ANZ Macro Daily(Beta Mode)

RBNZ Holds Steady, Aus-NZ Markets Rise

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,951.80 | +2.55% |

| NZX 50 | 13,273.81 | +0.15% |

| AUD/USD | 0.71 | +0.12% |

| NZD/USD | 0.59 | +0.91% |

| AUD/NZD | 1.21 | -0.76% |

| BHP | 54.56 | +0.06% |

| Gold | 4,794.80 | +0.95% |

| Brent Crude | 97.25 | +2.64% |

| Bitcoin | 72,090.48 | +1.36% |

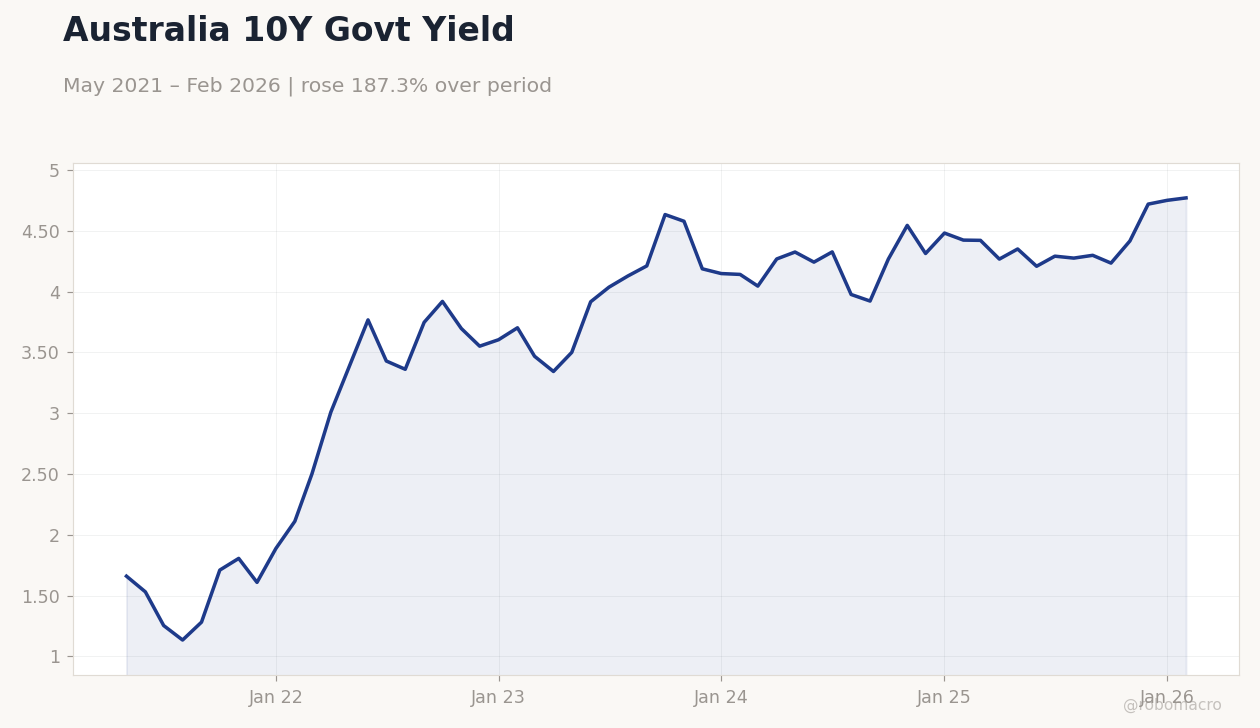

| Australia 10Y Govt Yield | 4.77% | +0.42% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| RBNZ Interest Rate Decision | 2.25 | 2.25 | 2.25 |

Australia 10Y Govt Yield | Type: macro_line | AU 10Y Yield (%): 4.77 (2026-02-01) | Range: 1.135–4.77 | Trend(6pt): 1.66,3.429,4.211,4.544,4.75,4.77

Australia 10Y Govt Yield | Type: macro_line | AU 10Y Yield (%): 4.77 (2026-02-01) | Range: 1.135–4.77 | Trend(6pt): 1.66,3.429,4.211,4.544,4.75,4.77

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Business NZ PMI | 55 | - | 14:30 |

- RBNZ keeps Official Cash Rate at 2.25%, emphasizing inflation control amid oil pressures.

- ASX 200 surges 2.55% on commodity gains, NZX 50 edges up 0.15%.

- AUD/NZD falls 0.76% as RBNZ stance strengthens Kiwi versus Aussie dollar.

Yesterday's Recap

The Reserve Bank of New Zealand (RBNZ) held its Official Cash Rate steady at 2.25% in a high-impact decision, meeting consensus expectations and reinforcing commitment to inflation targets despite oil shock pressures. New Zealand's NZX 50 index closed at 13,273.81, up 0.15% on the day, supported by dairy sector gains amid global commodity optimism. Australia's ASX 200 advanced strongly to 8,951.80, marking a 2.55% daily gain driven by mining stocks like BHP, which rose 0.06% to 54.56.

The NZD/USD pair strengthened 0.91% to 0.59, reflecting RBNZ's hawkish hold, while AUD/USD edged up 0.12% to 0.71. Cross-rate AUD/NZD fell 0.76% to 1.21, highlighting relative Kiwi resilience. New Zealand's short-term rate dropped sharply by 9.60% to 4.33%, signaling market repricing of policy expectations.

Australia's 10-year government yield rose 0.42% to 4.77%, amid persistent inflation concerns.

The Day Ahead

New Zealand's Business NZ PMI for March is due at 14:30 ET, with the previous reading at 55.0 indicating expansion; a slip below 50 could signal manufacturing weakness amid high rates and oil volatility. No major Australian data releases are scheduled, allowing markets to digest recent RBA commentary on potential hikes. Attention will focus on any RBNZ follow-up statements post-decision, potentially influencing NZD dynamics.

Broader ANZ sentiment may track global commodity moves, especially iron ore and dairy prices. Traders eye upcoming Australian fuel supply developments from the PM's Singapore visit for energy sector implications.

Other Economic Notes

Australia's economy faces recession risks as persistent inflation prompts RBA hike considerations, with Westpac warning of further tightening needs. New Zealand's dairy-driven exports benefit from global price rebounds, but housing consents remain weak under elevated rates. Both nations' trade linkages to China amplify sensitivity to Beijing's growth outlook, with commodity exporters like BHP serving as key sentiment gauges.

Fuel supply security emerges as a theme, with PM Albanese's efforts to bolster imports addressing Australia's vulnerability. (cont...)