ANZ Macro Daily(Beta Mode)

NZ Confidence Dives, AU Trade Surges

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,579.50 | -1.06% |

| NZX 50 | 12,902.15 | +0.59% |

| AUD/USD | 0.69 | -0.20% |

| NZD/USD | 0.57 | -0.67% |

| AUD/NZD | 1.21 | +0.47% |

| BHP | 52.76 | +4.70% |

| Gold | 4,697.40 | -1.79% |

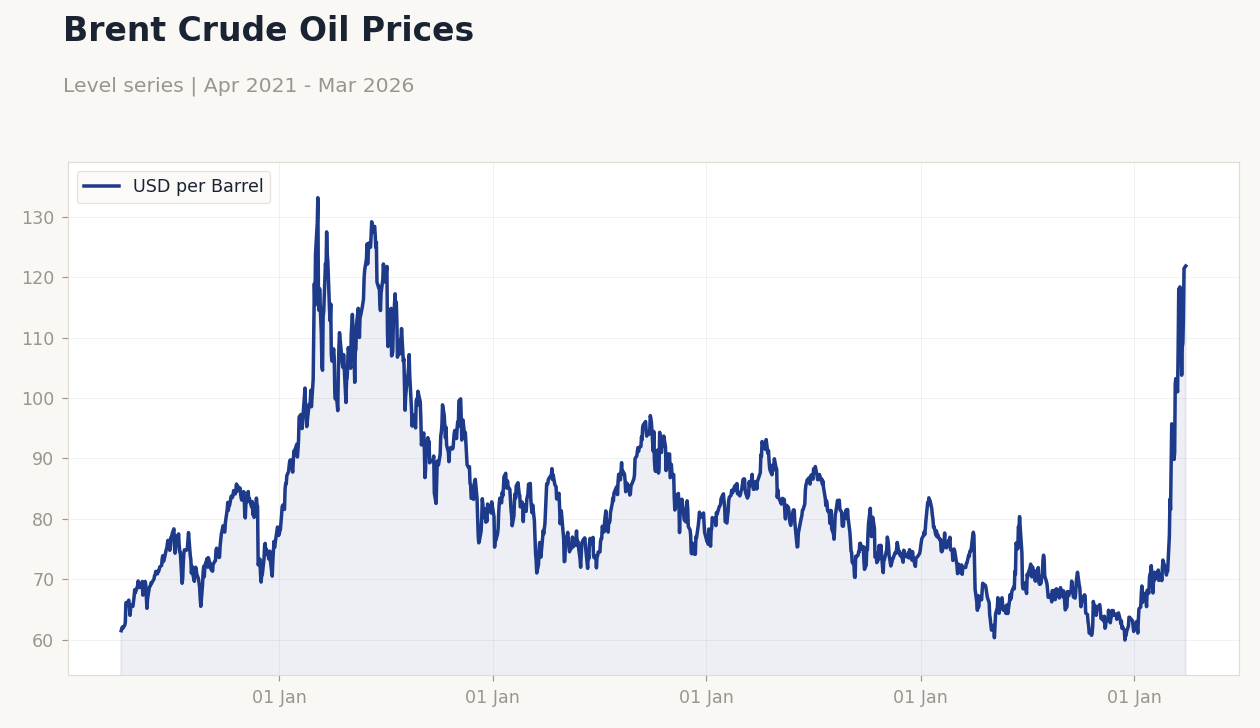

| Brent Crude | 108.64 | +7.39% |

| Bitcoin | 67,024.75 | -1.55% |

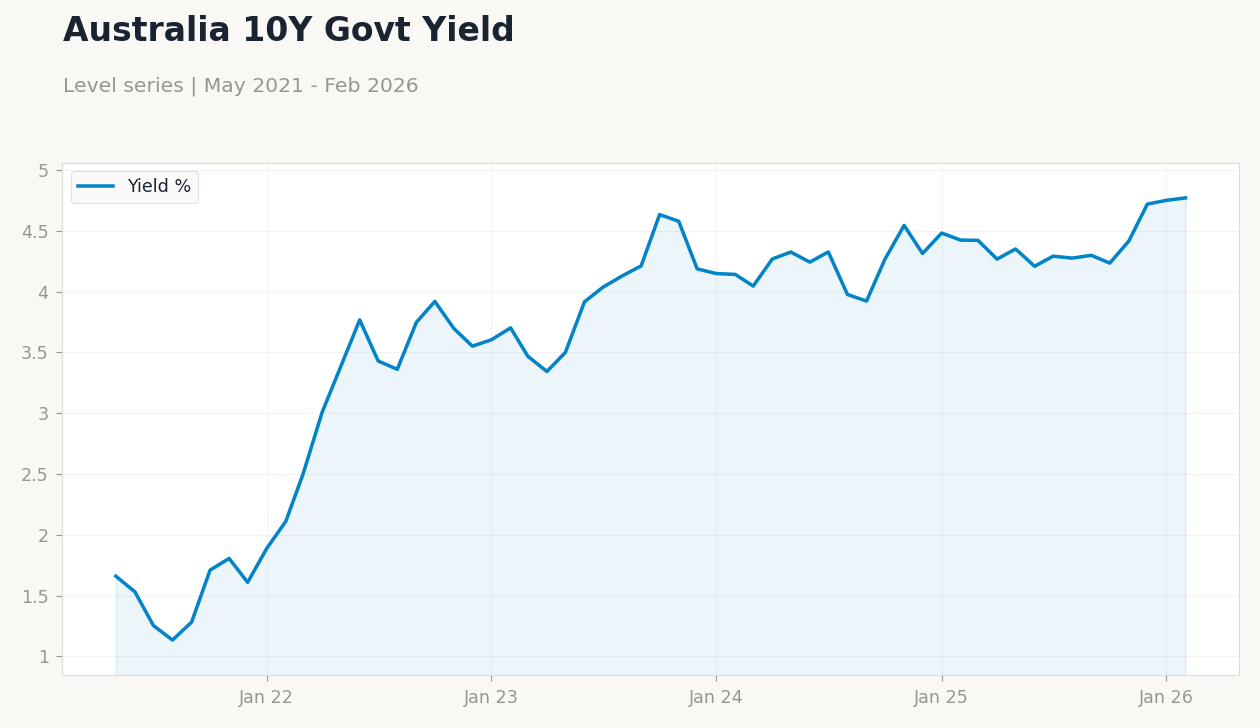

| Australia 10Y Govt Yield | 4.77% | +0.42% |

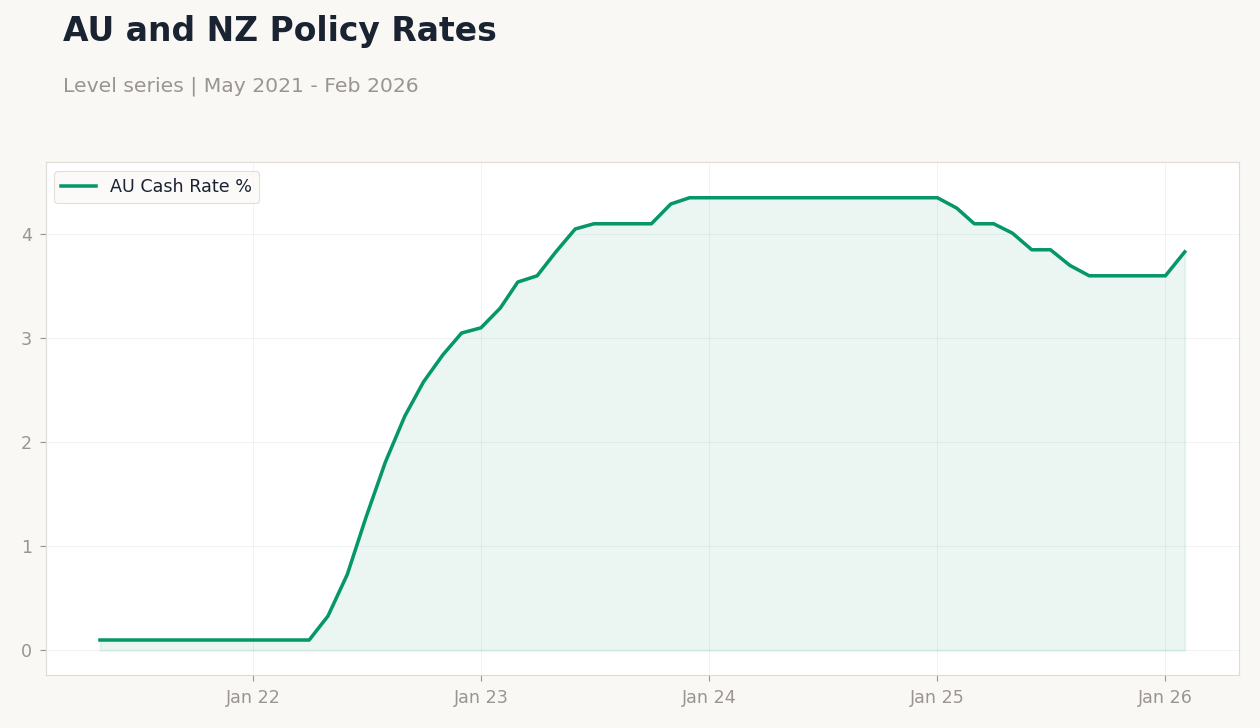

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| ANZ Business Confidence | 59.20 | - | 32.50 |

| RBA Meeting Minutes | - | - | - |

| Ai Group Industry Index | -1.50 | - | -23.60 |

| Building Permits Month-over-Month Prel | -7.20 | 6.50 | 29.70 |

| Trade Balance | 2,258m | 2,600m | 5,686m |

Brent Crude Oil Prices | Type: macro_line | USD per Barrel: 121.9 (2026-03-30) | Range: 59.93–133.2 | Trend(5pt): 61.47,121.8,94.46,74.58,121.9

Brent Crude Oil Prices | Type: macro_line | USD per Barrel: 121.9 (2026-03-30) | Range: 59.93–133.2 | Trend(5pt): 61.47,121.8,94.46,74.58,121.9

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- New Zealand's ANZ Business Confidence fell sharply to 32.5, indicating weakening sentiment amid global risks.

- Australia's trade surplus widened to A$5.686 billion, boosted by strong commodity exports.

- ANZ equities mixed: ASX 200 down 1.06%, NZX 50 up 0.59%, amid commodity price swings.

Yesterday's Recap

New Zealand's ANZ Business Confidence index dropped to 32.5 from 59.2, reflecting a deteriorating business outlook due to softer export demand and global uncertainties. In Australia, the RBA released its meeting minutes, highlighting ongoing inflation concerns from energy prices and labor market tightness, without indicating immediate policy changes. Australia's Ai Group Industry Index declined to -23.6 from -1.5, signaling manufacturing contraction amid higher input costs and supply disruptions.

Australian building permits rose 29.7% month-over-month preliminary, beating consensus of 6.5% and reversing the prior -7.2% drop, driven by residential construction rebound. Australia's trade balance expanded to A$5.686 billion, exceeding expectations of A$2.6 billion and the previous A$2.258 billion, supported by robust iron ore and coal exports to Asia. Markets showed mixed responses: ASX 200 fell 1.06% to 8,579.50 due to mining sector pressures, while NZX 50 gained 0.59% to 12,902.15 on dairy strength; AUD/USD slipped 0.20% to 0.69 and NZD/USD declined 0.67% to 0.57, with AUD/NZD rising 0.47% to 1.21.

BHP shares increased 4.70% to 52.76, aided by commodity recoveries despite overall equity softness.

The Day Ahead

No major data releases are scheduled for Australia or New Zealand today, providing space for markets to process yesterday's weak confidence reading and strong trade data. Focus may turn to global factors, such as Brent crude's 7.39% rise to 108.64, which could affect ANZ inflation expectations. Tomorrow also lacks key events, likely resulting in lower trading activity on ASX and NZX.

Investors will watch for impacts from USD movements on AUD and NZD crosses. News highlights upcoming RBA board speeches, potentially offering policy insights. Without domestic drivers, external commodity and FX shifts could drive volatility.

Other Economic Notes

Australia's building permits surge signals housing market recovery, but it may heighten affordability challenges in cities like Sydney and Melbourne amid tight labor markets. New Zealand's dairy exports benefit from global demand, yet currency weakness and travel disruptions pose risks to tourism. Both nations face headwinds from China's growth slowdown, a key factor for commodity trades, as seen in competitive agricultural pushes like Uganda's into Chinese markets.