ANZ Macro Daily(Beta Mode)

RBA Minutes and Jobs Data in Focus

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,630.80 | -0.11% |

| NZX 50 | 12,762.92 | -1.56% |

| AUD/USD | 0.72 | -0.59% |

| NZD/USD | 0.59 | -0.43% |

| AUD/NZD | 1.22 | -0.18% |

| BHP | 60.46 | -2.58% |

| Gold | 4,565.30 | +0.21% |

| Brent Crude | 108.90 | -0.33% |

| Bitcoin | 76,956.08 | -0.61% |

| Australia 10Y Govt Yield | 4.96% | +0.69% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Australia 10Y Government Yield | Type: macro_line | Yield (%): 4.96 (2026-04-01) | Range: 1.135–4.96 | Trend(6pt): 1.531,3.361,4.633,4.313,4.758,4.96

Australia 10Y Government Yield | Type: macro_line | Yield (%): 4.96 (2026-04-01) | Range: 1.135–4.96 | Trend(6pt): 1.531,3.361,4.633,4.313,4.758,4.96

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| RBA Hunter Speech | - | - | 16:30 |

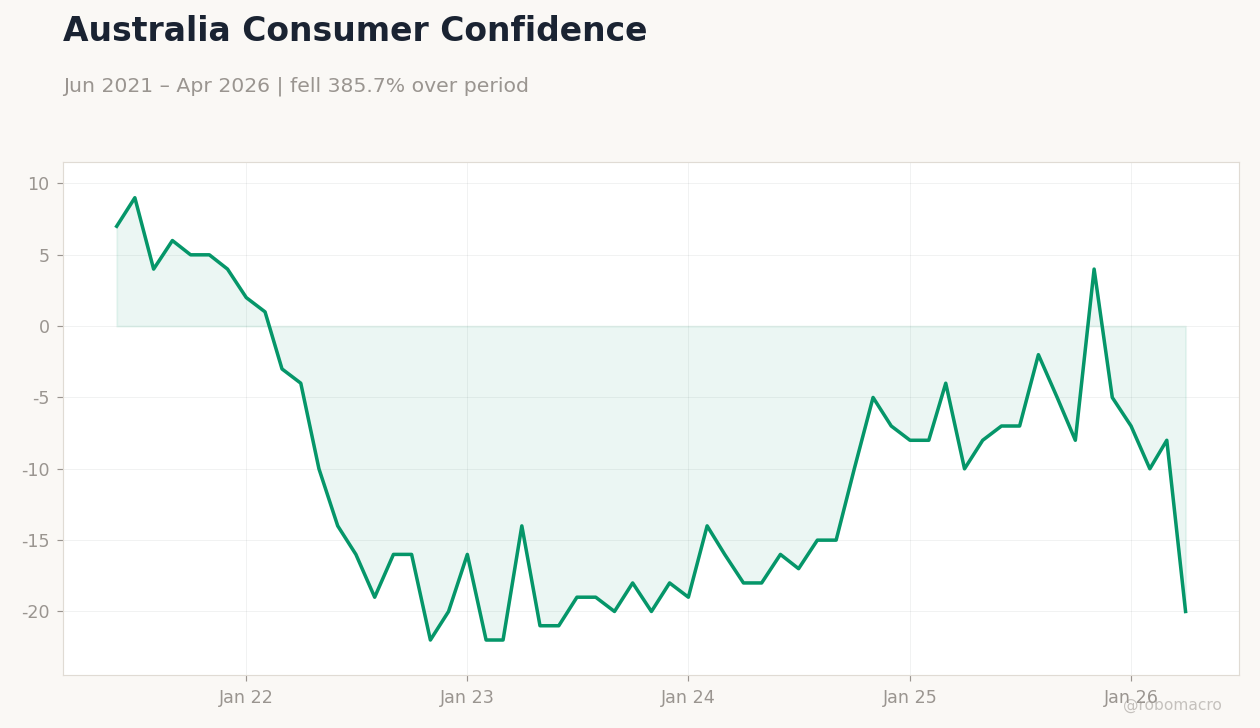

| Westpac Consumer Confidence Change | -12.50 | - | 16:30 |

| Westpac Consumer Confidence Index | 80.10 | - | 16:30 |

| RBA Meeting Minutes | - | - | 17:30 |

| Trade Balance | 698m | 842m | 14:45 |

| S&P Global Manufacturing PMI Flash | 51.30 | - | 15:00 |

| S&P Global Services PMI Flash | 50.70 | - | 15:00 |

| Employment Change | 17,900 | 20,000 | 17:30 |

| Full-Time Employment Change | 52,500 | - | 17:30 |

| Headline Unemployment Rate | 4.30 | 4.30 | 17:30 |

- ASX 200 slips 0.11% while NZX 50 drops 1.56% amid softer commodity sentiment and higher yields.

- AUD/USD falls to 0.72 as Westpac confidence data and RBA minutes loom for Australia.

- RBA cash rate holds at 4.10% with markets watching Hunter speech and upcoming employment figures.

Yesterday's Recap

Markets closed mixed on 17 May with the ASX 200 easing 0.11% to 8,630.80 as BHP fell 2.58% to 60.46 despite firmer iron-ore futures. The NZX 50 declined 1.56% to 12,762.92, pressured by broader risk-off flows. AUD/USD traded down 0.59% at 0.72 while NZD/USD slipped 0.43% to 0.59, leaving AUD/NZD 0.18% lower at 1.22.

Australian 10-year yields rose 0.69% to 4.96% and NZ short-term rates fell sharply to 4.33%. Gold edged 0.21% higher to 4,565.30 while Brent crude eased 0.33% to 108.90. No major data releases occurred in either Australia or New Zealand.

The Day Ahead

Australia releases Westpac Consumer Confidence Index and Change at 16:30 AEST alongside RBA Hunter speech. RBA Meeting Minutes follow at 17:30 AEST, offering fresh insight into the board’s 4.10% policy stance. New Zealand Trade Balance prints on 20 May at 14:45 NZT with a consensus surplus of NZ$842 million.

S&P Global flash PMIs for Australia appear the same day, followed by Employment Change and Unemployment Rate data at 17:30 AEST. Markets will monitor any signals on wage pressures and labour-market resilience.

Other Economic Notes

Australia’s commodity-export model remains tightly linked to China demand, with BHP serving as the key bellwether for mining sentiment. New Zealand’s dairy and tourism sectors continue to underpin NZD stability despite softer construction activity. Housing markets in both countries stay sensitive to rate expectations, with any RBA or RBNZ hawkish tilt likely to weigh on prices.

Fiscal budgets have improved medium-term outlooks yet left inflation control squarely with the central banks.

Global Macro News

Hawkish Fed bets continue to lift the US dollar and pressure the yen, supporting AUD/JPY cross rates. China data misses have weighed on regional sentiment but left commodity prices resilient for Australian exporters. Saudi tokenisation initiatives and broader Middle-East flows show limited direct spill-over to ANZ markets.

<i>↓ p.2</i>