Other Economic Notes

Australia's economy faces billions in losses from the US-Iran war, with petrol prices soaring to near A$2.20 per liter, exacerbating cost-of-living pressures and potentially curbing discretionary spending. New Zealand's dairy-driven exports offer some buffer, but tourism and construction sectors remain vulnerable to global risk aversion. Broader themes include persistent inflation in Australia, even before the oil shock, underscoring commodity dependence and China trade risks.

Housing markets in both countries link closely to rate paths, with former RBA insiders noting past decisions influenced by property prices.

Global Macro News

The US-Iran war continues to disrupt global energy supplies, sending Brent crude volatility higher and impacting ANZ as major commodity exporters, with Australia's LNG and coal trades at risk from Middle East instability. Euro and yen gains against the USD, following steady central bank rates, have indirectly pressured AUD and NZD lower amid safe-haven flows. India's Sensex jumped 0.75% to 76,070.84 on March 17, but ANZ markets contrast with declines, highlighting regional divergence driven by geopolitical risks over domestic data.

China's steel production cuts signal weakening demand, a critical drag for Australia's iron ore exports, which comprise a significant revenue share. Gold's rally to 4,524.30 provides a hedge for ANZ miners like BHP, yet overall risk-off sentiment from the conflict has led to AUD/USD slipping to around 0.6980. NZD/USD backslid to near 0.5900, erasing recent gains ahead of US jobs data, as global uncertainty builds.

These dynamics underscore China's growth outlook as the pivotal external driver for ANZ, with potential PMI data to watch for restocking signals.

ANZ Central Banks Watch

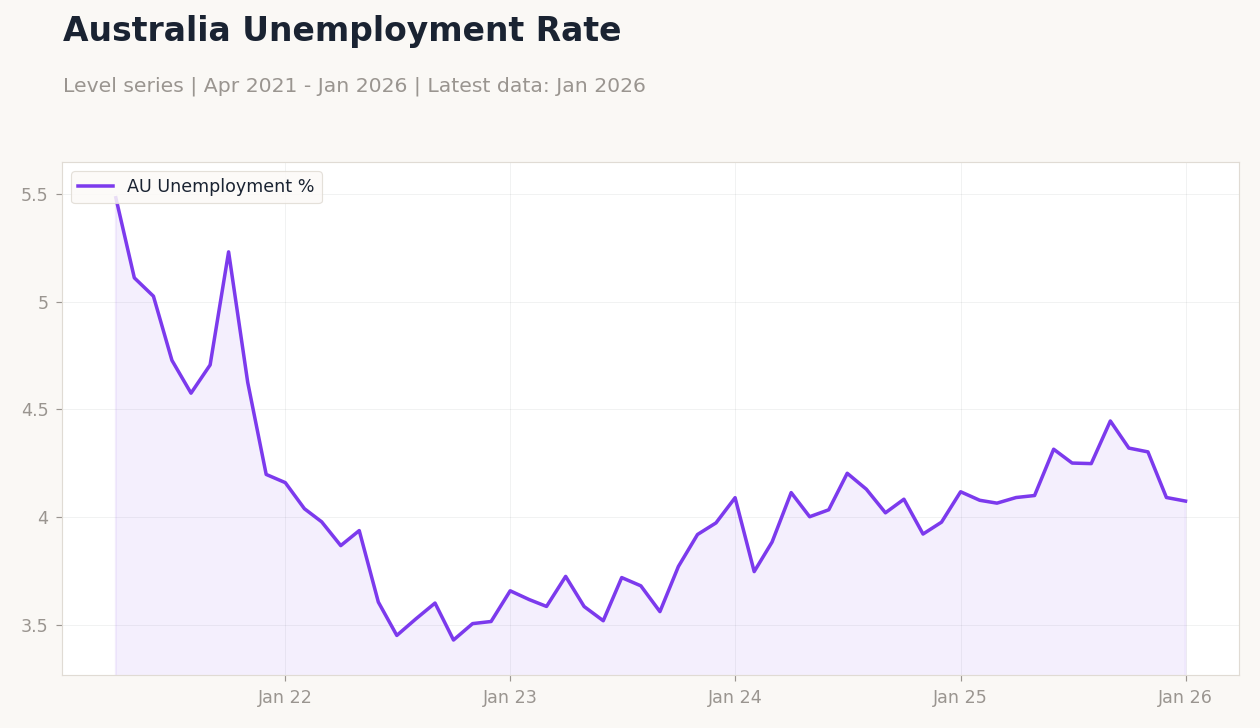

The RBA narrowly voted to lift interest rates in its latest decision, adding pressure on mortgages amid surging fuel prices from the Middle East war, with the cash rate at 3.83% as of February 1. This hike reflects elevated inflation persisting even before the Iran oil shock, and upcoming minutes may reveal discussions on housing market influences, as former insiders suggest property prices have factored into past decisions. In contrast, the RBNZ has shown historical aggressiveness in rate adjustments, though recent stability contrasts with RBA's move, potentially widening divergence in policy paths.

Both central banks target inflation independently, with RBNZ's framework more responsive to dairy and export dynamics, while RBA focuses on commodity and China linkages. Employment data implications remain key, as resilient Australian consumer spending could prompt further RBA tightening, whereas New Zealand's GDP contraction signals caution. Housing linkages are critical, with rate hikes risking slowdowns in both markets, but RBNZ's past boldness may lead to quicker pivots if global risks ease.

Brent Crude Oil Price | Type: macro_line | Brent Price USD: 103.8 (2026-03-23) | Range: 59.93–133.2 | Trend(6pt): 63.28,122.2,94.46,73.75,111,103.8

Brent Crude Oil Price | Type: macro_line | Brent Price USD: 103.8 (2026-03-23) | Range: 59.93–133.2 | Trend(6pt): 63.28,122.2,94.46,73.75,111,103.8