ANZ Macro Daily(Beta Mode)

RBA Hikes Rates in Split as Inflation Fears Mount

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,786.50 | -0.08% |

| NZX 50 | 12,874.94 | -0.08% |

| AUD/USD | 0.71 | +0.02% |

| NZD/USD | 0.59 | +0.46% |

| AUD/NZD | 1.21 | -0.50% |

| BHP | 56.10 | +0.12% |

| Gold | 4,740.90 | +0.76% |

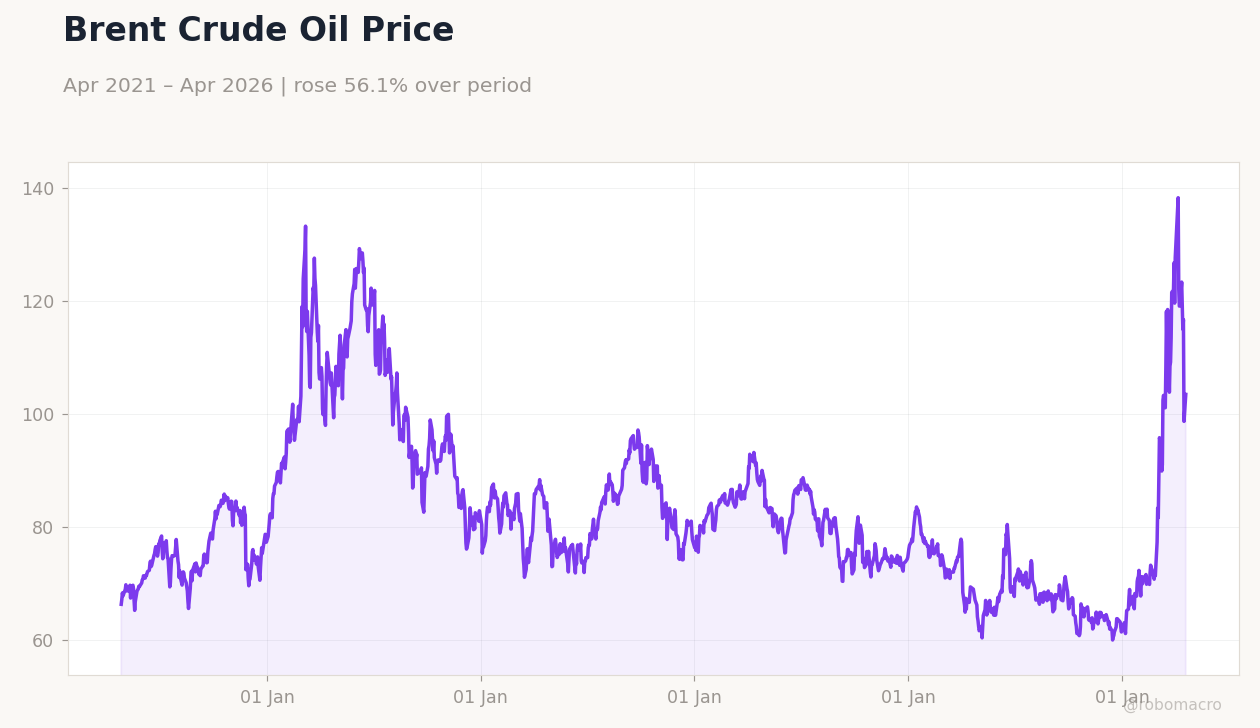

| Brent Crude | 99.13 | -5.65% |

| Bitcoin | 78,271.59 | +0.85% |

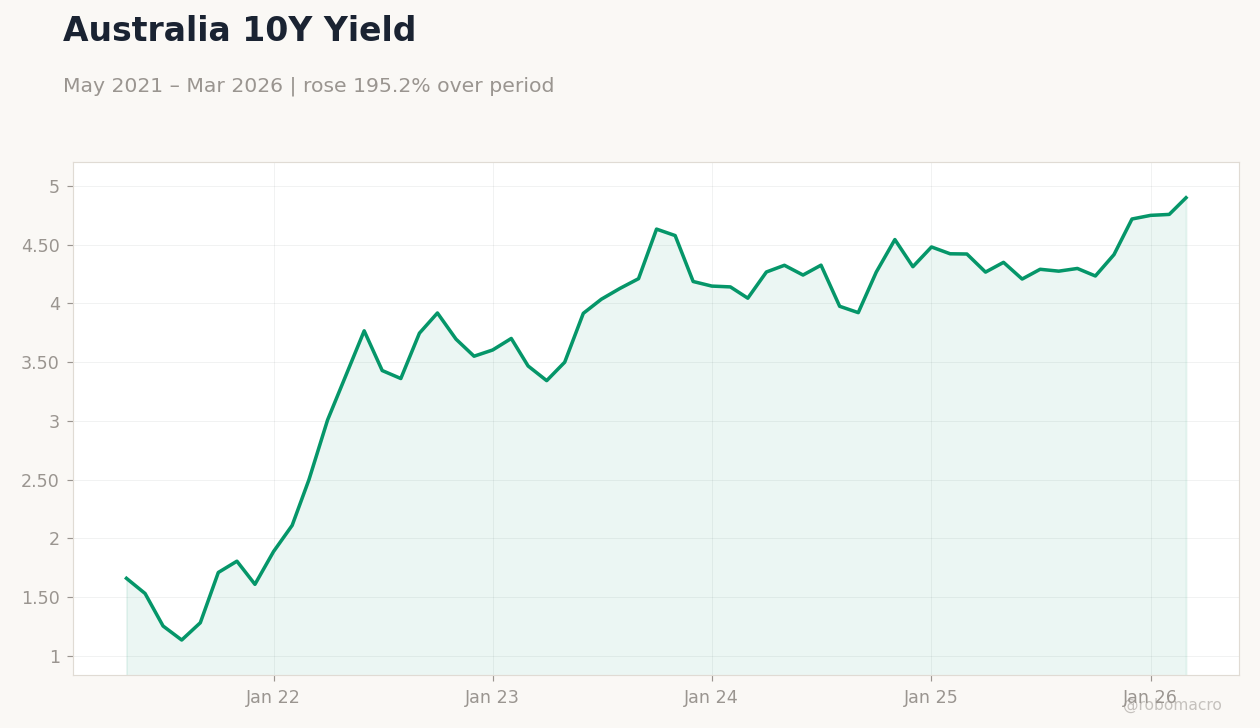

| Australia 10Y Govt Yield | 4.90% | +2.98% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

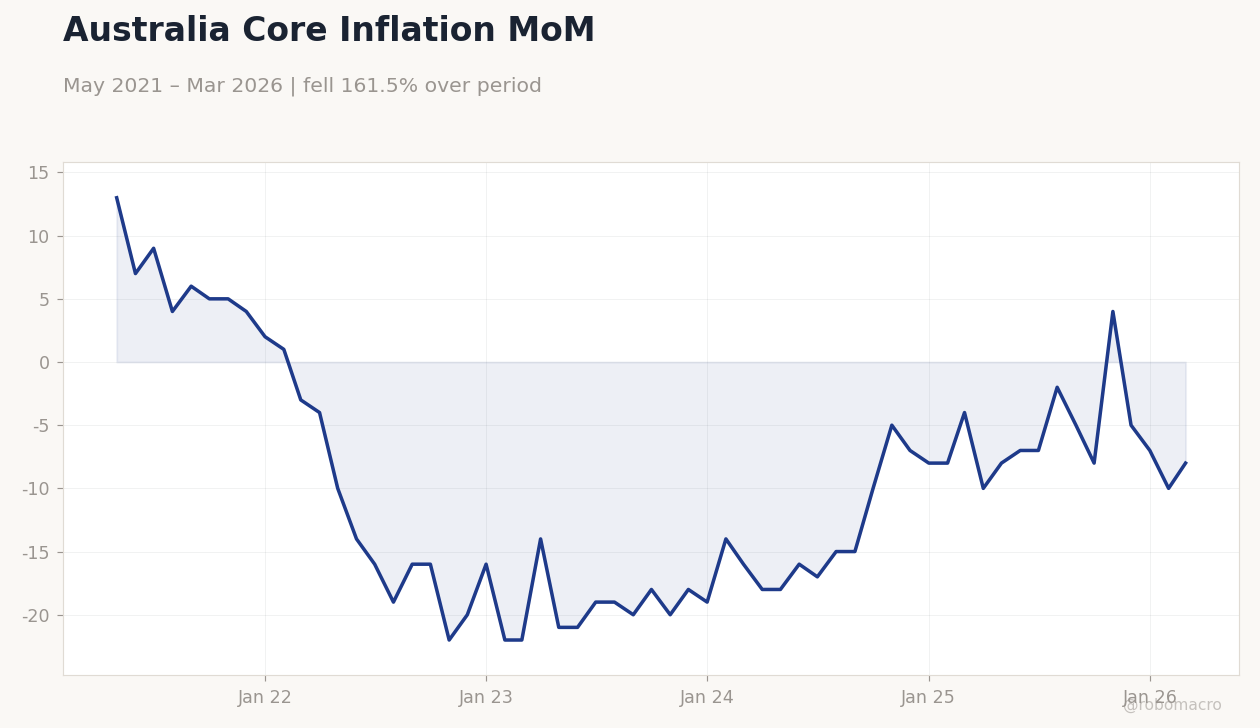

Australia Core Inflation MoM | Type: macro_line | Core CPI % MoM: -8 (2026-03-01) | Range: -22–13 | Trend(6pt): 13,-16,-20,-5,-7,-8

Australia Core Inflation MoM | Type: macro_line | Core CPI % MoM: -8 (2026-03-01) | Range: -22–13 | Trend(6pt): 13,-16,-20,-5,-7,-8

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Inflation Rate Month-over-Month | 0 | - | 21:30 |

| Inflation Rate Year-over-Year | 3.70 | 4.70 | 21:30 |

| Quarterly Inflation Rate Quarter-over-Quarter | 0.60 | 1.40 | 21:30 |

| Quarterly Inflation Rate Year-over-Year | 3.60 | 4.10 | 21:30 |

| Quarterly RBA Trimmed Mean CPI Quarter-over-Quarter | 0.90 | - | 21:30 |

| Quarterly RBA Trimmed Mean CPI Year-over-Year | 3.40 | - | 21:30 |

| RBA Trimmed Mean CPI Month-over-Month | 0.20 | - | 21:30 |

| RBA Trimmed Mean CPI Year-over-Year | 3.30 | - | 21:30 |

| RBNZ Gov Breman Speech | - | - | 21:30 |

| ANZ Business Confidence | 32.50 | - | 21:00 |

- RBA raises rates in split decision amid rising inflation from fuel hikes and oil shocks.

- ASX 200 and NZX 50 edge lower, pressured by energy volatility despite gold's rise.

- AUD and NZD mixed versus USD, with NZD gaining on safe-haven flows.

Yesterday's Recap

Australian equities dipped slightly, with the ASX 200 closing at 8,786.50 after a 0.08% decline, pressured by an oil shock splitting market sentiment ahead of RBA scrutiny. New Zealand's NZX 50 followed suit, ending at 12,874.94 with a 0.08% drop, as dairy-linked stocks faced headwinds from global commodity shifts. The AUD/USD pair rose 0.02% to 0.71, bolstered by gold prices at 4,740.90 amid a 0.76% gain, while Brent crude fell 5.65% to 99.13, heightening Australian inflation concerns.

NZD/USD advanced 0.46% to 0.59 on safe-haven demand, though AUD/NZD declined 0.50% to 1.21, underscoring Kiwi currency strength. BHP shares increased 0.12% to 56.10, supported by mining stability despite equity weakness. Australia's 10-year government yield rose 2.98% to 4.90%, signaling rate hike bets, while New Zealand's short-term rate fell 9.60% to 4.33%, hinting at policy differences.

No major macro data releases occurred in Australia or New Zealand, shifting focus to the RBA's recent split-decision rate hike and its effects on housing and inflation.

The Day Ahead

Focus shifts to Australia's inflation data on April 28, including month-over-month and year-over-year rates, with consensus for year-over-year at 4.7% from 3.7%, potentially shaping RBA policy. Quarterly inflation metrics for Australia are due, with year-over-year consensus at 4.1% versus 3.6%, plus RBA trimmed mean CPI figures that may highlight ongoing price pressures. New Zealand sees a speech by RBNZ Governor Breman on April 28, providing monetary policy clues amid dairy and trade issues.

On April 29, New Zealand's ANZ Business Confidence index releases, following a prior 32.5 reading, possibly indicating sentiment in construction and tourism. Australia's PPI quarter-over-quarter data comes on April 30, with consensus at 1.5% from 0.8%, reflecting producer costs linked to exports like iron ore and LNG.

Other Economic Notes

ANZ economies remain exposed to commodity volatility, with Australia's iron ore and LNG exports vulnerable to China's slowdown, while New Zealand's dairy sector contends with global demand changes. Housing markets are under scrutiny, as high rates strain Australian homeowners, with RBA warnings of tough scenarios raising affordability issues. (cont...)