ANZ Macro Daily(Beta Mode)

RBA Hikes Fail to Lift AUD

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,365.90 | -0.74% |

| NZX 50 | 12,899.72 | -0.69% |

| AUD/USD | 0.70 | -0.97% |

| NZD/USD | 0.59 | -0.01% |

| AUD/NZD | 1.21 | -0.51% |

| BHP | 47.47 | -1.82% |

| Gold | 4,414.90 | -3.40% |

| Brent Crude | 99.69 | -11.14% |

| Bitcoin | 70,700.36 | +4.21% |

| Australia 10Y Govt Yield | 4.77% | +0.42% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

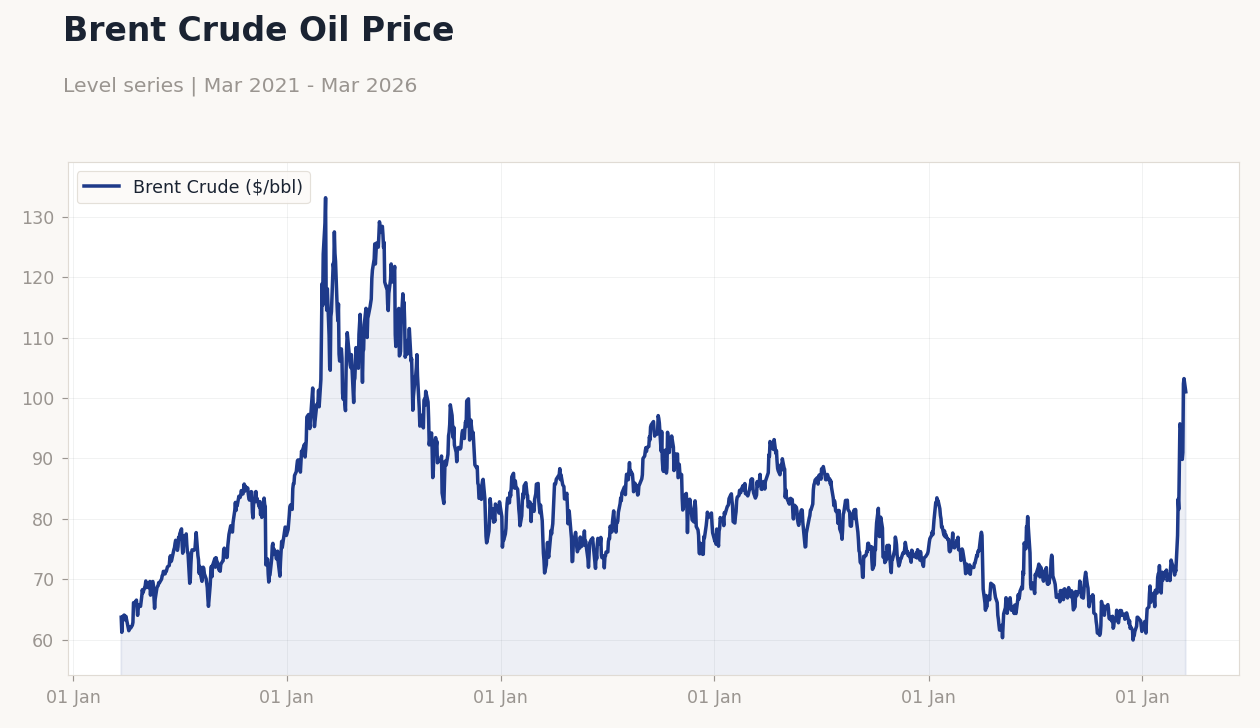

Brent Crude Oil Price | Type: macro_line | Brent Crude ($/bbl): 101 (2026-03-16) | Range: 59.93–133.2 | Trend(6pt): 63.7,115.5,94.56,74.89,103.2,101

Brent Crude Oil Price | Type: macro_line | Brent Crude ($/bbl): 101 (2026-03-16) | Range: 59.93–133.2 | Trend(6pt): 63.7,115.5,94.56,74.89,103.2,101

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| S&P Global Manufacturing PMI Flash | 51 | - | 18:00 |

| S&P Global Services PMI Flash | 52.80 | - | 18:00 |

| Inflation Rate Month-over-Month | 0.40 | 0 | 20:30 |

| Inflation Rate Year-over-Year | 3.80 | 3.80 | 20:30 |

| RBA Trimmed Mean CPI Month-over-Month | 0.30 | - | 20:30 |

| RBA Trimmed Mean CPI Year-over-Year | 3.40 | 3.40 | 20:30 |

| RBA Jones Speech | - | - | 22:40 |

| RBA Kent Speech | - | - | 18:15 |

- RBA's back-to-back rate hikes overshadowed by geopolitical fears, leading to AUD/USD slump despite bullish forecasts.

- Australian and NZ markets decline on commodity weakness; Fitch cuts NZ rating outlook to negative.

- Key AU PMI and inflation data ahead, alongside RBA speeches, to guide policy expectations.

Yesterday's Recap

Australian equity markets declined as the ASX 200 closed at 8,365.90, down 0.74%, driven by falls in mining stocks like BHP, which dropped 1.82% to 47.47 amid sliding commodity prices. New Zealand's NZX 50 finished at 12,899.72, down 0.69%, amid regional risk aversion. The AUD/USD pair fell 0.97% to 0.70, undermined by geopolitical tensions despite RBA hikes, while NZD/USD edged down 0.01% to 0.59.

The AUD/NZD cross weakened 0.51% to 1.21, underscoring Australia's commodity exposure. Australian 10-year government yields increased 0.42% to 4.77%, reflecting hawkish sentiment, while New Zealand's short-term rate fell 9.60% to 4.33%, potentially linked to Fitch's negative outlook cut on debt concerns. No significant data releases occurred in Australia or New Zealand, with markets focused on global news such as the Iran war's inflationary effects.

Commodities weakened sharply, with gold down 3.40% to 4,414.90 and Brent crude plunging 11.14% to 99.69, pressuring Australia's export sectors, though Bitcoin rose 4.21% to 70,700.36.

The Day Ahead

Australian S&P Global Manufacturing PMI Flash and Services PMI Flash release at 18:00 ET today, with previous readings of 51 and 52.8, providing early March activity signals amid global demand softness. Tomorrow features Australian inflation data at 20:30 ET, including month-over-month (consensus 0%, previous 0.4%) and year-over-year rates (consensus 3.8%, previous 3.8%), plus RBA Trimmed Mean CPI month-over-month (previous 0.3%) and year-over-year (consensus 3.4%, previous 3.4%), which may affect rate outlooks. An RBA Jones speech follows at 22:40 ET tomorrow, potentially addressing inflation and housing risks.

On March 25, RBA Kent speaks at 18:15 ET, offering insights on policy divergence. No immediate New Zealand events, but ANZ markets may respond to Australian data due to trade ties. Watch for PMI surprises indicating manufacturing slowdowns.

Other Economic Notes

Australia's economy depends heavily on commodity exports, vulnerable to global energy disruptions from the Iran war, though upcoming EU-Australia free trade agreement could enhance diversification. (cont...)