Yesterday's Recap

New Zealand's inflation rate for Q1 came in at 0.9% quarter-over-quarter, surpassing the consensus estimate of 0.8% and the previous 0.6%, highlighting ongoing domestic price pressures driven by housing and food costs. This hotter-than-expected print boosted the NZD/USD by 0.48% to 0.59, reflecting market bets on a more aggressive RBNZ stance. In Australia, no major data releases occurred, but equity markets saw modest gains with the ASX 200 closing at 8,953.30, up 0.07%, supported by mining sector stability despite BHP shares dipping 0.66% to 55.32.

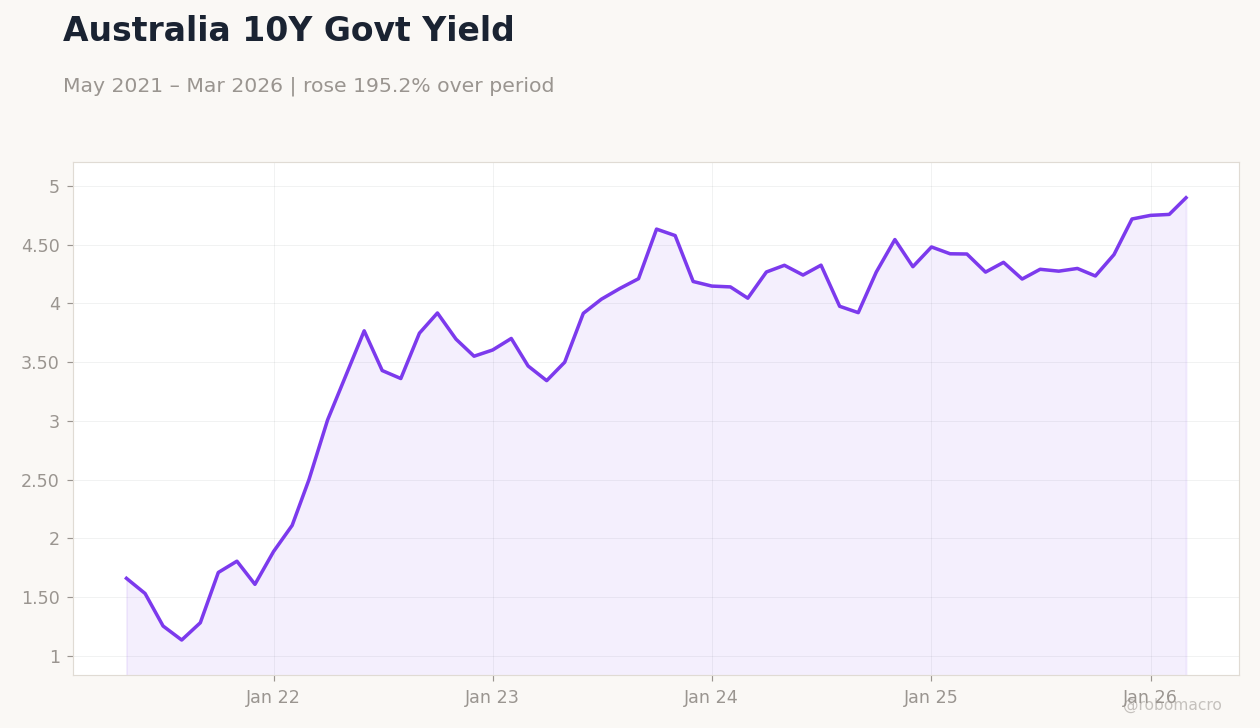

The AUD/USD rose 0.23% to 0.72, aided by commodity tailwinds, while AUD/NZD fell 0.13% to 1.21 as NZD outperformed. New Zealand's NZX 50 advanced 0.08% to 12,915.45, buoyed by export-oriented firms amid positive China trade news. Bond markets weakened, with Australia's 10Y government yield jumping 2.98% to 4.90%, signaling inflation concerns, while New Zealand's short-term rate dropped 9.60% to 4.33% on mixed rate expectations.

Commodities pressured sentiment, with gold falling 1.42% to 4,738.50 and Brent crude declining 1.70% to 93.86, impacting Australia's export outlook.

The Day Ahead

Australia's S&P Global Manufacturing PMI Flash for April is due at 15:00 ET on April 22, with the previous reading at 49.8 indicating contraction; a further slip could heighten recession fears amid slowing China demand for commodities. The S&P Global Services PMI Flash, previously at 46.3, will also release at the same time, offering insights into the dominant services sector's health, where weakness might pressure the RBA's growth projections. No major New Zealand data is scheduled, leaving markets to digest yesterday's inflation beat and global risk sentiment.

Investors will watch for any RBA speeches or commentary on stagflation risks, potentially influencing AUD volatility. Broader ANZ events include monitoring China-Australia trade developments, such as new beef export licences, which could support agricultural sentiment in both countries. Overall, the PMIs will be key for gauging divergence in Australia and New Zealand's economic trajectories.

Brent Crude Oil Prices | Type: macro_line | Brent USD/Barrel: 123.3 (2026-04-13) | Range: 59.93–138.2 | Trend(5pt): 65.07,115,92.52,82.39,123.3

Brent Crude Oil Prices | Type: macro_line | Brent USD/Barrel: 123.3 (2026-04-13) | Range: 59.93–138.2 | Trend(5pt): 65.07,115,92.52,82.39,123.3