ANZ Macro Daily(Beta Mode)

NZ PMI Dips, RBA Speeches Ahead

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,960.60 | -0.14% |

| NZX 50 | 13,181.44 | -0.70% |

| AUD/USD | 0.71 | -0.19% |

| NZD/USD | 0.58 | -0.22% |

| AUD/NZD | 1.21 | +0.01% |

| BHP | 53.98 | -1.06% |

| Gold | 4,761.90 | -0.63% |

| Brent Crude | 95.20 | -0.75% |

| Bitcoin | 73,664.77 | +0.94% |

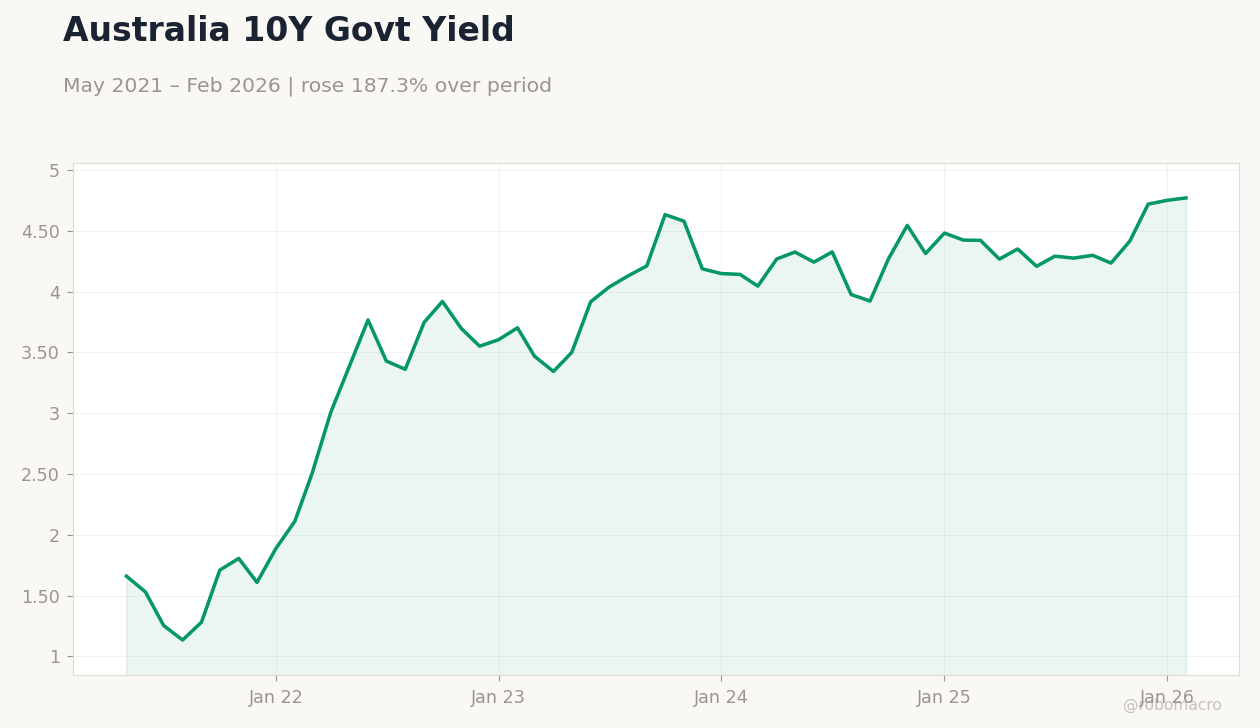

| Australia 10Y Govt Yield | 4.77% | +0.42% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Business NZ PMI | 54.80 | - | 53.20 |

Australia Unemployment Rate | Type: macro_line | Unemployment Rate (%): 4.075 (2026-01-01) | Range: 3.431–5.231 | Trend(5pt): 5.11,3.453,3.563,3.923,4.075

Australia Unemployment Rate | Type: macro_line | Unemployment Rate (%): 4.075 (2026-01-01) | Range: 3.431–5.231 | Trend(5pt): 5.11,3.453,3.563,3.923,4.075

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| RBA Hauser Speech | - | - | 18:15 |

| Westpac Consumer Confidence Change | 1.20 | - | 20:30 |

| Westpac Consumer Confidence Index | 91.60 | - | 20:30 |

| NAB Business Confidence Index | -1 | - | 21:30 |

| RBA Hauser Speech | - | - | 16:00 |

| Employment Change | 48,900 | 20,000 | 21:30 |

| Full-Time Employment Change | -30,500 | - | 21:30 |

| Headline Unemployment Rate | 4.30 | 4.30 | 21:30 |

| RBA Hunter Speech | - | - | 14:30 |

- New Zealand's Business NZ PMI fell to 53.2, indicating softening manufacturing amid weaker exports and supply issues.

- Australian markets dipped slightly, with ASX 200 down 0.14% to 8,960.60 and AUD/USD at 0.71 after a 0.19% decline.

- RBA speeches and key data like consumer confidence and employment loom, spotlighting inflation and rate hike bets.

Yesterday's Recap

New Zealand's Business NZ PMI declined to 53.2 from 54.8, reflecting slower manufacturing growth due to reduced export demand and ongoing supply chain challenges. The NZX 50 index fell 0.70% to 13,181.44, influenced by concerns over tourism and dairy volatility. Australian equities also softened, with the ASX 200 down 0.14% to 8,960.60, driven by mining weakness including BHP's 1.06% drop to 53.98.

Currency moves included AUD/USD slipping 0.19% to 0.71 and NZD/USD down 0.22% to 0.58, while AUD/NZD rose 0.01% to 1.21, highlighting Australia's relative strength. Commodities weakened, with gold at 4,761.90 off 0.63% and Brent crude at 95.20 down 0.75%, pressuring export sectors. Australia's 10-year government yield increased 0.42% to 4.77%, amid inflation expectations, while New Zealand's short-term rate dropped 9.60% to 4.33% on easing prospects.

These developments underscored economic divergence, with Australia's commodity exposure mitigating losses compared to New Zealand's data softness.

The Day Ahead

Australia's calendar features several high-impact events. RBA Deputy Governor Hauser speaks at 18:15 ET on April 13, potentially addressing inflation and policy direction. Westpac Consumer Confidence follows at 20:30 ET, with prior change at 1.2% and index at 91.6, assessing household sentiment amid cost pressures.

NAB Business Confidence Index is due at 21:30 ET, after a previous -1 reading, gauging corporate views in a tight rate environment. Another Hauser speech occurs April 14 at 16:00 ET, which may elaborate on economic resilience. Labor market data arrives April 15 at 21:30 ET, including employment change consensus of 20,000 versus prior 48,900, full-time change from -30,500, and unemployment rate expected at 4.3%.

RBA Assistant Governor Hunter speaks April 16 at 14:30 ET, likely covering commodity and housing dynamics. These releases could influence rate expectations and market sentiment.

Other Economic Notes

Australian property prices are still rising in most suburbs despite rate concerns, bolstered by migration and limited supply, though further RBA tightening might strain affordability. (cont...)