ANZ Macro Daily(Beta Mode)

Markets Mixed on Oil Surge

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,579.50 | -1.06% |

| NZX 50 | 12,902.15 | +0.59% |

| AUD/USD | 0.69 | -0.29% |

| NZD/USD | 0.57 | -0.31% |

| AUD/NZD | 1.21 | +0.06% |

| BHP | 52.76 | +4.70% |

| Gold | 4,702.70 | -1.68% |

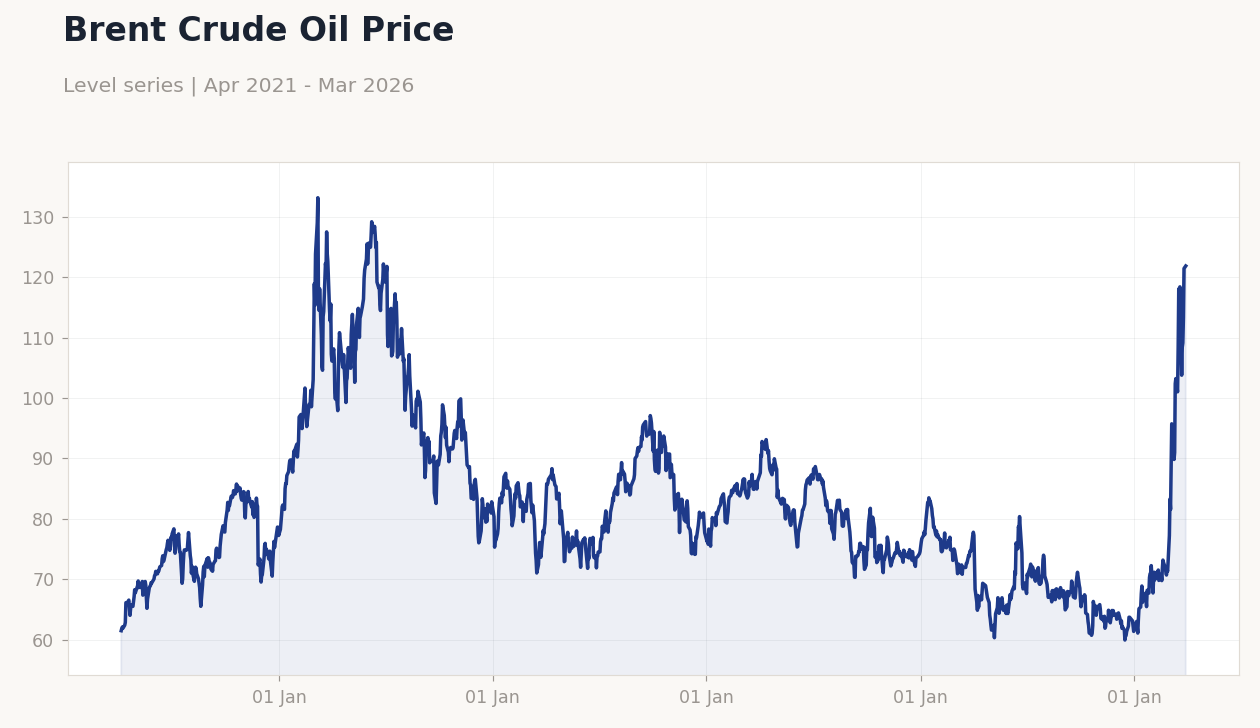

| Brent Crude | 109.05 | +7.80% |

| Bitcoin | 67,301.19 | +0.02% |

| Australia 10Y Govt Yield | 4.77% | +0.42% |

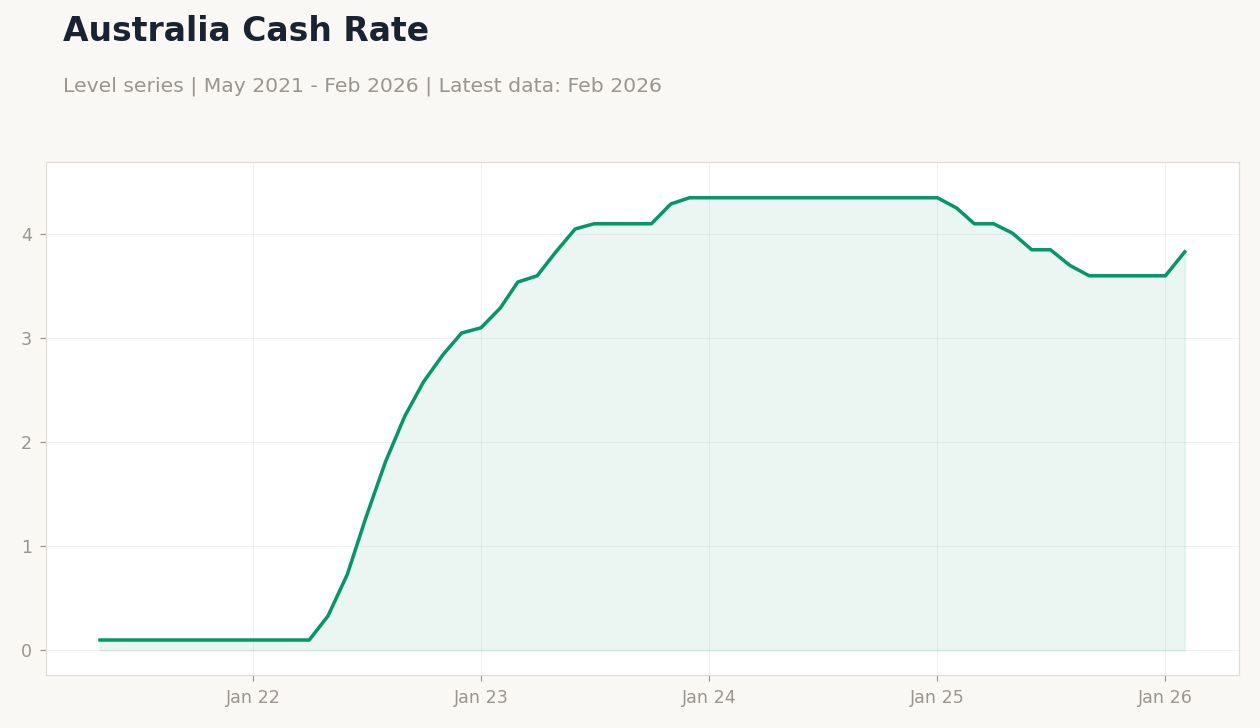

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Brent Crude Oil Price | Type: macro_line | USD per Barrel: 121.9 (2026-03-30) | Range: 59.93–133.2 | Trend(5pt): 61.47,121.8,94.46,74.58,121.9

Brent Crude Oil Price | Type: macro_line | USD per Barrel: 121.9 (2026-03-30) | Range: 59.93–133.2 | Trend(5pt): 61.47,121.8,94.46,74.58,121.9

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| RBNZ Interest Rate Decision | 2.25 | 2.25 | 22:00 |

| Business NZ PMI | 55 | - | 18:30 |

- ASX 200 fell 1.06% amid broader risk aversion, while NZX 50 gained 0.59% on dairy sector strength.

- AUD/USD and NZD/USD both weakened, down 0.29% and 0.31% respectively, pressured by USD strength.

- Brent crude surged 7.80% to $109.05, boosting miners like BHP (+4.70%) despite gold's 1.68% drop.

Yesterday's Recap

Australian equity markets softened yesterday, with the ASX 200 closing down 1.06% at 8,579.50, driven by declines in tech and consumer sectors amid global volatility. In contrast, New Zealand's NZX 50 rose 0.59% to 12,902.15, supported by gains in agricultural exporters following positive dairy trade signals. Currency movements saw AUD/USD slip 0.29% to 0.69 and NZD/USD drop 0.31% to 0.57, while AUD/NZD edged up 0.06% to 1.21, reflecting relative Australian resilience.

BHP, a key Australian mining bellwether, surged 4.70% to 52.76 on rising commodity prices, particularly Brent crude's 7.80% rally to $109.05. Gold prices fell 1.68% to 4,702.70, weighing on some Australian resource stocks. Australia's 10-year government yield rose 0.42% to 4.77%, signaling inflation concerns, while New Zealand's short-term rate dropped sharply by 9.60% to 4.33%.

No major data releases occurred in either Australia or New Zealand, but RBA reports noted easing household financial stress due to rising incomes and growing buffers.

The Day Ahead

New Zealand faces key events this week, starting with the RBNZ interest rate decision on April 7, where consensus expects the rate to hold at 2.25% amid sticky inflation. This follows recent NZD weakness, and any hawkish signals could support the currency. Later, on April 9, New Zealand's Business NZ PMI is due, with the previous reading at 55.0 indicating expansion; a dip below 50 would flag manufacturing slowdown risks.

No immediate Australian releases are scheduled, allowing focus on global cues like oil prices influencing trade balances. Markets will watch for any RBA board member speeches, as recent news highlights a break from tradition with planned public addresses. Overall, ANZ traders should monitor commodity volatility, given Australia's export reliance.

Other Economic Notes

Broader ANZ themes include Australia's vulnerability to fuel supply shocks, with experts urging long-term energy independence planning amid global disruptions. New Zealand's economy benefits from dairy resilience, but housing market linkages remain critical, tying into RBNZ policy. Household stress in Australia is easing, per RBA findings, as income growth bolsters buffers against rate pressures.

(cont...)