ANZ Macro Daily(Beta Mode)

AUD Surges on RBA Hike Bets

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,960.60 | -0.14% |

| NZX 50 | 13,181.44 | -0.70% |

| AUD/USD | 0.70 | -0.85% |

| NZD/USD | 0.58 | -0.42% |

| AUD/NZD | 1.20 | -0.73% |

| BHP | 53.98 | -1.06% |

| Gold | 4,787.40 | -0.10% |

| Brent Crude | 95.20 | -0.75% |

| Bitcoin | 71,109.82 | -2.66% |

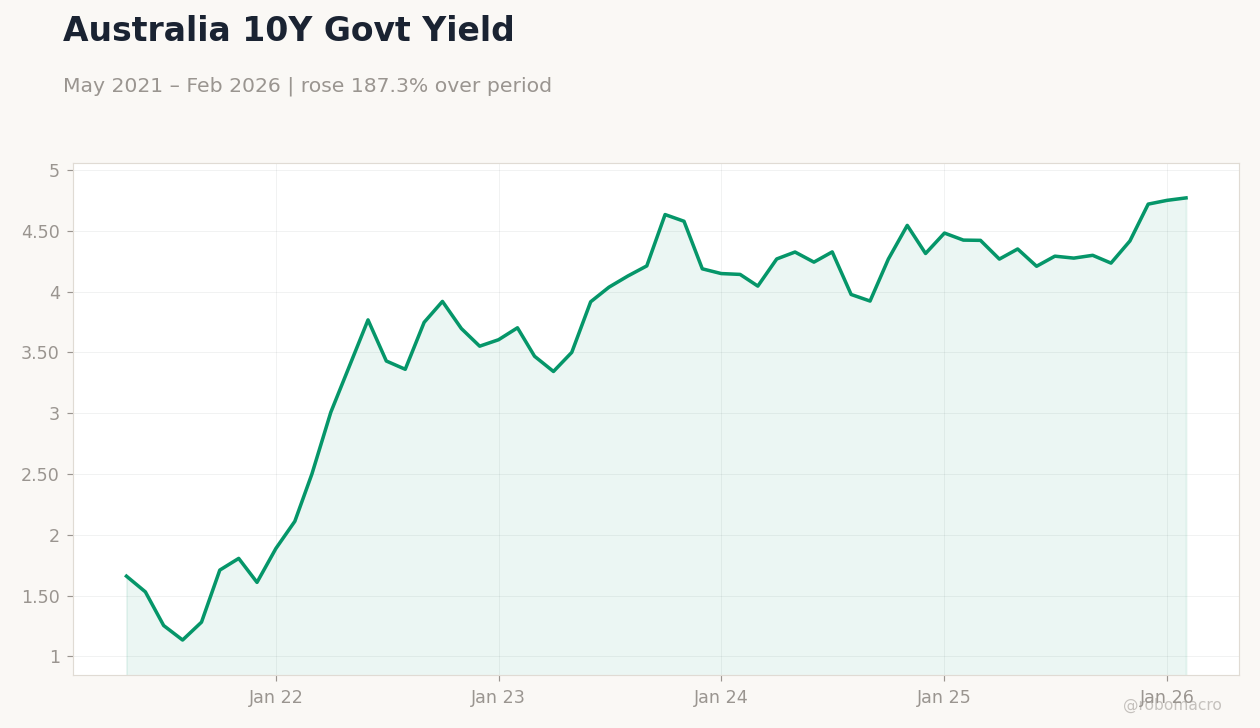

| Australia 10Y Govt Yield | 4.77% | +0.42% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Brent Crude Oil Price | Type: macro_line | Brent Price (USD): 127.6 (2026-04-02) | Range: 59.93–133.2 | Trend(6pt): 62.83,114,87.86,76.72,126.7,127.6

Brent Crude Oil Price | Type: macro_line | Brent Price (USD): 127.6 (2026-04-02) | Range: 59.93–133.2 | Trend(6pt): 62.83,114,87.86,76.72,126.7,127.6

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| RBA Hauser Speech | - | - | 18:15 |

| Westpac Consumer Confidence Change | 1.20 | - | 20:30 |

| Westpac Consumer Confidence Index | 91.60 | - | 20:30 |

| NAB Business Confidence Index | -1 | - | 21:30 |

| RBA Hauser Speech | - | - | 16:00 |

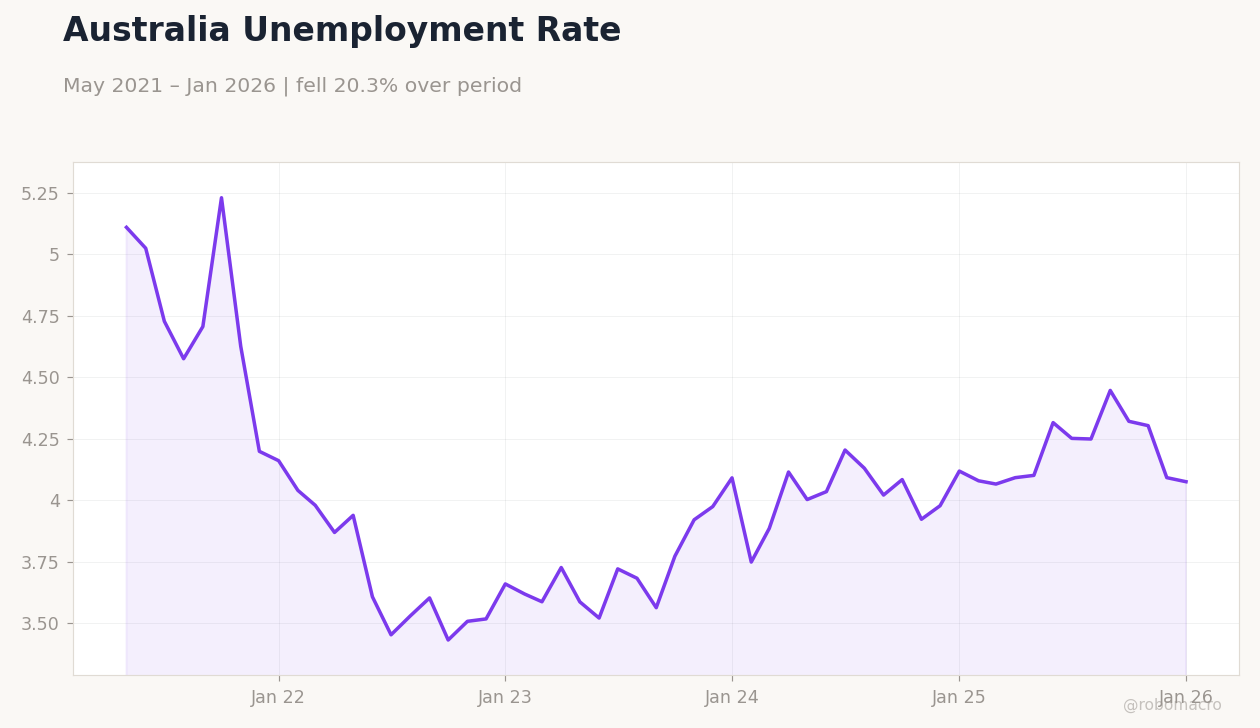

| Employment Change | 48,900 | 20,000 | 21:30 |

| Full-Time Employment Change | -30,500 | - | 21:30 |

| Headline Unemployment Rate | 4.30 | 4.30 | 21:30 |

| RBA Hunter Speech | - | - | 14:30 |

| Trade Balance | -257m | - | 18:45 |

- AUD hits 3-year highs amid RBA rate hike expectations and commodity strength, pressuring NZD.

- Equity markets dip on softer commodities, with ASX 200 and NZX 50 down modestly.

- RBA speeches and jobs data loom, highlighting persistent inflation risks in Australia.

Yesterday's Recap

Australian equity markets softened yesterday, with the ASX 200 closing at 8,960.60 after a 0.14% decline, driven by weakness in mining stocks like BHP, which fell 1.06% to 53.98 amid sliding commodity prices. New Zealand's NZX 50 dropped 0.70% to 13,181.44, reflecting dairy sector pressures and broader risk-off sentiment. The AUD/USD pair weakened 0.85% to 0.70, while NZD/USD eased 0.42% to 0.58, with the AUD/NZD cross falling 0.73% to 1.20 as Australian dollar resilience outpaced its Kiwi counterpart.

Commodity moves weighed on both economies, with Brent crude down 0.75% to 95.20 and gold slipping 0.10% to 4,787.40, underscoring Australia's exposure to energy and metals exports. Australia's 10-year government yield rose 0.42% to 4.77%, signaling hawkish bets, while New Zealand's short-term rate fell 9.60% to 4.33%, hinting at divergent policy paths. No major data releases occurred in either Australia or New Zealand, allowing markets to focus on global cues like US dollar strength.

Bitcoin's 2.66% drop to 71,109.82 added to volatile sentiment affecting ANZ crypto-linked investments.

The Day Ahead

Australian markets will watch the RBA Hauser speech at 18:15 ET for insights into rate paths, followed by Westpac Consumer Confidence data at 20:30 ET, where the change is eyed after a prior 1.2% rise and the index at 91.6. NAB Business Confidence at 21:30 ET could signal corporate sentiment following the previous -1 reading. Another RBA Hauser speech at 16:00 ET tomorrow may reinforce monetary signals, while employment figures on April 15 at 21:30 ET are forecast at 20,000 job gains and a steady 4.3% unemployment rate.

Full-time employment changes, previously at -30,500, will be scrutinized for labor market health. RBA Hunter's speech on April 16 at 14:30 ET rounds out the week, potentially addressing inflation persistence. New Zealand's trade balance on April 19 at 18:45 ET follows a prior -257 million deficit, impacting export-driven growth.

Other Economic Notes

Australia's commodity boom, fueled by iron ore and LNG exports to China, supports AUD strength but exposes the economy to Beijing's slowdown risks, with news warning of potential 2026 collapse if inflation persists. (cont...)