Yesterday's Recap

Australian markets ended lower on March 29, 2026, with the ASX 200 index down 0.65% at 8,461.00, pressured by geopolitical risks from the US-Iran conflict and a steep decline in Brent crude prices. New Zealand's NZX 50 index tumbled 1.44% to 12,748.92, reflecting broader risk aversion and weakness in dairy and tourism-exposed stocks. The AUD/USD pair weakened 0.55% to 0.68, while NZD/USD fell 0.75% to 0.57, with AUD/NZD nearly unchanged at 1.20 due to shared ties to China trade.

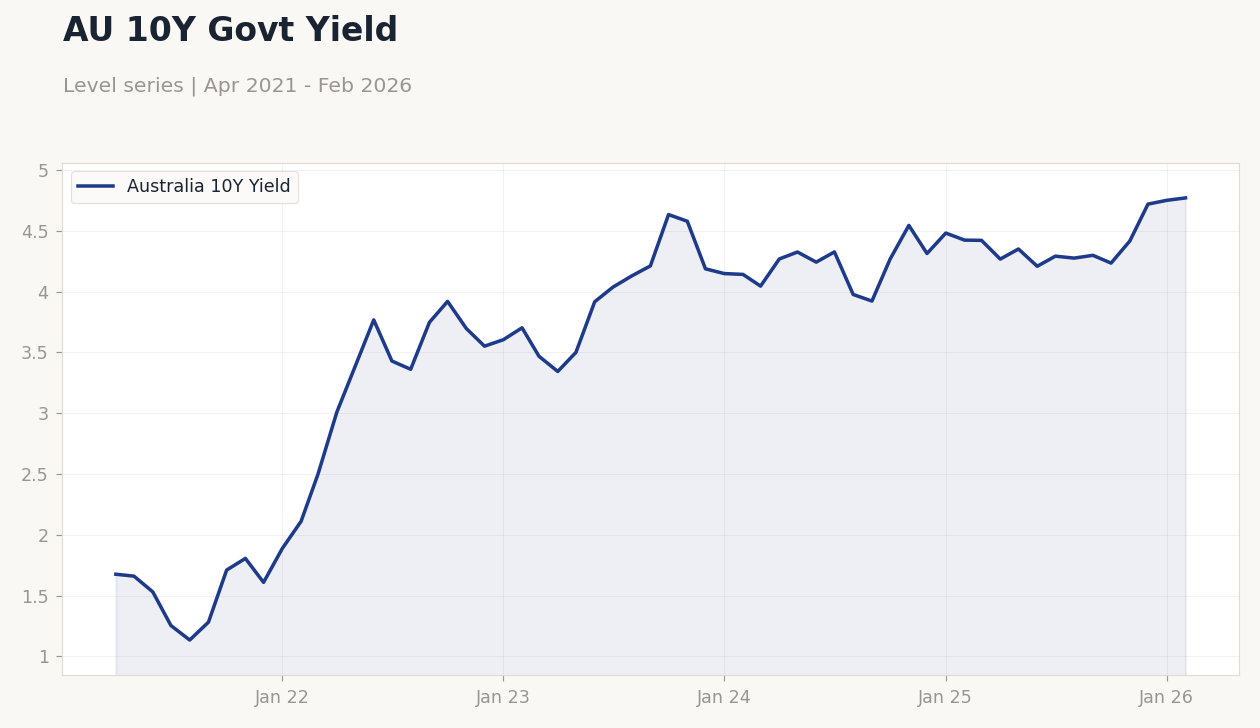

BHP stock rose 0.28% to 50.37, offering minor support to miners amid commodity fluctuations. Australia's 10-year government yield increased 0.42% to 4.77%, indicating worries over war-driven inflation and fuel costs. New Zealand's short-term rate dropped 9.60% to 4.33%, signaling easing expectations.

No significant economic data was released in Australia or New Zealand, allowing external factors like Australian petrol prices nearing A$2.20 per liter to dominate sentiment. Gold advanced 1.01% to 4,537.40 as a haven asset, while Bitcoin gained 0.83% to 66,502.34 in risk-off trading. The day underscored ANZ economies' exposure to Middle East instability and energy disruptions.

The Day Ahead

Attention turns to New Zealand's ANZ Business Confidence at 20:00 ET on March 30, 2026, previous 59.2, which may gauge sentiment amid war uncertainties. Australia's RBA Meeting Minutes release at 20:30 ET on March 30 could detail recent policy amid inflation and geopolitical risks. On March 31, Australia's Ai Group Industry Index is scheduled at 18:00 ET, prior -1.5, assessing manufacturing amid commodity pressures.

Australia's Building Permits Month-over-Month Preliminary follows at 20:30 ET on March 31, consensus 6.2% after -7.2%, key for housing and RBA outlook. Australia's Trade Balance arrives at 20:30 ET on April 1, consensus 2,500,000,000 after 2,631,000,000, highlighting export dynamics with China. These events could spur volatility in AUD and NZD, particularly with ongoing oil market swings and global risk flows.

AU 10Y Govt Yield | Type: macro_line | Australia 10Y Yield: 4.77 (2026-02-01) | Range: 1.135–4.77 | Trend(6pt): 1.676,3.767,4.128,4.267,4.719,4.77

AU 10Y Govt Yield | Type: macro_line | Australia 10Y Yield: 4.77 (2026-02-01) | Range: 1.135–4.77 | Trend(6pt): 1.676,3.767,4.128,4.267,4.719,4.77