Yesterday's Recap

The Reserve Bank of Australia (RBA) hiked its cash rate by 25 basis points to 4.35% in line with consensus, marking the third consecutive increase this year, driven by sticky inflation and external pressures from Middle East conflicts impacting oil prices. During the subsequent RBA press conference, the governor emphasized that Australians are feeling poorer due to inflation and geopolitical tensions, forecasting a rough period ahead while noting government spending limited policy options. Australian equities softened, with the ASX 200 closing down 0.37% at 8,697.10, pressured by mining stocks like BHP which fell 0.87% to 54.47 amid volatile commodity prices.

In New Zealand, the RBNZ published its Financial Stability Report, noting resilience in the banking sector but no automatic tightening bias in response to the Hormuz shock, with board member Gai stating it does not warrant reflexive hikes. New Zealand's NZX 50 bucked the trend, rising 0.09% to 13,035.70, supported by dairy exporters amid stable global demand. Currency movements reflected caution, with AUD/USD dropping 0.38% to 0.72 and NZD/USD falling 0.32% to 0.59, while AUD/NZD eased 0.16% to 1.22.

Commodity shifts included Brent crude tumbling 3.65% to 110.26, weighing on energy-linked assets, though gold rose 1.05% to 4,566.80 as a safe haven.

The Day Ahead

New Zealand's labor market data takes center stage with the Q1 employment change expected at 0.2% quarter-over-quarter and the headline unemployment rate holding steady at 5.4%, both due at 14:45 ET, providing insights into wage pressures and RBNZ's growth outlook. Australia's Ai Group Industry Index, a gauge of manufacturing sentiment, is slated for release at 15:00 ET, with prior reading at -23.6 signaling contraction amid high rates and trade uncertainties. The RBNZ press conference at 17:00 ET will elaborate on the Financial Stability Report, potentially clarifying views on housing market risks and external shocks.

Australia's trade balance for March, forecasted at A$4.25 billion surplus versus previous A$5.686 billion, arrives at 17:30 ET, critical for AUD dynamics given reliance on iron ore and coal exports to China. These releases could amplify currency volatility, especially if NZ employment softens or AU trade disappoints amid global oil disruptions.

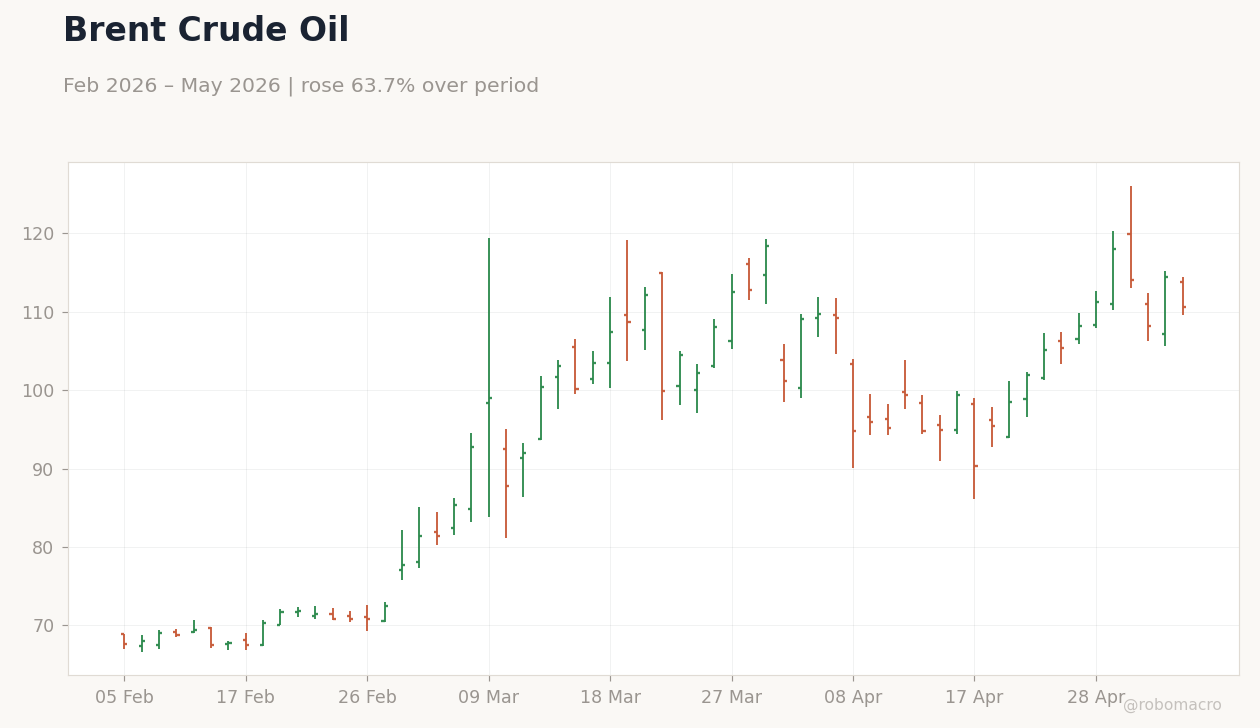

Brent Crude Oil Price | Type: macro_line | Brent Crude Price: 113.9 (2026-04-27) | Range: 59.93–138.2 | Trend(6pt): 68.62,106.1,90.73,77.3,111.9,113.9

Brent Crude Oil Price | Type: macro_line | Brent Crude Price: 113.9 (2026-04-27) | Range: 59.93–138.2 | Trend(6pt): 68.62,106.1,90.73,77.3,111.9,113.9