ANZ Macro Daily(Beta Mode)

NZ Confidence Plunges, RBA Minutes Out

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,481.80 | +0.25% |

| NZX 50 | 12,912.11 | +1.28% |

| AUD/USD | 0.69 | +0.71% |

| NZD/USD | 0.57 | +0.34% |

| AUD/NZD | 1.20 | +0.38% |

| BHP | 50.49 | +0.12% |

| Gold | 4,715.00 | +4.18% |

| Brent Crude | 104.27 | -7.55% |

| Bitcoin | 67,760.16 | +1.60% |

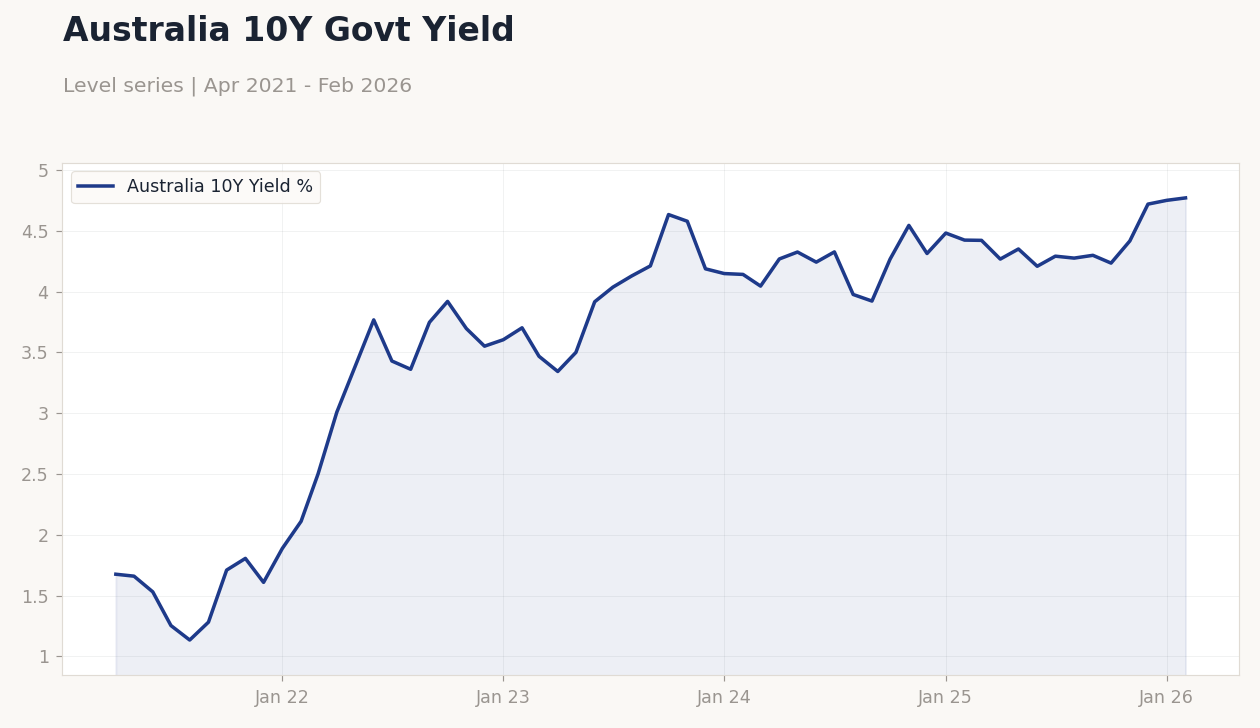

| Australia 10Y Govt Yield | 4.77% | +0.42% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| ANZ Business Confidence | 59.20 | - | 32.50 |

| RBA Meeting Minutes | - | - | - |

Australia 10Y Govt Yield | Type: macro_line | Australia 10Y Yield %: 4.77 (2026-02-01) | Range: 1.135–4.77 | Trend(6pt): 1.676,3.767,4.128,4.267,4.719,4.77

Australia 10Y Govt Yield | Type: macro_line | Australia 10Y Yield %: 4.77 (2026-02-01) | Range: 1.135–4.77 | Trend(6pt): 1.676,3.767,4.128,4.267,4.719,4.77

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Ai Group Industry Index | -1.50 | - | 18:00 |

| Building Permits Month-over-Month Prel | -7.20 | 6.50 | 20:30 |

| Trade Balance | 2,631m | 2,600m | 20:30 |

- New Zealand's ANZ Business Confidence fell sharply to 32.5 in March from 59.2 prior, highlighting weakening sentiment amid global risks.

- Australia's RBA released meeting minutes, stressing ongoing inflation concerns and housing market influences.

- ANZ markets gained modestly, with ASX 200 up 0.25% and NZX 50 rising 1.28%, despite US-Iran war tensions.

Yesterday's Recap

New Zealand's ANZ Business Confidence index tumbled to 32.5 in March from 59.2 previously, indicating growing business pessimism driven by economic slowdown concerns and external factors like the US-Iran conflict. Australia's RBA issued its meeting minutes, underscoring persistent inflationary pressures and the importance of monitoring housing prices, with no immediate policy changes signaled. Australian stocks rose slightly, with the ASX 200 ending at 8,481.80 after a 0.25% increase, aided by mining firms such as BHP, which gained 0.12% to 50.49 amid steady commodity markets.

New Zealand's NZX 50 advanced 1.28% to 12,912.11, lifted by banking and consumer stocks despite dairy sector weakness. Currency moves were positive, with AUD/USD up 0.71% to 0.69 and NZD/USD rising 0.34% to 0.57, while AUD/NZD increased 0.38% to 1.20 reflecting Australia's relative strength. Bond yields varied, with Australia's 10Y government yield up 0.42% to 4.77%, against a 9.60% drop in New Zealand's short-term rate to 4.33%.

These shifts highlight ANZ economies' exposure to global oil volatility, as Brent crude declined 7.55% to 104.27.

The Day Ahead

Australia's Ai Group Industry Index releases at 18:00 ET, offering views on manufacturing and services, following a -1.5 prior reading that pointed to contraction. Building Permits Month-over-Month Preliminary arrives at 20:30 ET, with consensus at 6.5% versus -7.2% last, key for assessing housing trends. Australia's Trade Balance is set for 20:30 ET on April 1, forecasted at 2.6 billion AUD surplus from 2.631 billion prior, underscoring export momentum in iron ore and LNG tied to China demand.

No significant New Zealand data today, shifting attention to Australian figures that may affect AUD trends. These releases could influence RBA outlooks, particularly if permits signal property market softening. Markets will monitor global cues, including US jobs data previews.

Other Economic Notes

Australia's economy contends with high inflation and rising fuel costs from the US-Iran war, with petrol prices approaching A$2.20 per liter curbing consumer spending. (cont...)