ANZ Macro Daily(Beta Mode)

RBNZ Holds Steady, Markets Surge

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,728.80 | +1.74% |

| NZX 50 | 13,253.94 | +1.41% |

| AUD/USD | 0.71 | +1.98% |

| NZD/USD | 0.58 | +2.01% |

| AUD/NZD | 1.21 | +0.05% |

| BHP | 52.76 | +4.70% |

| Gold | 4,751.40 | +2.02% |

| Brent Crude | 96.50 | -11.69% |

| Bitcoin | 71,276.29 | -0.92% |

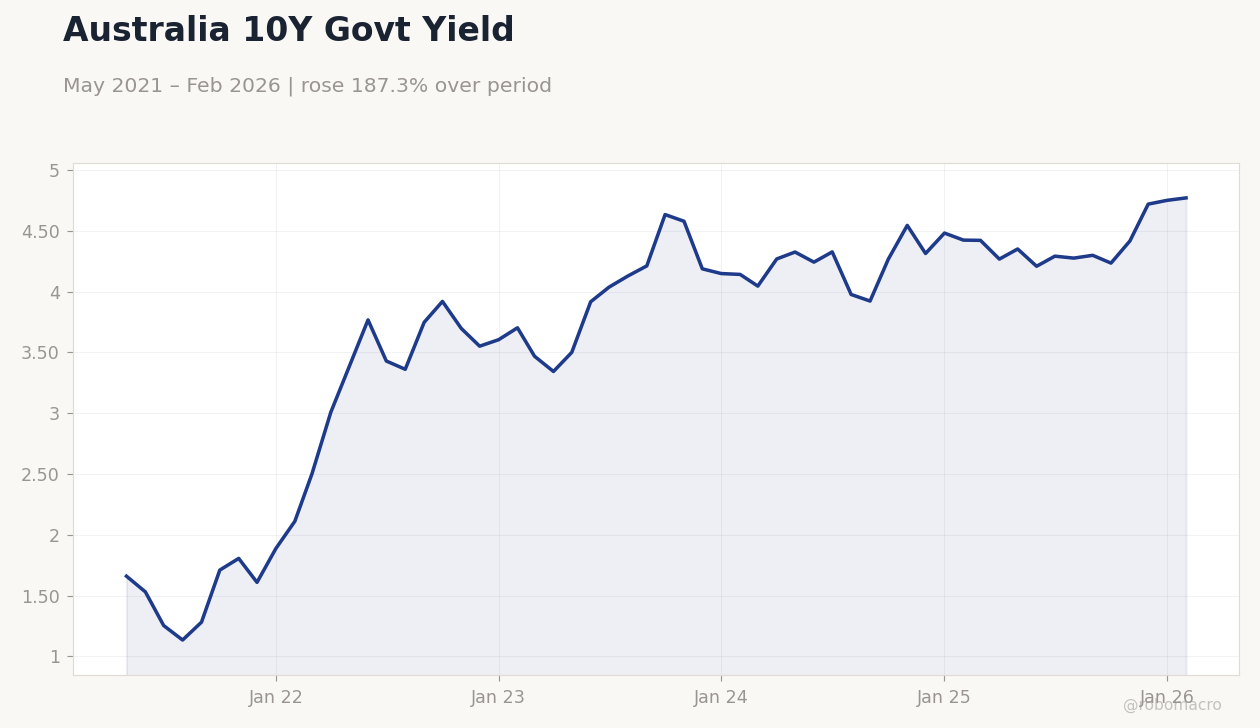

| Australia 10Y Govt Yield | 4.77% | +0.42% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| RBNZ Interest Rate Decision | 2.25 | 2.25 | 2.25 |

Australia 10Y Govt Yield | Type: macro_line | Australia 10Y Yield: 4.77 (2026-02-01) | Range: 1.135–4.77 | Trend(6pt): 1.66,3.429,4.211,4.544,4.75,4.77

Australia 10Y Govt Yield | Type: macro_line | Australia 10Y Yield: 4.77 (2026-02-01) | Range: 1.135–4.77 | Trend(6pt): 1.66,3.429,4.211,4.544,4.75,4.77

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Business NZ PMI | 55 | - | 14:30 |

| Thursday (2026-04-09) | |||

| Business NZ PMI | 55 | - | 14:30 |

- RBNZ maintains OCR at 2.25% amid inflation pressures, boosting NZD and equities.

- Australian markets rally on commodity strength despite sticky inflation concerns.

- Global oil shock weighs on sentiment, with Brent plunging amid geopolitical tensions.

Yesterday's Recap

The Reserve Bank of New Zealand (RBNZ) held its Official Cash Rate (OCR) steady at 2.25% as expected, delivering a hawkish statement that reinforced commitment to inflation targets amid mounting worries from oil price volatility. New Zealand's NZX 50 index climbed 1.41% to 13,253.94, driven by gains in export-linked sectors buoyed by the rate hold. In Australia, the ASX 200 advanced 1.74% to 8,728.80, propelled by mining stocks like BHP, which surged 4.70% to 52.76 on resilient gold prices at 4,751.40 (up 2.02%).

The AUD/USD pair strengthened 1.98% to 0.71, while NZD/USD rose 2.01% to 0.58, narrowing AUD/NZD to 1.21 (up just 0.05%). Brent crude tumbled 11.69% to 96.50, pressuring energy-exposed assets in both countries. Australia's 10-year government yield edged up 0.42% to 4.77%, reflecting inflation speculation, while New Zealand's short-term rate dropped 9.60% to 4.33%.

No major data releases occurred in Australia yesterday, but the RBNZ decision highlighted divergence in policy stances.

The Day Ahead

Attention turns to New Zealand's Business NZ PMI release tomorrow at 14:30 ET, with the previous reading at 55.0 indicating expansion; consensus is unavailable, but a slip could signal manufacturing slowdown amid dairy export weakness. No significant Australian data is scheduled today or tomorrow, allowing markets to digest global cues like oil volatility. Investors will monitor any RBA commentary on inflation, given recent headlines stoking hike speculation.

Broader ANZ events remain light, with focus shifting to potential trade flow updates from China. Expect currency volatility in AUD and NZD pairs if PMI surprises. Housing market indicators could influence sentiment indirectly through central bank watch.

Other Economic Notes

Australia's sticky inflation continues to fuel debate on RBA policy, with speculation of further rate hikes to curb demand despite resilient consumer spending, as seen in Western Australia's $9.3 billion February retail surge. New Zealand's economy faces headwinds from dairy price softness and oil shocks, potentially widening trade deficits. Broader themes include Australia's commodity-driven fiscal strength from iron ore and gold, contrasting with New Zealand's tourism and construction vulnerabilities.

(cont...)