ANZ Macro Daily(Beta Mode)

RBA Flags Stagflation Risk as Sentiment Plunges

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,970.80 | +0.50% |

| NZX 50 | 13,076.58 | +0.46% |

| AUD/USD | 0.72 | +1.06% |

| NZD/USD | 0.59 | +0.78% |

| AUD/NZD | 1.21 | -0.03% |

| BHP | 55.87 | -0.41% |

| Gold | 4,822.50 | -0.05% |

| Brent Crude | 94.77 | -0.02% |

| Bitcoin | 74,975.14 | +1.07% |

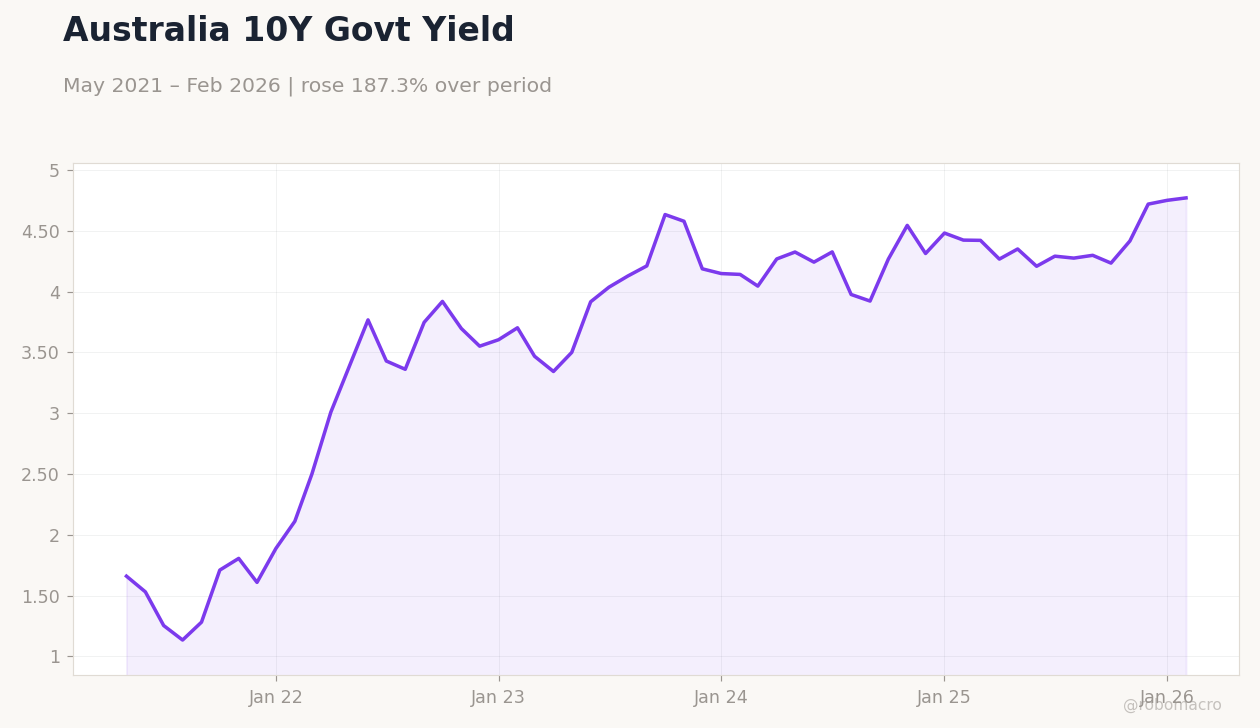

| Australia 10Y Govt Yield | 4.77% | +0.42% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| RBA Hauser Speech | - | - | - |

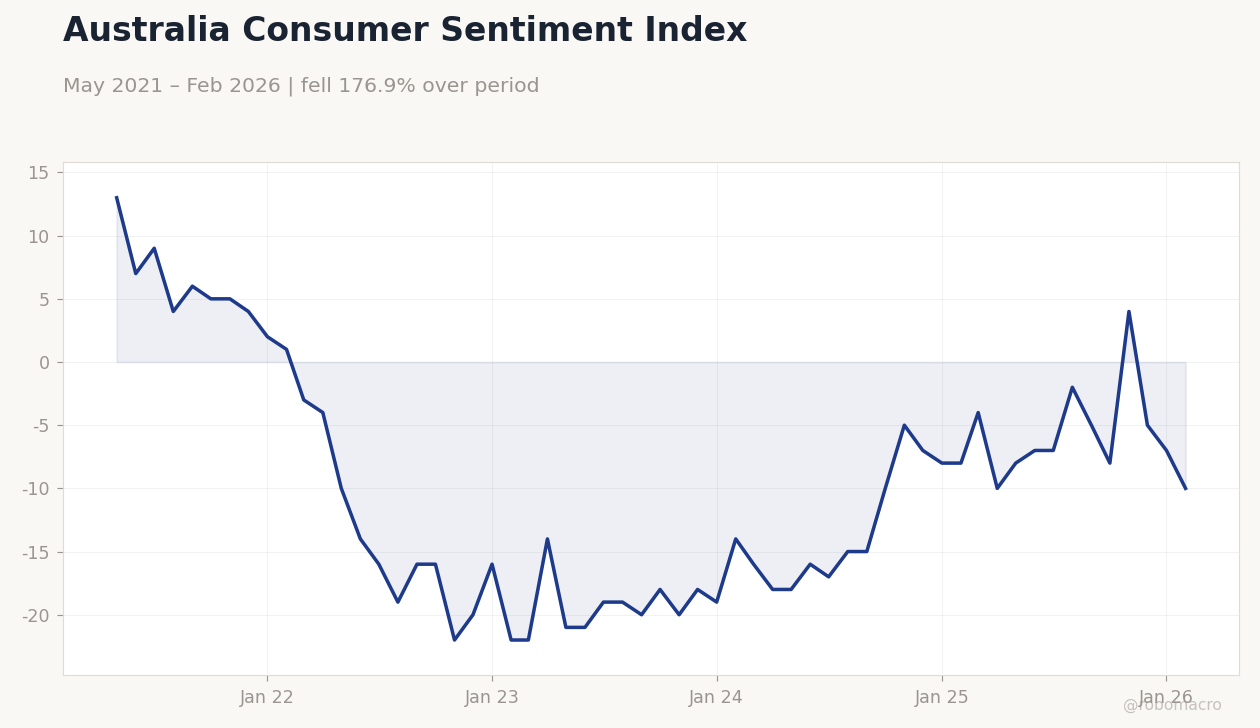

| Westpac Consumer Confidence Change | 1.20 | - | -12.50 |

| Westpac Consumer Confidence Index | 91.60 | - | 80.10 |

| NAB Business Confidence Index | 0 | - | -29 |

| RBA Hauser Speech | - | - | - |

Australia Consumer Sentiment Index | Type: macro_line | Index: -10 (2026-02-01) | Range: -22–13 | Trend(6pt): 13,-16,-20,-5,-7,-10

Australia Consumer Sentiment Index | Type: macro_line | Index: -10 (2026-02-01) | Range: -22–13 | Trend(6pt): 13,-16,-20,-5,-7,-10

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Employment Change | 48,900 | 20,000 | 17:30 |

| Full-Time Employment Change | -30,500 | - | 17:30 |

| Headline Unemployment Rate | 4.30 | 4.30 | 17:30 |

| RBA Hunter Speech | - | - | 10:30 |

| Trade Balance | -257m | - | 14:45 |

- Australian consumer and business confidence fell sharply, amplifying RBA warnings of persistent inflation amid weakening growth.

- AUD/USD and NZD/USD rose on global risk appetite, with ASX 200 and NZX 50 posting modest gains despite domestic pessimism.

- RBA speeches underscored stagflation concerns, dominating the ANZ macro landscape ahead of key employment data.

Yesterday's Recap

Australian indicators showed sharp declines in sentiment, with the Westpac Consumer Confidence Index dropping to 80.1 from 91.6, a -12.5% change, driven by inflation fears and rate hike prospects. The NAB Business Confidence Index plunged to -29 from 0, reflecting business worries over slowing activity and cost pressures. RBA Deputy Governor Hauser gave speeches highlighting risks of high inflation persisting with low growth.

Equity markets advanced slightly, with the ASX 200 up 0.50% to 8,970.80, aided by commodity support, and the NZX 50 rising 0.46% to 13,076.58. Currencies strengthened, with AUD/USD climbing 1.06% to 0.72 and NZD/USD up 0.78% to 0.59, while AUD/NZD dipped -0.03% to 1.21. BHP shares fell -0.41% to 55.87.

Gold eased -0.05% to 4,822.50, Brent crude slipped -0.02% to 94.77, and Bitcoin gained 1.07% to 74,975.14. Australia's 10Y government yield rose 0.42% to 4.77%, and New Zealand's short-term rate dropped -9.60% to 4.33%. No significant New Zealand data emerged, keeping focus on Australia's softening metrics and regional trade ties.

The Day Ahead

Today's key release is Australian employment data at 17:30 ET, with consensus for a 20,000 job increase after February's 48,900 gain, and the unemployment rate holding at 4.3%. Full-time employment change, previously -30,500, will be watched for labor market strength amid economic slowdown. An RBA speech by Assistant Governor Hunter is set for tomorrow at 10:30 ET, offering potential guidance on inflation and policy.

New Zealand's trade balance, last at -257 million, is due later this week on April 19 at 14:45 ET, providing insights into export trends in dairy and other sectors. These events could sway AUD and NZD, particularly with commodity demand from China influencing ANZ terms of trade.

Other Economic Notes

Australia's housing sector faces strains from elevated rates, worsening affordability and tying into broader consumer weakness. New Zealand's economy, reliant on dairy, contends with soft global prices that may expand trade deficits and weigh on NZD. Fertilizer supply issues in Australia, with prices up 60%, highlight import vulnerabilities and could spur local manufacturing growth to enhance self-sufficiency.