ANZ Macro Daily(Beta Mode)

AUD Strengthens on Commodity Rally

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,744.40 | -1.51% |

| NZX 50 | 13,210.48 | +0.27% |

| AUD/USD | 0.73 | +0.59% |

| NZD/USD | 0.60 | +0.41% |

| AUD/NZD | 1.22 | +0.16% |

| BHP | 57.95 | -0.97% |

| Gold | 4,740.90 | +0.43% |

| Brent Crude | 104.21 | +2.88% |

| Bitcoin | 82,010.45 | -0.16% |

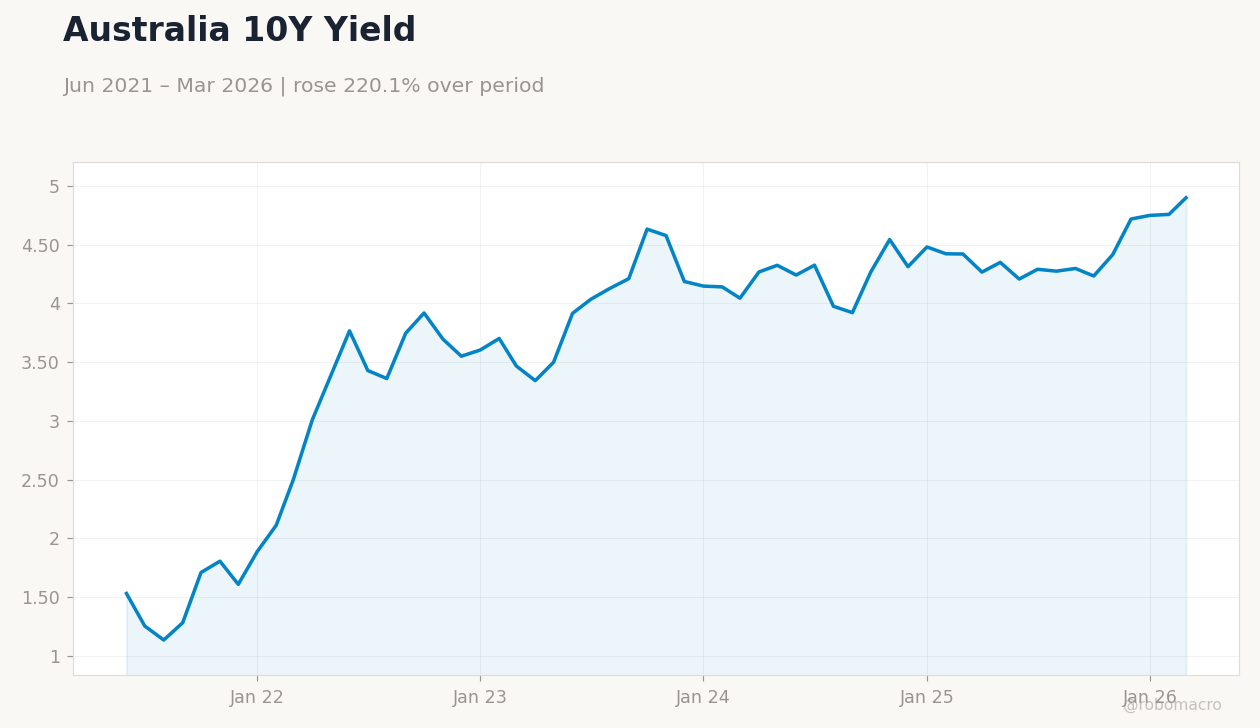

| Australia 10Y Govt Yield | 4.90% | +2.98% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Brent Crude Price | Type: macro_line | Brent Crude Oil Price: 118.3 (2026-05-01) | Range: 59.93–138.2 | Trend(6pt): 69.62,100.3,87.55,77.11,124.2,118.3

Brent Crude Price | Type: macro_line | Brent Crude Oil Price: 118.3 (2026-05-01) | Range: 59.93–138.2 | Trend(6pt): 69.62,100.3,87.55,77.11,124.2,118.3

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Westpac Consumer Confidence Change | -12.50 | - | 20:30 |

| Westpac Consumer Confidence Index | 80.10 | - | 20:30 |

| NAB Business Confidence Index | -29 | - | 21:30 |

| 2026-27 Federal Budget | - | - | 05:30 |

| Home Loans Quarter-over-Quarter | 10.60 | - | 21:30 |

| Investment Lending for Homes | 7.90 | - | 21:30 |

| Business NZ PMI | 53.20 | - | 18:30 |

- Australian equities dipped amid mining weakness, while NZ stocks edged up; AUD and NZD gained on commodity surges despite global tensions.

- RBA grapples with inflation amid household wealth boom; RBNZ eyes tech risks and migration outflows to Australia.

- Iran conflict lifts AUD forecasts to 0.75, boosted by energy prices, as US jobs data signals steady but vulnerable economy.

Yesterday's Recap

Australian equity markets weakened as the ASX 200 closed at 8,744.40, down 1.51% amid broader risk-off sentiment and falling mining stocks like BHP at 57.95, down 0.97%. In contrast, New Zealand's NZX 50 rose to 13,210.48, up 0.27%, supported by defensive sectors. The AUD/USD pair advanced to 0.73, up 0.59%, driven by surging Brent crude at 104.21, up 2.88%, and gold at 4,740.90, up 0.43%, reflecting Australia's commodity export strength.

NZD/USD climbed to 0.60, up 0.41%, though gains were tempered by cross-rate dynamics with AUD/NZD at 1.22, up 0.16%. Australian 10-year government yields rose to 4.90%, up 2.98%, signaling inflation concerns, while New Zealand's short-term rate fell to 4.33%, down 9.60%, indicating easing expectations. No major data releases occurred in either Australia or New Zealand, allowing markets to focus on global commodity trends and ongoing Iran conflict impacts.

Bitcoin held steady at 82,010.45, down 0.16%, with minimal spillover to ANZ crypto-linked assets.

The Day Ahead

Australian markets will watch the Westpac Consumer Confidence Change at 20:30 ET, with previous at -12.5, and the Index at 80.1, both key for gauging household spending amid rate pressures. The NAB Business Confidence Index follows at 21:30 ET, previous -29, offering insights into business sentiment in a high-rate environment. Tomorrow brings Australia's 2026-27 Federal Budget at 05:30 ET, medium-impact, potentially outlining fiscal measures to combat inflation.

Additional releases include Home Loans QoQ at 21:30 ET, previous 10.6, and Investment Lending for Homes at 7.9, both medium-impact and key for housing market trends. New Zealand's Business NZ PMI is slated for May 14 at 18:30 ET, previous 53.2, providing a forward look at manufacturing activity. These events could influence RBA and RBNZ policy outlooks, especially with China's trade data looming as a driver for ANZ commodities.

Other Economic Notes

Australia's residential property prices have risen since recent RBA rate hikes, fueled by household wealth booms that complicate inflation control. New Zealand faces housing market softness, exacerbated by record migration to Australia, with 41,000 Kiwis moving in 2025 for better job prospects. <i>↓ p.2</i>