ANZ Macro Daily(Beta Mode)

RBA Minutes Flag Inflation and Growth Risks

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,505.30 | -1.45% |

| NZX 50 | 12,974.32 | +1.66% |

| AUD/USD | 0.71 | -0.27% |

| NZD/USD | 0.58 | +0.09% |

| AUD/NZD | 1.22 | -0.37% |

| BHP | 58.13 | -1.09% |

| Gold | 4,489.00 | -1.39% |

| Brent Crude | 111.34 | -0.68% |

| Bitcoin | 76,789.63 | -0.21% |

| Australia 10Y Govt Yield | 4.96% | +0.69% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

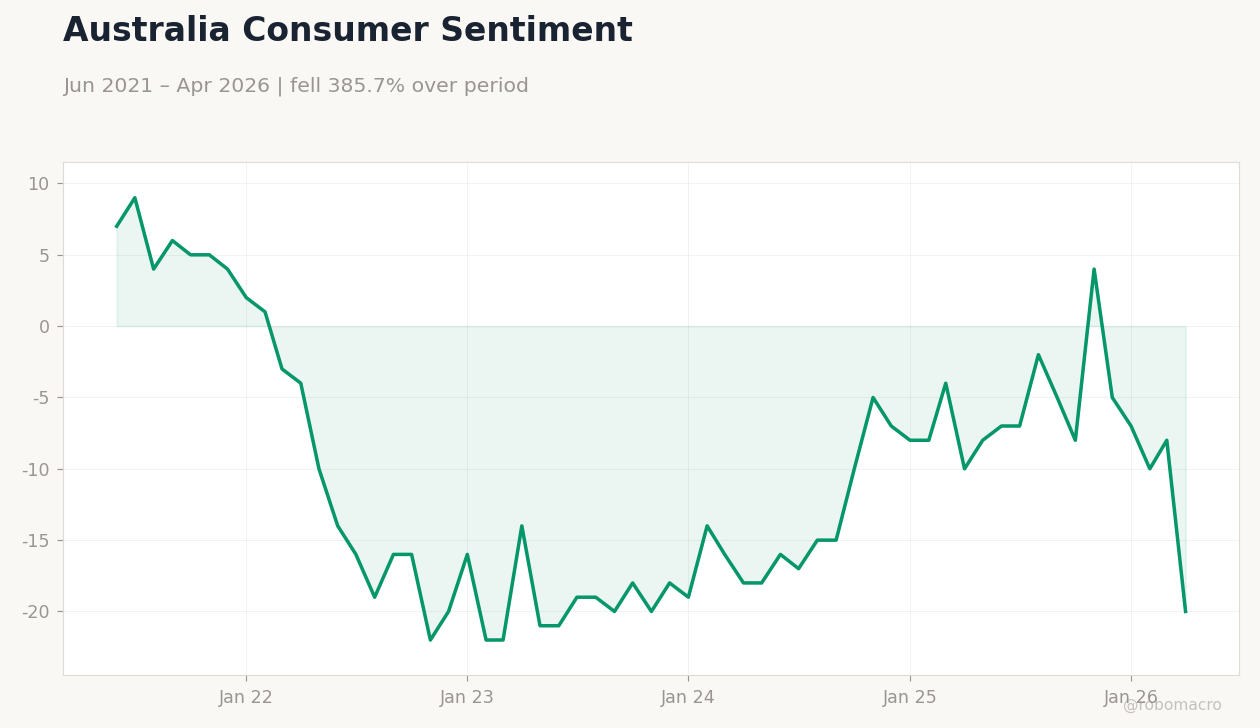

| Westpac Consumer Confidence Change | -12.50 | - | 3.50 |

| RBA Hunter Speech | - | - | - |

| Westpac Consumer Confidence Index | 80.10 | - | 83 |

| RBA Meeting Minutes | - | - | - |

Australia 10Y Govt Yield | Type: macro_line | Yield (%): 4.96 (2026-04-01) | Range: 1.135–4.96 | Trend(6pt): 1.531,3.361,4.633,4.313,4.758,4.96

Australia 10Y Govt Yield | Type: macro_line | Yield (%): 4.96 (2026-04-01) | Range: 1.135–4.96 | Trend(6pt): 1.531,3.361,4.633,4.313,4.758,4.96

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Trade Balance | 698m | 980m | 18:45 |

| S&P Global Manufacturing PMI Flash | 51.30 | - | 19:00 |

| S&P Global Services PMI Flash | 50.70 | - | 19:00 |

| Employment Change | 17,900 | 17,500 | 21:30 |

| Full-Time Employment Change | 52,500 | - | 21:30 |

| Headline Unemployment Rate | 4.30 | 4.30 | 21:30 |

- Australian consumer confidence rebounds sharply while RBA minutes highlight inflation pressures

- ASX 200 falls 1.45% as NZX 50 gains 1.66% on defensive buying

- RBA holds cash rate at 4.10% with markets pricing later easing

Yesterday's Recap

Australian Westpac Consumer Confidence Change printed +3.5 in May, rebounding from -12.5, while the Index rose to 83 from 80.1. The RBA released its Meeting Minutes and Governor Hunter spoke, both underscoring persistent price pressures and downside risks to growth. Australia’s equity benchmark ASX 200 closed at 8,505.30, down 1.45%, led by mining names, while the NZX 50 advanced 1.66% to 12,974.32.

AUD/USD eased 0.27% to 0.71 and NZD/USD rose 0.09% to 0.58, narrowing AUD/NZD by 0.37%. Australian 10-year yields climbed 0.69% to 4.96% and NZ short-term rates fell 9.60% to 4.33%. BHP declined 1.09% to 58.13 amid softer iron-ore sentiment.

The RBA cash rate remains at 4.10%.

The Day Ahead

New Zealand releases its Trade Balance at 18:45 NZ time with consensus pointing to a NZ$980 million surplus. Australia follows with S&P Global Manufacturing and Services PMI Flash prints at 19:00, expected to show modest expansion. Employment Change, Full-Time Employment Change and the Headline Unemployment Rate are due at 21:30, with the jobless rate forecast to hold at 4.3%.

Markets will also monitor any follow-up comments from RBA officials on the just-released minutes.

Other Economic Notes

Australia’s inflation warnings have intensified, with the RBA citing risks of a 1990s-style recession if oil shocks persist. China demand remains the dominant external driver for Australian commodity exports and fiscal balances. New Zealand’s PPI Input jump of 1.4% has lifted NZD outlook and reduced near-term rate-cut expectations.

Housing-market linkages continue to influence both central banks’ policy deliberations given elevated household debt levels.

Global Macro News

Japan’s surprise Q1 GDP growth weakened the yen and supported USD/JPY, indirectly pressuring AUD and NZD crosses. China’s slowdown is exerting dual pressure on the Australian dollar via softer commodity demand, according to MUFG. Samsung strike risks could trim South Korea’s economy by 0.5 percentage points, with spillovers to regional supply chains that touch Australian LNG and NZ dairy exports.

<i>↓ p.2</i>