ANZ Macro Daily(Beta Mode)

RBA Hike Bets Unwind After Jobs Data

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,657.00 | +0.41% |

| NZX 50 | 12,991.31 | +0.88% |

| AUD/USD | 0.72 | +0.27% |

| NZD/USD | 0.59 | -0.06% |

| AUD/NZD | 1.22 | +0.28% |

| BHP | 59.75 | +1.10% |

| Gold | 4,523.20 | -0.37% |

| Brent Crude | 100.21 | -2.31% |

| Bitcoin | 76,610.09 | -0.08% |

| Australia 10Y Govt Yield | 4.96% | +0.69% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Australia 10Y Government Yield | Type: macro_line | Yield (%): 4.96 (2026-04-01) | Range: 1.135–4.96 | Trend(6pt): 1.531,3.361,4.633,4.313,4.758,4.96

Australia 10Y Government Yield | Type: macro_line | Yield (%): 4.96 (2026-04-01) | Range: 1.135–4.96 | Trend(6pt): 1.531,3.361,4.633,4.313,4.758,4.96

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Construction Work Done Quarter-over-Quarter | -0.10 | 0.80 | 21:30 |

| Inflation Rate Month-over-Month | 1.10 | 0.60 | 21:30 |

| Inflation Rate Year-over-Year | 4.60 | 4.40 | 21:30 |

| RBA Trimmed Mean CPI Month-over-Month | 0.30 | 0.40 | 21:30 |

| RBA Trimmed Mean CPI Year-over-Year | 3.30 | - | 21:30 |

| RBNZ Interest Rate Decision | 2.25 | 2.25 | 22:00 |

| RBNZ Press Conference | - | - | 23:00 |

| RBA Bulletin | - | - | 21:30 |

| Budget 2026 | - | - | 22:00 |

| ANZ Business Confidence | -10.60 | - | 21:00 |

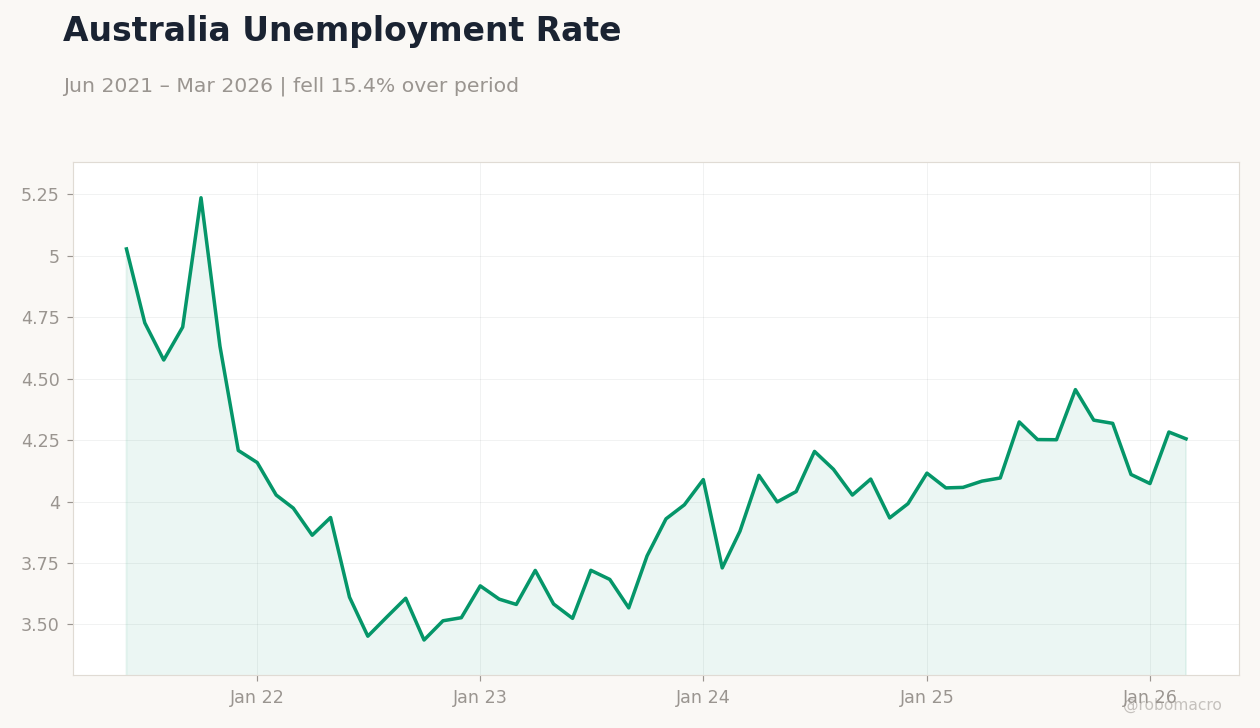

- Weak Australian jobs data reduced odds of an RBA rate hike in June.

- RBNZ expected to hold OCR at 2.25% on 26 May as economy cools.

- ASX 200 gained 0.41% to 8,657 with AUD/USD at 0.72 supported by commodities.

Yesterday's Recap

Australian employment data released on 23 May showed a sharp rise in the unemployment rate, the highest level in over four years, which immediately reduced market pricing for an RBA rate hike in June. The ASX 200 advanced 0.41% to 8,657 led by BHP which gained 1.10% to 59.75 on firmer iron-ore prices. The NZX 50 climbed 0.88% to 12,991.31 despite softer dairy sentiment.

AUD/USD lifted 0.27% to 0.72 while NZD/USD eased 0.06% to 0.59. Australian 10-year yields rose 0.69% to 4.96% as markets adjusted rate expectations. NZ short-term rates fell 9.60% to 4.33% reflecting lower RBNZ tightening odds.

The RBA cash rate remains at 4.10%.

The Day Ahead

Markets focus on the RBNZ cash-rate decision on 26 May where the committee is expected to hold the OCR at 2.25%. Australian quarterly inflation data and construction work done are also due that evening, with trimmed-mean CPI forecast at 0.4% m/m. The RBNZ press conference follows at 23:00 ET.

On 27 May the RBA releases its monthly bulletin while New Zealand presents Budget 2026. ANZ Business Confidence for May prints on 28 May.

Other Economic Notes

Australia’s commodity-export model remains tightly linked to Chinese steel output which continues to underpin iron-ore and thermal-coal prices. New Zealand’s housing market shows modest price gains but retail sales weakness signals softer domestic demand. Both economies face divergent inflation trajectories with Australian trimmed-mean CPI still above target while New Zealand price pressures ease faster.

Global Macro News

Hawkish RBA expectations have unwound rapidly after the jobs print, prompting Rabobank to warn of further AUD repricing pressure against the yen. South Korean authorities issued verbal intervention as the won approached 1,520 per dollar, highlighting regional FX volatility. Hedge funds have scaled back steep RBNZ rate-rise bets as New Zealand economic data cool.

Brent crude fell 2.31% to 100.21 amid softer global demand signals. Gold eased 0.37% to 4,523.20 yet remains supportive for Australian export revenues. China’s industrial-profit trends will be watched closely for spill-overs into AUD and fiscal receipts.