ANZ Macro Daily(Beta Mode)

RBA Minutes in Focus as AUD Slides

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,630.80 | -0.11% |

| NZX 50 | 12,965.01 | -0.46% |

| AUD/USD | 0.72 | -0.84% |

| NZD/USD | 0.58 | -1.00% |

| AUD/NZD | 1.22 | +0.11% |

| BHP | 60.46 | -2.58% |

| Gold | 4,561.90 | -2.48% |

| Brent Crude | 109.26 | +3.35% |

| Bitcoin | 78,399.13 | +0.34% |

| Australia 10Y Govt Yield | 4.96% | +0.69% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Australia 10-Year Government Yield | Type: macro_line | Yield (%): 4.96 (2026-04-01) | Range: 1.135–4.96 | Trend(6pt): 1.531,3.361,4.633,4.313,4.758,4.96

Australia 10-Year Government Yield | Type: macro_line | Yield (%): 4.96 (2026-04-01) | Range: 1.135–4.96 | Trend(6pt): 1.531,3.361,4.633,4.313,4.758,4.96

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

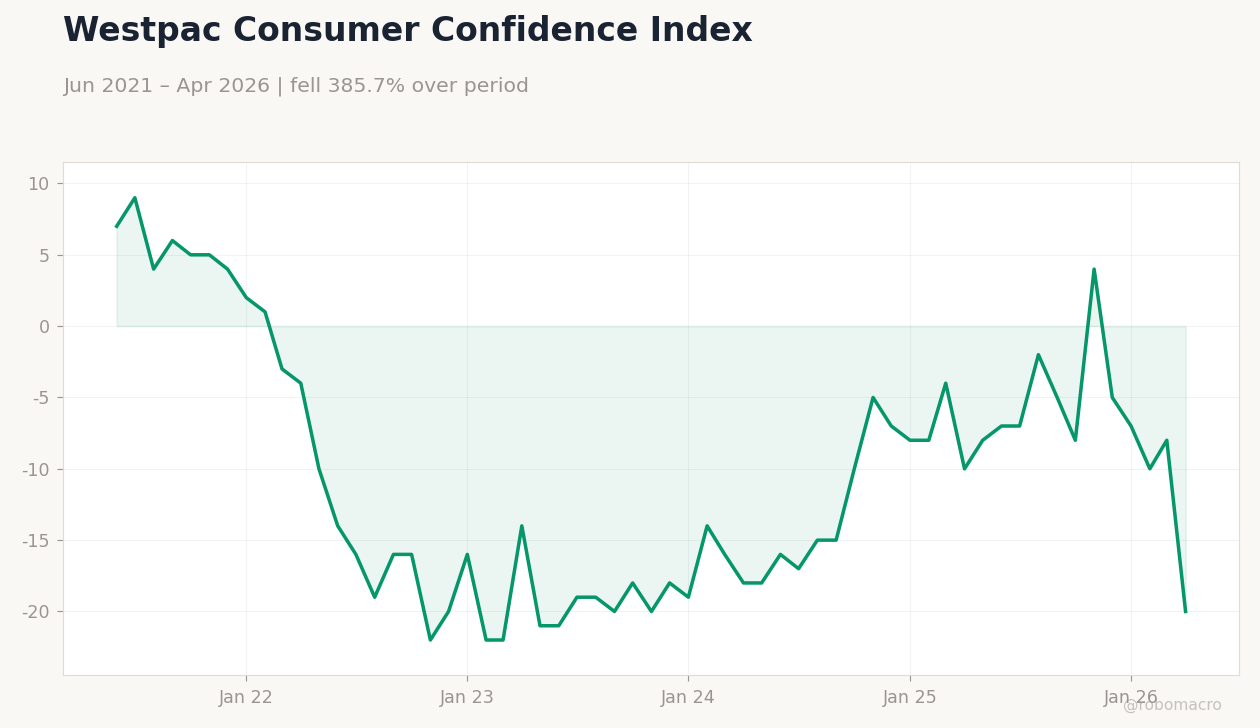

| Westpac Consumer Confidence Change | -12.50 | - | 20:30 |

| RBA Hunter Speech | - | - | 20:30 |

| Westpac Consumer Confidence Index | 80.10 | - | 20:30 |

| RBA Meeting Minutes | - | - | 21:30 |

| Trade Balance | 698m | 842m | 18:45 |

| S&P Global Manufacturing PMI Flash | 51.30 | - | 19:00 |

| S&P Global Services PMI Flash | 50.70 | - | 19:00 |

| Employment Change | 17,900 | 17,500 | 21:30 |

| Full-Time Employment Change | 52,500 | - | 21:30 |

| Headline Unemployment Rate | 4.30 | 4.30 | 21:30 |

- ASX 200 slips 0.11% to 8,630.80 while AUD/USD falls 0.84% to 0.72 amid softer commodity prices.

- RBA minutes and Westpac consumer confidence headline today’s Australian releases.

- Employment change and flash PMIs due later this week with NZ trade balance also scheduled.

Yesterday's Recap

Australian and New Zealand equity markets closed modestly lower with the ASX 200 ending at 8,630.80, down 0.11%, and the NZX 50 falling 0.46% to 12,965.01. The AUD/USD rate declined 0.84% to 0.72 while NZD/USD dropped 1.00% to 0.58, reflecting broad US dollar strength and weaker iron-ore futures. BHP shares fell 2.58% to 60.46, weighing on the broader resources sector.

Australian 10-year government yields rose 0.69% to 4.96% while the NZ short-term rate eased sharply. Brent crude gained 3.35% to 109.26, providing some support to energy-linked names, but gold’s 2.48% decline to 4,561.90 capped safe-haven flows into the AUD. No major economic data were released in either Australia or New Zealand.

The Day Ahead

The RBA releases its May meeting minutes at 21:30 AEST, offering fresh insight into the board’s assessment of inflation and labour-market conditions. Westpac consumer confidence figures for May are also due at 20:30, with both the index and monthly change expected to show ongoing household caution. Later in the week, Australia publishes S&P Global flash manufacturing and services PMIs alongside employment data, including the headline unemployment rate.

New Zealand reports its April trade balance on Wednesday, with the consensus pointing to a narrower deficit. Markets will watch for any signs that softer confidence readings could reinforce expectations for steady RBA policy.

Other Economic Notes

Australia’s heavy reliance on Chinese steel output and iron-ore demand continues to drive AUD swings and mining equity performance. New Zealand’s dairy prices and tourism receipts remain the dominant supports for NZD terms of trade. Housing credit growth in both countries stays resilient, keeping household balance-sheet sensitivity to rate decisions elevated.

Government spending in Australia is drawing closer scrutiny from the RBA for potential inflation spill-overs.

Global Macro News

Global commodity markets remain the key external driver for ANZ currencies, with iron-ore and dairy prices directly influencing trade balances. <i>↓ p.2</i>