 billion, highlighting ongoing external pressures from weak exports.

Australian equities rose, with the ASX 200 up 0.31% to 8,640.60, led by mining gains including BHP at 50.19 (up 0.92%) on firmer Brent crude at 104.91 (up 1.44%). The NZX 50 climbed 1.01% to 13,315.60, aided by construction and tourism optimism. AUD/NZD fell 0.08% to 1.21, showing Australian edge.

Australia's 10Y yield rose 0.42% to 4.77%, while New Zealand's short-term rate dropped 9.60% to 4.33%, signaling policy divergence.

The Day Ahead

New Zealand's Q4 GDP data at 13:45 ET expects QoQ growth of 0.4% (prior 1.1%) and YoY of 1.7% (prior 1.3%), offering clues on economic resilience amid export and tourism challenges. Australia's February labor stats at 16:30 ET forecast employment change of 20,300 (prior 17,800), full-time change (no consensus, prior 50,500), and unemployment at 4.1% (prior 4.1%), key for RBA amid housing sensitivities. Tomorrow's NZ trade balance at 13:45 ET anticipates -NZ$470M (prior -NZ$519M), potentially weighing on NZD if deficits widen.

No major ANZ central bank events today, but data could influence RBNZ easing bets if soft.

Other Economic Notes

Australia's economy shows heavy reliance on commodity exports, with RBA charts highlighting risks from China's slowdown, potentially echoing GFC-like vulnerabilities if demand weakens. New Zealand faces construction and tourism headwinds from high rates, contributing to housing corrections and softer spending. De-dollarisation trends are evident globally, with Australia advancing an EU trade deal to diversify and add $10B to GDP, mitigating USD dominance amid US-China tensions.