ANZ Macro Daily(Beta Mode)

AU PMIs Soften, RBA Hike Weighs

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,379.40 | +0.16% |

| NZX 50 | 12,899.72 | -0.69% |

| AUD/USD | 0.70 | -0.17% |

| NZD/USD | 0.58 | +0.11% |

| AUD/NZD | 1.20 | -0.31% |

| BHP | 48.51 | +2.97% |

| Gold | 4,467.00 | +1.43% |

| Brent Crude | 100.00 | +0.06% |

| Bitcoin | 70,056.45 | -1.21% |

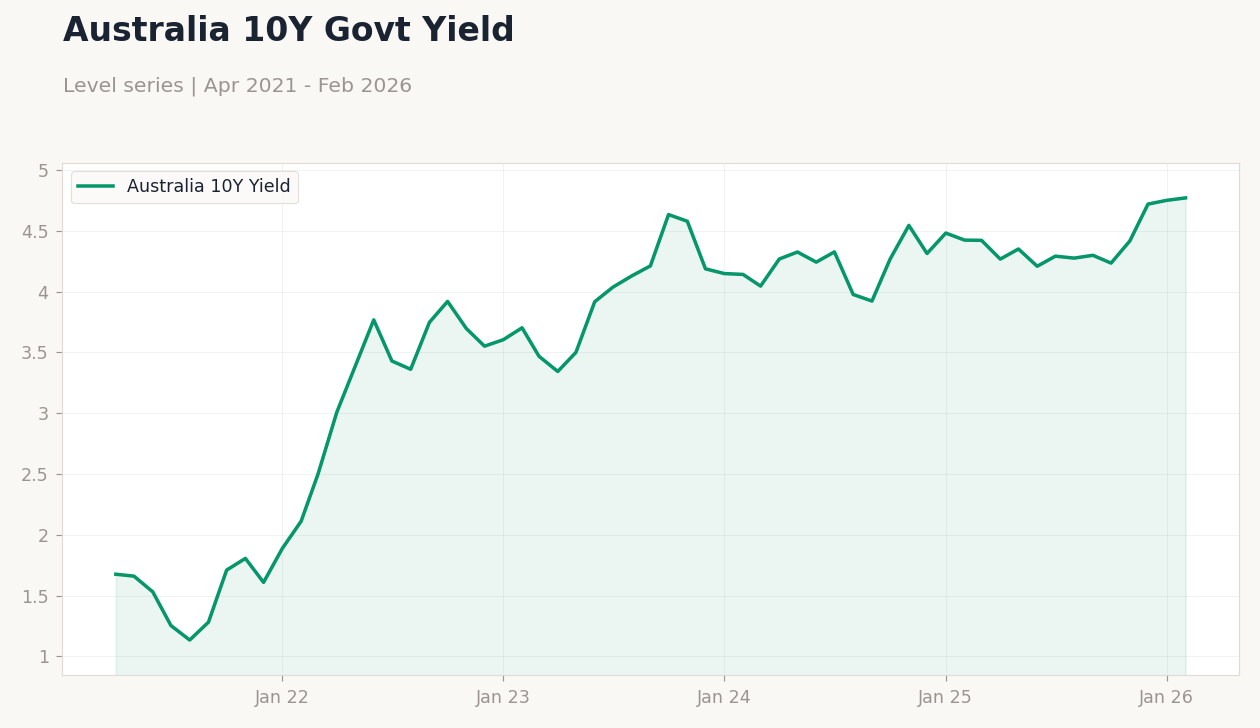

| Australia 10Y Govt Yield | 4.77% | +0.42% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| S&P Global Manufacturing PMI Flash | 51 | - | 50.10 |

| S&P Global Services PMI Flash | 52.80 | - | 46.60 |

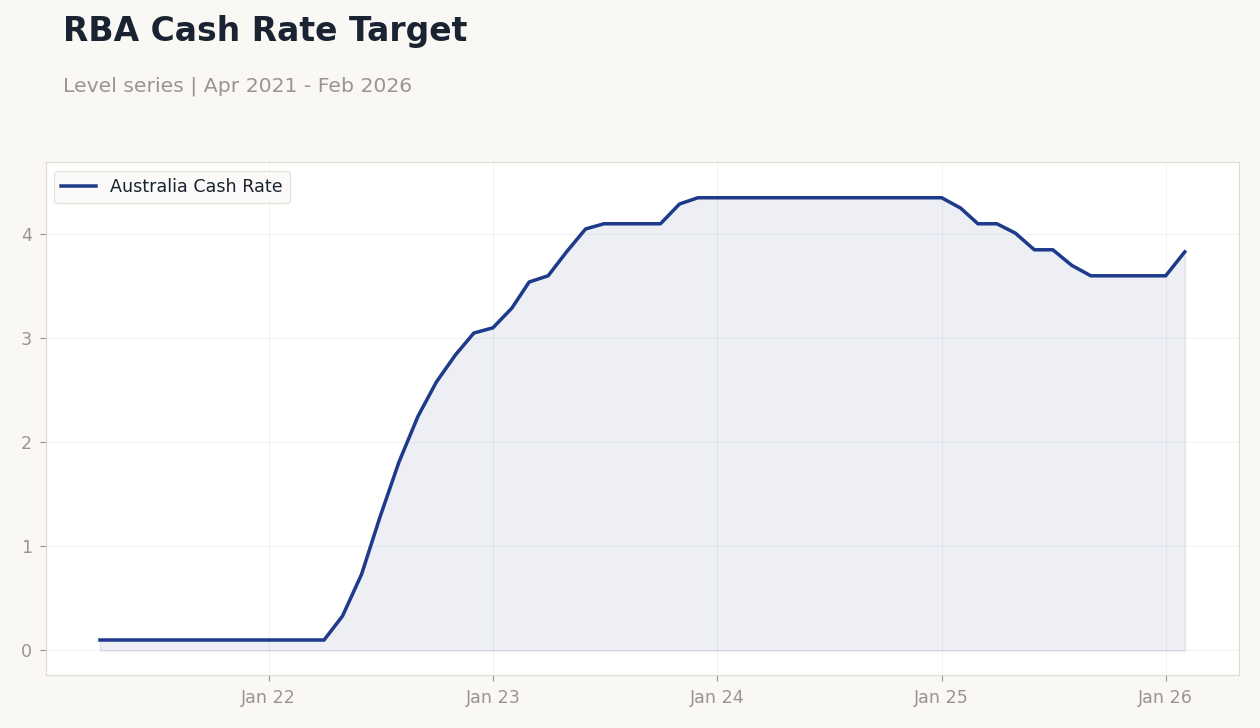

RBA Cash Rate Target | Type: macro_line | Australia Cash Rate: 3.83 (2026-02-01) | Range: 0.1–4.35 | Trend(6pt): 0.1,0.73,4.1,4.35,3.6,3.83

RBA Cash Rate Target | Type: macro_line | Australia Cash Rate: 3.83 (2026-02-01) | Range: 0.1–4.35 | Trend(6pt): 0.1,0.73,4.1,4.35,3.6,3.83

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Inflation Rate Month-over-Month | 0.40 | 0 | 16:30 |

| Inflation Rate Year-over-Year | 3.80 | 3.80 | 16:30 |

| RBA Trimmed Mean CPI Month-over-Month | 0.30 | - | 16:30 |

| RBA Trimmed Mean CPI Year-over-Year | 3.40 | 3.40 | 16:30 |

| RBA Jones Speech | - | - | 18:40 |

- Australian PMIs weakened, with services in contraction amid inflation concerns.

- Markets mixed: ASX up 0.16%, NZX down 0.69%; AUD/USD slips 0.17%.

- RBA's recent rate hike in split decision lifts savings rates but erodes confidence.

Yesterday's Recap

Australian S&P Global Manufacturing PMI Flash eased to 50.1 from 51, indicating a slowdown in factory activity due to softer demand. Services PMI Flash dropped sharply to 46.6 from 52.8, signaling contraction in consumer sectors amid high borrowing costs. No key New Zealand data was released, keeping attention on Australia's figures, which tempered commodity stock sentiment.

ASX 200 ended at 8,379.40, up 0.16%, supported by miners including BHP at 48.51 (up 2.97%) as gold rose 1.43% to 4,467.00. NZX 50 fell 0.69% to 12,899.72, pressured by dairy export worries in volatile globals. AUD/USD declined 0.17% to 0.70, NZD/USD gained 0.11% to 0.58, pushing AUD/NZD down 0.31% to 1.20.

Australia's 10Y yield increased 0.42% to 4.77% on inflation worries, while New Zealand's short-term rate dropped 9.60% to 4.33% amid policy hints.

The Day Ahead

Australia's inflation releases lead today, with month-over-month rate expected at 0% after 0.4% prior, potentially reducing RBA pressure if on target. Year-over-year inflation is projected steady at 3.8%, and RBA trimmed mean CPI year-over-year at 3.4%, providing core price views amid housing strains. RBA Assistant Governor Jones speaks at 18:40, expected to discuss recent decisions and commodity inflation risks tied to iron ore and LNG exports.

These could influence AUD, particularly with China's growth affecting trade. No New Zealand events, focusing markets on Australian data for regional effects. Watch for RBNZ alignment signals, as dairy remains vulnerable to demand shifts.

Other Economic Notes

ANZ economies face ongoing inflation impacting spending, with Australian retail caution post-RBA hike and New Zealand housing possibly easing via approvals. Commodities provide resilience: Australia's iron ore and gold ties to China support fiscal health, while New Zealand's dairy aids trade surpluses despite tourism dips. Housing is key, with rising Australian mortgage stress and cooling New Zealand prices central to policy.

The EU-Australia trade deal improves mineral access, diversifying from China for sustained growth. Businesses stay resilient under rate pressures, but confidence reaches lows from oil costs and hikes.