ANZ Macro Daily(Beta Mode)

AU CPI Misses, Yields Jump

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,710.70 | -0.64% |

| NZX 50 | 12,770.30 | +0.05% |

| AUD/USD | 0.71 | -1.00% |

| NZD/USD | 0.58 | -1.35% |

| AUD/NZD | 1.22 | +0.34% |

| BHP | 54.70 | -1.33% |

| Gold | 4,561.90 | -0.64% |

| Brent Crude | 111.50 | +0.22% |

| Bitcoin | 75,555.02 | -1.04% |

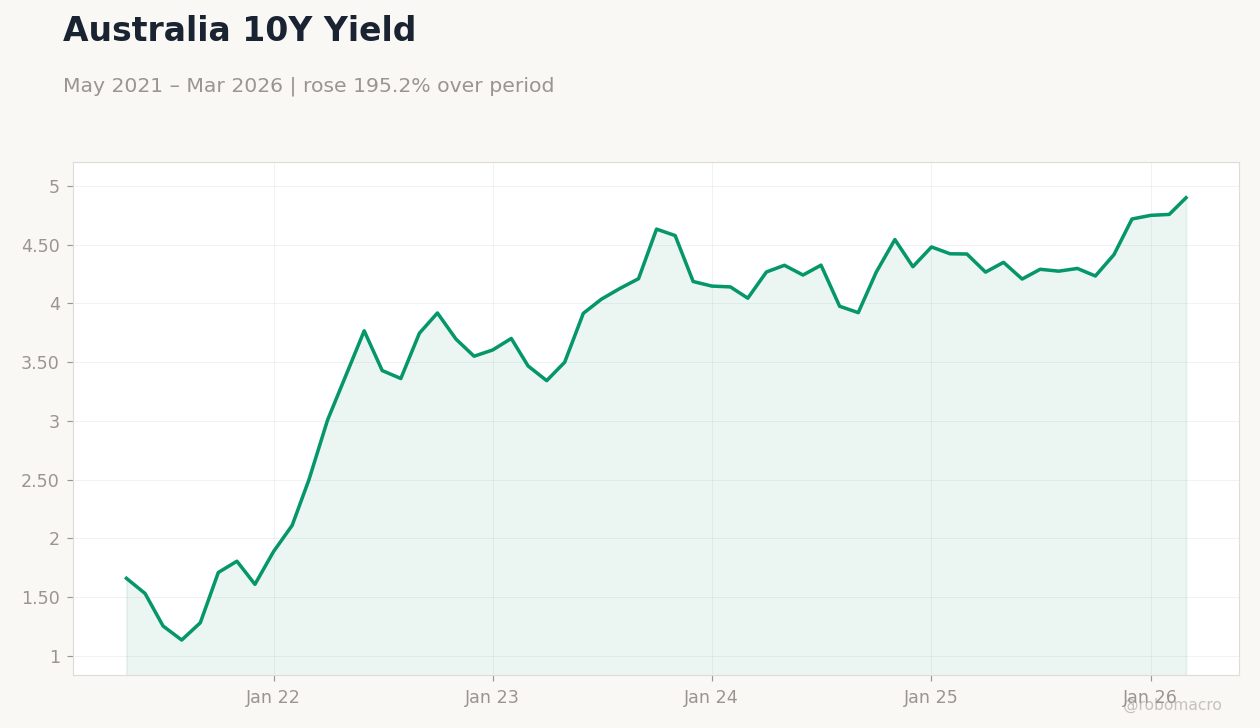

| Australia 10Y Govt Yield | 4.90% | +2.98% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Inflation Rate Month-over-Month | 0 | 1.30 | 1.10 |

| Inflation Rate Year-over-Year | 3.70 | 4.80 | 4.60 |

| RBA Trimmed Mean CPI Month-over-Month | 0.20 | 0.30 | 0.30 |

| RBA Trimmed Mean CPI Year-over-Year | 3.30 | 3.30 | 3.30 |

| RBNZ Gov Breman Speech | - | - | - |

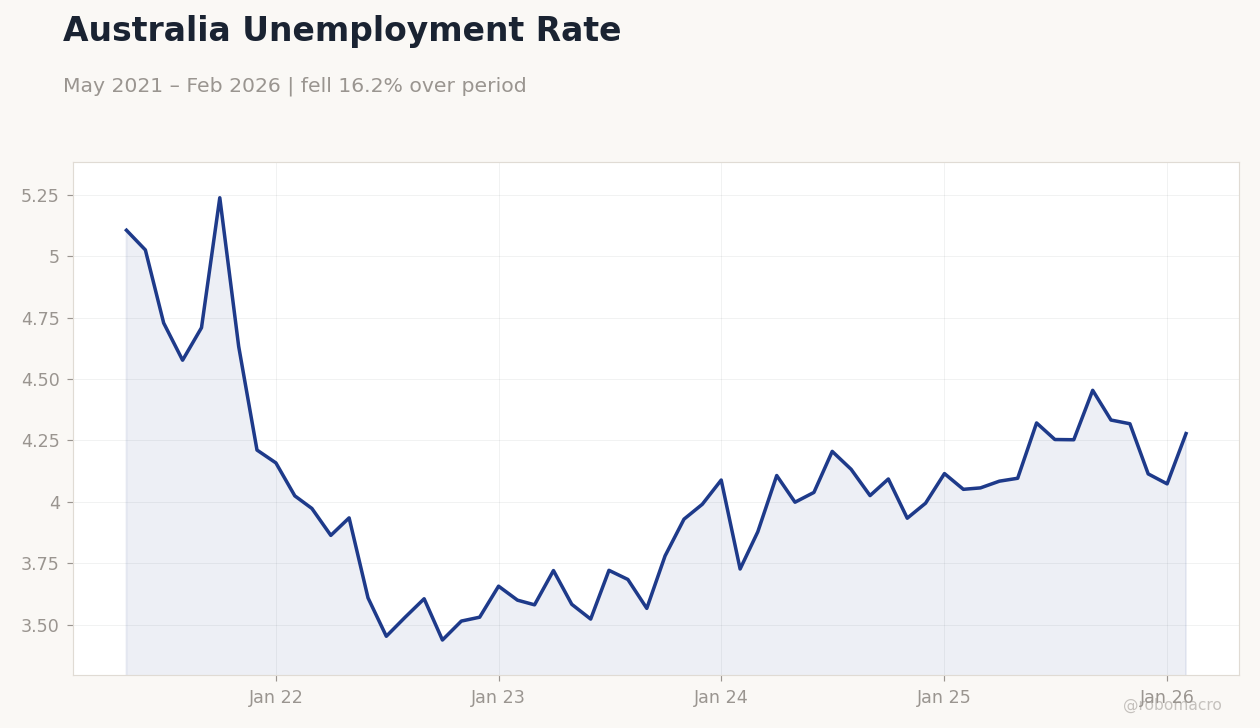

Australia Unemployment Rate | Type: macro_line | AU Unemployment %: 4.278 (2026-02-01) | Range: 3.438–5.238 | Trend(6pt): 5.106,3.453,3.566,3.933,4.073,4.278

Australia Unemployment Rate | Type: macro_line | AU Unemployment %: 4.278 (2026-02-01) | Range: 3.438–5.238 | Trend(6pt): 5.106,3.453,3.566,3.933,4.073,4.278

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| ANZ Business Confidence | 32.50 | - | 17:00 |

| PPI Quarter-over-Quarter | 0.80 | 1.50 | 17:30 |

| Thursday (2026-04-30) | |||

| PPI Quarter-over-Quarter | 0.80 | 1.50 | 17:30 |

- Australian inflation rose less than expected, with headline YoY at 4.6% vs consensus 4.8%, while core measures held steady, pressuring RBA rate hike bets.

- New Zealand's RBNZ Governor Breman speech highlighted stable core inflation within target, signaling no immediate policy shifts.

- Markets reacted with AUD and NZD weakening, ASX 200 down 0.64%, while AU 10Y yields rose 2.98% amid global risk-off.

Yesterday's Recap

Australian inflation data for March showed headline CPI month-over-month at 1.1%, below consensus of 1.3%, and year-over-year at 4.6% against expectations of 4.8%. Core inflation via RBA Trimmed Mean CPI met forecasts, with month-over-month at 0.3% and year-over-year steady at 3.3%, suggesting persistent but contained pressures in Australia. New Zealand had no major data releases, but RBNZ Governor Breman's speech emphasized Q1 core inflation stability within the 1-3% target band, downplaying urgency for rate changes.

Equity markets diverged, with Australia's ASX 200 closing down 0.64% at 8,710.70, dragged by mining stocks like BHP at -1.33% to 54.70 amid commodity weakness, while New Zealand's NZX 50 edged up 0.05% to 12,770.30. Currencies weakened, with AUD/USD falling 1.00% to 0.71 and NZD/USD down 1.35% to 0.58, though AUD/NZD rose 0.34% to 1.22. Bond yields in Australia climbed, with the 10Y government yield up 2.98% to 4.90%, reflecting hawkish inflation reads, while New Zealand's short-term rate dropped 9.60% to 4.33%.

Gold prices dipped 0.64% to 4,561.90, and Brent crude rose modestly 0.22% to 111.50, influencing Australia's export-sensitive sectors.

The Day Ahead

New Zealand's ANZ Business Confidence index is due at 17:00 ET, with the previous reading at 32.5, offering insights into corporate sentiment amid dairy export challenges and China demand risks. Australia's PPI quarter-over-quarter for Q1 releases tomorrow at 17:30 ET, consensus at 1.5% versus prior 0.8%, which could signal upstream inflationary pressures in commodities like iron ore and coal. No major events are scheduled for today in Australia, allowing markets to digest yesterday's CPI miss and its implications for RBA policy.

Attention may shift to global cues, including any Fed signals, potentially impacting AUD and NZD volatility. Overall, these releases could influence rate expectations, with New Zealand's business gauge tying into RBNZ's consumer caution narrative.

Other Economic Notes

Broader themes in ANZ include persistent housing market linkages to monetary policy, with Australia's property sector facing rate sensitivity amid inflation surprises, potentially cooling approvals if hikes resume. (cont...)