ANZ Macro Daily(Beta Mode)

RBA Warns on Stagflation, AUD Rebounds

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,926.00 | -0.39% |

| NZX 50 | 13,017.26 | -0.02% |

| AUD/USD | 0.71 | +1.52% |

| NZD/USD | 0.59 | +1.72% |

| AUD/NZD | 1.21 | -0.18% |

| BHP | 56.01 | +3.05% |

| Gold | 4,866.70 | +2.62% |

| Brent Crude | 95.16 | -4.23% |

| Bitcoin | 74,254.72 | -0.31% |

| Australia 10Y Govt Yield | 4.77% | +0.42% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| RBA Hauser Speech | - | - | - |

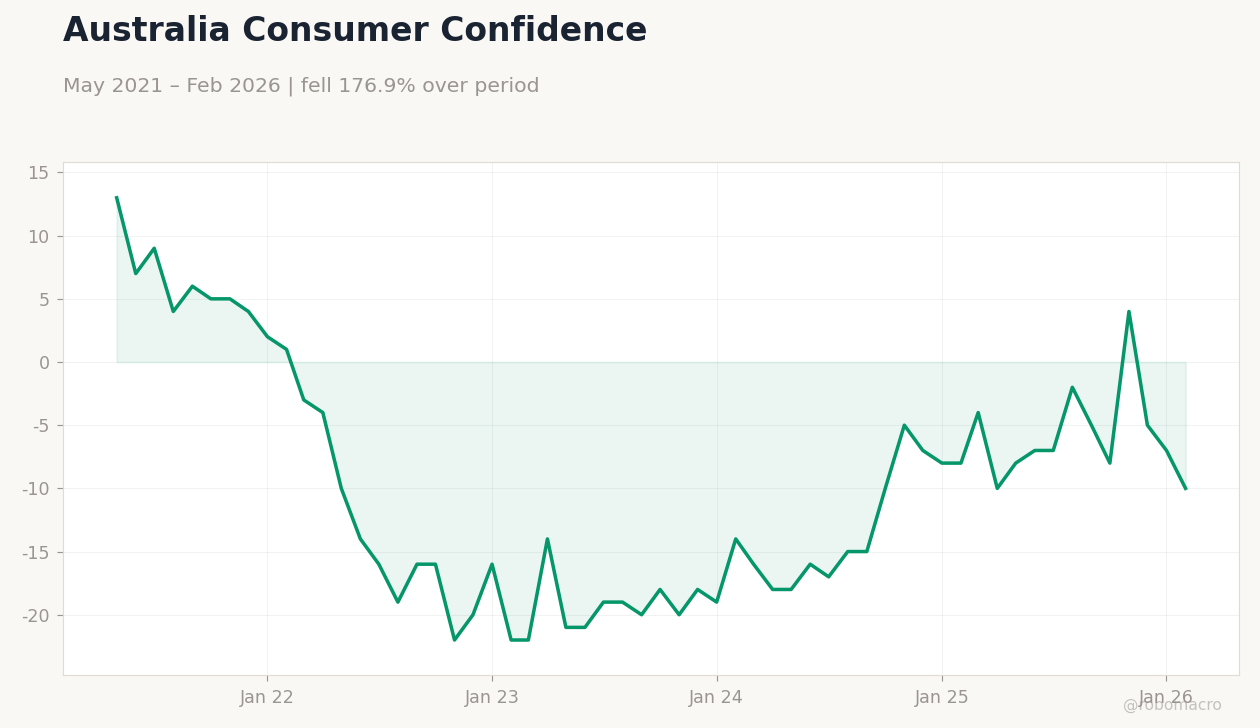

| Westpac Consumer Confidence Change | 1.20 | - | -12.50 |

| Westpac Consumer Confidence Index | 91.60 | - | 80.10 |

| NAB Business Confidence Index | -1 | - | -29 |

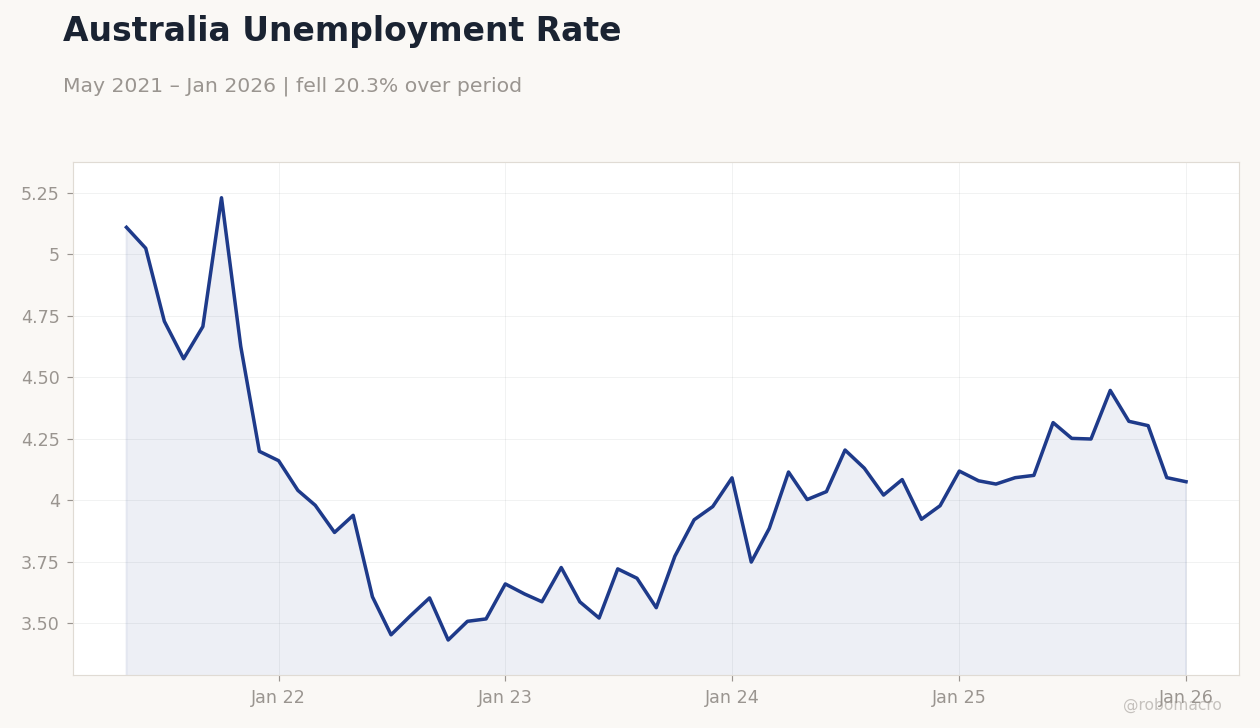

Australia Unemployment Rate | Type: macro_line | AU Unemployment %: 4.075 (2026-01-01) | Range: 3.431–5.231 | Trend(5pt): 5.11,3.453,3.563,3.923,4.075

Australia Unemployment Rate | Type: macro_line | AU Unemployment %: 4.075 (2026-01-01) | Range: 3.431–5.231 | Trend(5pt): 5.11,3.453,3.563,3.923,4.075

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| RBA Hauser Speech | - | - | 16:00 |

| Employment Change | 48,900 | 20,000 | 21:30 |

| Full-Time Employment Change | -30,500 | - | 21:30 |

| Headline Unemployment Rate | 4.30 | 4.30 | 21:30 |

| RBA Hunter Speech | - | - | 14:30 |

| Trade Balance | -257m | - | 18:45 |

| Inflation Rate Quarter-over-Quarter | 0.60 | - | 18:45 |

- RBA Deputy Governor Hauser highlighted stagflation risks from energy shocks and weak consumer sentiment, weighing on AUD despite a rebound.

- Australian consumer and business confidence dropped sharply, pointing to economic slowdown, with equities slightly lower amid mixed market moves.

- Improved global risk mood from US-Iran deal hopes lifted AUD and NZD, though commodity fluctuations and geopolitics add uncertainty.

Yesterday's Recap

Yesterday, RBA Deputy Governor Hauser's speech emphasized stagflation risks from energy shocks impacting the economy, with persistent inflation and slowing growth. Westpac Consumer Confidence Change in Australia fell to -12.5 from 1.2 previously, and the Index dropped to 80.1 from 91.6, driven by cost-of-living concerns. NAB Business Confidence Index plunged to -29 from -1, reflecting deep business pessimism amid challenges.

No key New Zealand data emerged, shifting attention to Australian indicators that fueled market caution. ASX 200 ended at 8,926.00, down 0.39%, pressured by risk aversion but supported by mining gains like BHP at 56.01 (+3.05%). NZX 50 closed at 13,017.26, down 0.02%, resilient despite commodity softness.

AUD/USD climbed to 0.71 (+1.52%) and NZD/USD to 0.59 (+1.72%), aided by better risk sentiment, while AUD/NZD fell to 1.21 (-0.18%).

The Day Ahead

Today includes RBA Hauser speech at 16:00 ET, which may echo stagflation worries and shape rate outlooks. Tomorrow features Australia's Employment Change at 21:30 ET, consensus 20,000 after 48,900 prior, plus Full-Time Employment Change and Headline Unemployment Rate expected at 4.3%. RBA Hunter speech follows on April 16 at 14:30 ET, offering policy clues amid labor data.

New Zealand Trade Balance arrives April 19 at 18:45 ET, after -257 million previously, highlighting export trends in dairy and commodities. NZ Inflation Rate Quarter-over-Quarter releases April 20 at 18:45 ET, following 0.6% prior, key for RBNZ inflation goals. These events emphasize Australia's jobs focus and New Zealand's trade-inflation balance, likely influencing currencies.

Other Economic Notes

ANZ economies face commodity exposure, with Australia's iron ore and coal hit by China's mixed recovery, offset partly by gold at 4,866.70 (+2.62%) aiding miners like BHP. New Zealand's dairy sector sees steady demand, including kiwifruit exports, but contends with tourism and construction weakness. Housing in both nations reacts to rates, with Australian credit potentially slowing on confidence falls, and New Zealand's market tied to migration.

(cont...)