ANZ Macro Daily(Beta Mode)

AUD Soars on Ceasefire Hopes, RBNZ Eyed

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,579.50 | -1.06% |

| NZX 50 | 13,069.66 | +1.30% |

| AUD/USD | 0.70 | +1.24% |

| NZD/USD | 0.57 | +0.69% |

| AUD/NZD | 1.22 | +0.65% |

| BHP | 52.76 | +4.70% |

| Gold | 4,736.20 | +1.71% |

| Brent Crude | 107.24 | -2.30% |

| Bitcoin | 69,055.57 | +0.28% |

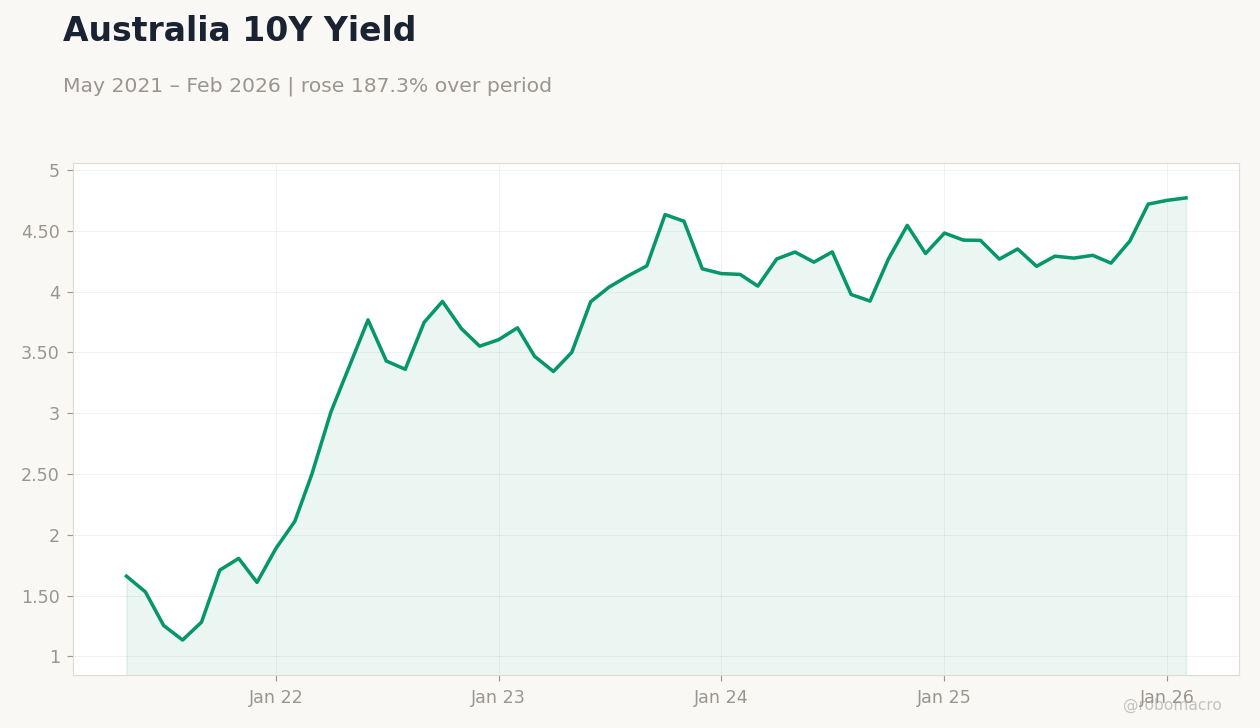

| Australia 10Y Govt Yield | 4.77% | +0.42% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

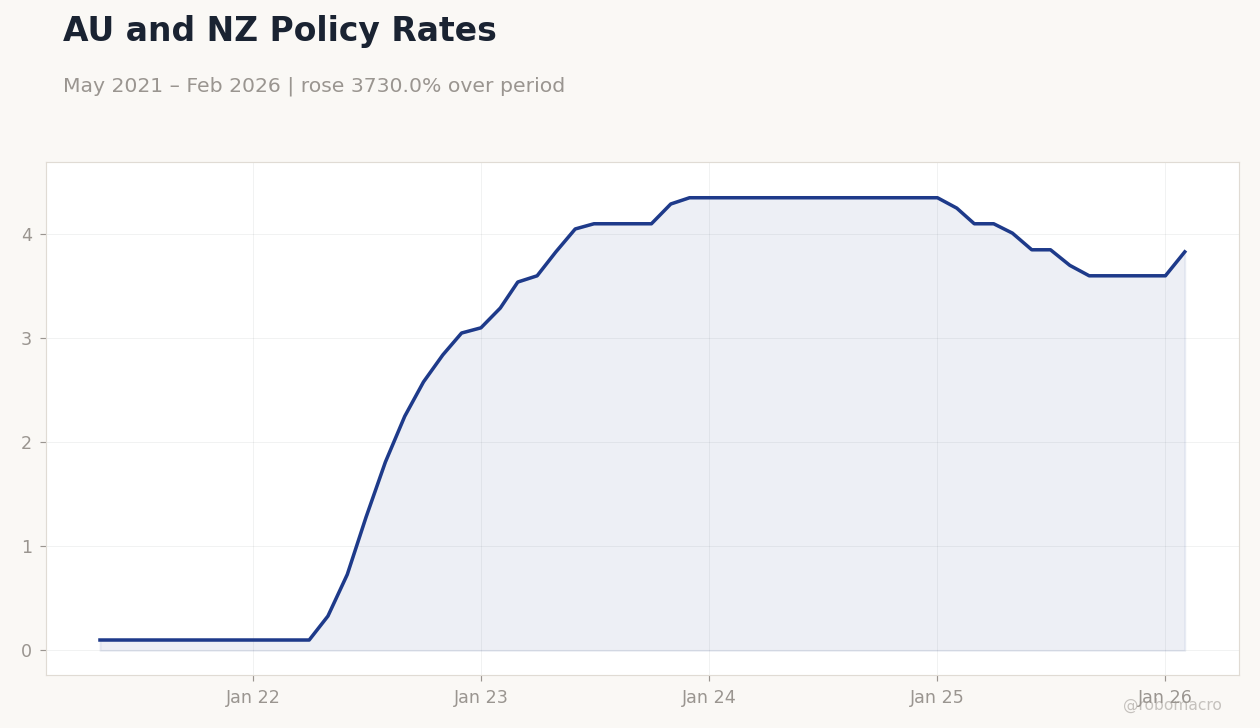

AU and NZ Policy Rates | Type: macro_line | Australia Cash Rate: 3.83 (2026-02-01) | Range: 0.1–4.35 | Trend(6pt): 0.1,1.28,4.1,4.35,3.6,3.83

AU and NZ Policy Rates | Type: macro_line | Australia Cash Rate: 3.83 (2026-02-01) | Range: 0.1–4.35 | Trend(6pt): 0.1,1.28,4.1,4.35,3.6,3.83

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| RBNZ Interest Rate Decision | 2.25 | 2.25 | 18:00 |

| Business NZ PMI | 55 | - | 14:30 |

- AUD/USD surged 1.24% to 0.70 on US-Iran ceasefire optimism, lifting Australian assets amid easing geopolitical risks.

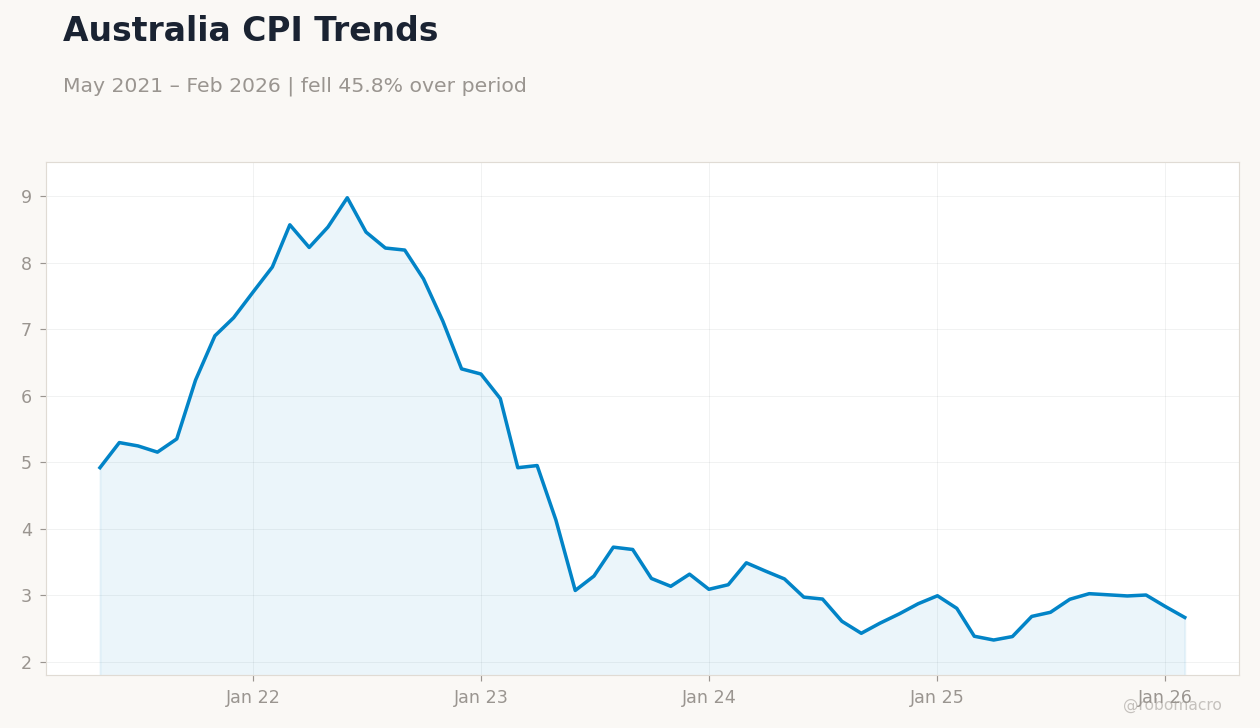

- RBA under fire for potential recession risks from extended hikes, with cycle possibly lasting into 2027.

- RBNZ poised to hold rates at 2.25%, monitoring fuel shock effects, as NZX 50 gained while ASX 200 slipped.

Yesterday's Recap

Australian equities softened with the ASX 200 down 1.06% to 8,579.50, weighed by global volatility despite BHP's 4.70% rise to 52.76 on commodity strength. New Zealand's NZX 50 climbed 1.30% to 13,069.66, buoyed by dairy and utility gains. AUD/USD advanced 1.24% to 0.70, fueled by risk-on sentiment from ceasefire hopes and RBA hike outlooks, while NZD/USD rose 0.69% to 0.57.

AUD/NZD gained 0.65% to 1.22, highlighting Australia's edge from gold's 1.71% increase to 4,736.20. Brent crude fell 2.30% to 107.24, adding pressure. Australia 10Y yield rose 0.42% to 4.77%, reflecting inflation worries, but New Zealand's short-term rate dropped 9.60% to 4.33%, signaling easing expectations.

Bitcoin edged up 0.28% to 69,055.57. No key data releases in ANZ, leaving markets attuned to external factors like Middle East developments.

The Day Ahead

RBNZ interest rate decision at 18:00 ET, with consensus for hold at 2.25% as the bank assesses fuel shock fallout. Business NZ PMI on April 9 at 14:30 ET, following prior 55.0, to gauge manufacturing amid soft dairy trends. No Australian releases, but RBA scrutiny persists on inflation and mortgages.

Investors eye RBNZ guidance for divergence from RBA's hawkish path, potentially affecting NZD. Light calendar shifts focus to global cues like China trade.

Other Economic Notes

Australia's persistent inflation drives RBA hike speculation into 2027, supported by strong commodity exports including gold and iron ore, bolstering trade surpluses. New Zealand contends with dairy weakness and tourism lags, offset partly by construction, though high rates pose risks. Housing resilience evident in Australia, with many ahead on mortgages, potentially softening RBA tightening impacts on spending.

Both economies monitor China demand, where restocking could aid Australian miners but pressure New Zealand's trade balance if dairy imports falter.