Other Economic Notes

The RBA's hike to 4.1% adds strain to Australia's housing sector, with savings rates increasing and possibly dampening mortgage activity, particularly for older borrowers facing elevated costs. New Zealand's construction activity, a growth pillar, risks further deceleration after the GDP shortfall, compounding dairy export risks in a volatile trade environment. ANZ ties to China are crucial, where Australian iron ore and LNG could buffer oil shocks, unlike New Zealand's agriculture-heavy economy vulnerable to FX swings.

Broader war effects, including inflation from fuel prices, may widen these divergences.

Global Macro News

Iran war tensions lead headlines, with the RBA noting elevated risks of global shocks like oil surges inflating Australian imports and threatening supplies from Malaysia. Brent crude slipped 1.78% to $106.72, but fears overshadowed the RBA decision, holding AUD/USD near 0.7090. In Asia, Japan's yen strengthened against the dollar after central banks held steady, while USD/JPY rose on U.S.

dollar gains limited by BoJ hawkishness, aiding NZD through carry trades. China's outlook, key for ANZ commodities, contends with inflation as Brazil sees war-fueled price rises pre-election. The Philippine peso reached P60 per dollar, and Nigeria's 2025 balance of payments fell 38.1%, indicating emerging market pressures that might curb Australian export demand.

Gold declined 2.18% to $4,500.20 as a haven asset, while Bitcoin rose 0.18% to $70,041.38 in mixed sentiment. Discussions on petrodollar shifts due to the war reshape energy markets, increasing ANZ exposure to Middle East instability. These elements highlight ANZ policy splits, with Australia's commodity strength versus New Zealand's agri vulnerabilities.

ANZ Central Banks Watch

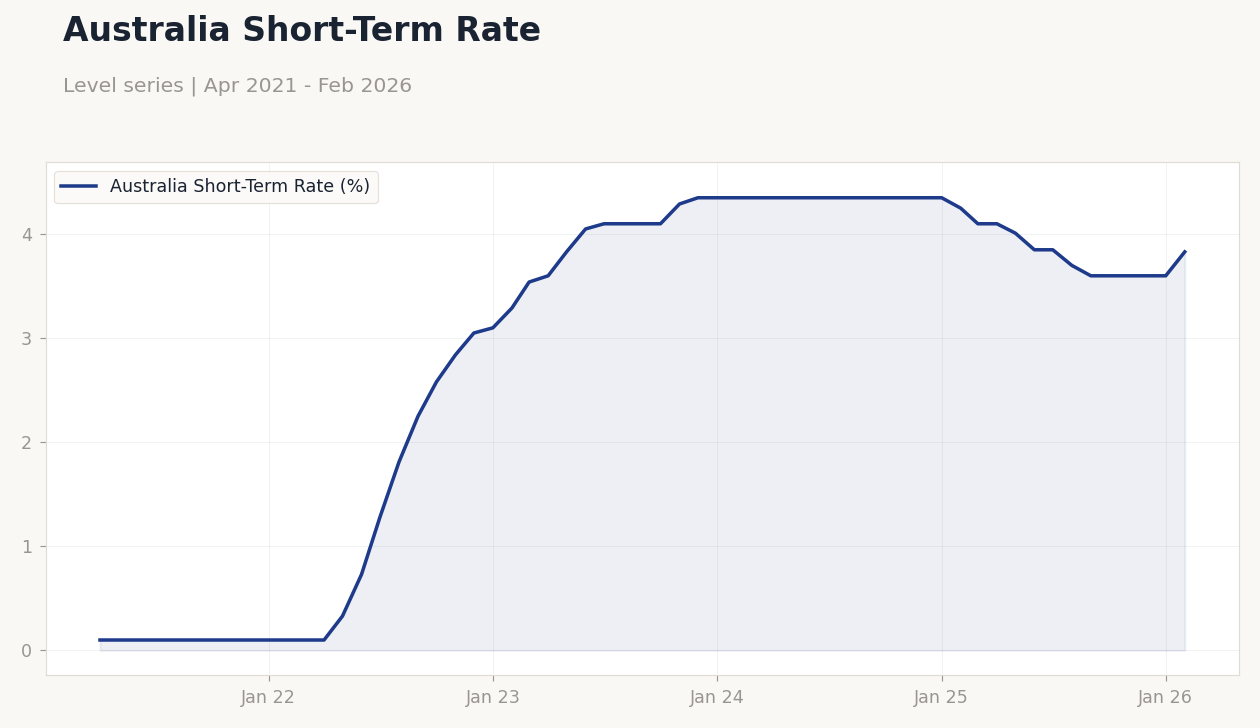

The RBA increased its cash rate to 4.1% on March 16 as anticipated, focusing on inflation vigilance amid Middle East war risks like petrol price jumps. This aligns with employment data showing solid gains but a 4.3% unemployment uptick and full-time losses, which might temper future hikes if housing softens. The RBNZ, meanwhile, grapples with 0.2% QoQ GDP weakness, potentially fostering dovishness relative to past aggressive moves, with no near-term actions indicated.

Differences endure, as RBA's policy suits Australia's commodity economy, while RBNZ tracks housing and a wider current account deficit. Both prioritize inflation, but RBNZ's history suggests possible cuts if NZD appreciation hurts exports. Trade gains provide slight NZ relief, yet unified oil shocks could align ANZ inflation paths.

Australia Short-Term Rate | Type: macro_line | Australia Short-Term Rate (%): 3.83 (2026-02-01) | Range: 0.1–4.35 | Trend(6pt): 0.1,0.73,4.1,4.35,3.6,3.83

Australia Short-Term Rate | Type: macro_line | Australia Short-Term Rate (%): 3.83 (2026-02-01) | Range: 0.1–4.35 | Trend(6pt): 0.1,0.73,4.1,4.35,3.6,3.83