ANZ Macro Daily(Beta Mode)

Hawkish RBNZ Lifts NZD as AUD Weakens

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,731.70 | +1.62% |

| NZX 50 | 13,244.55 | +0.29% |

| AUD/USD | 0.72 | +0.00% |

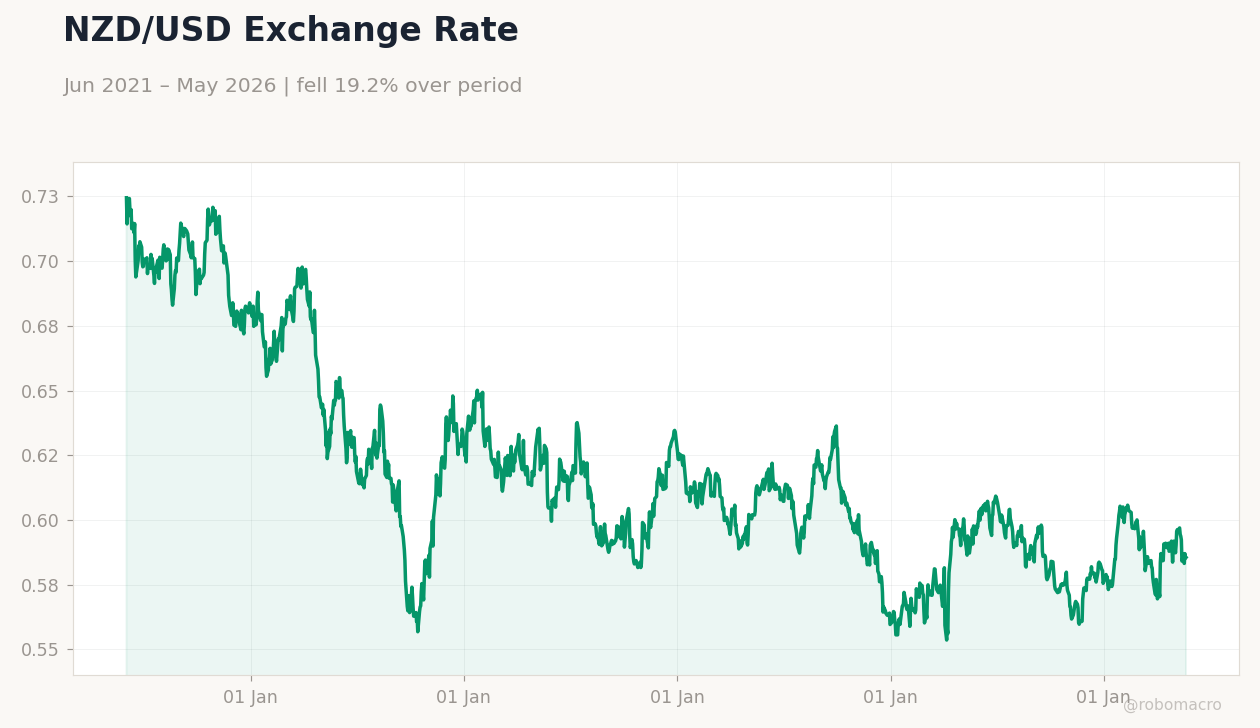

| NZD/USD | 0.59 | -0.14% |

| AUD/NZD | 1.21 | +0.12% |

| BHP | 62.31 | +2.91% |

| Gold | 4,512.50 | -1.05% |

| Brent Crude | 95.32 | +3.55% |

| Bitcoin | 71,457.13 | -2.88% |

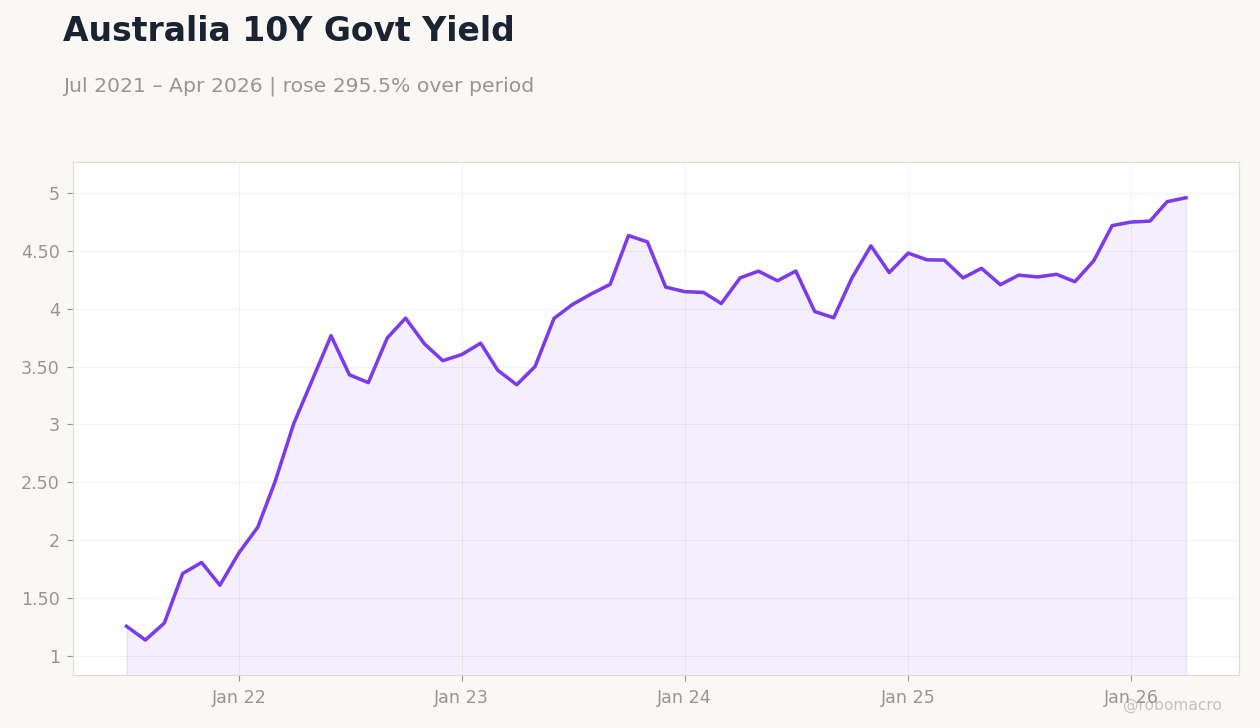

| Australia 10Y Govt Yield | 4.96% | +0.69% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

AUD/USD Exchange Rate | Type: macro_line | AUD per USD: 0.7132 (2026-05-22) | Range: 0.598–0.7765 | Trend(5pt): 0.7752,0.6909,0.6666,0.6323,0.7132

AUD/USD Exchange Rate | Type: macro_line | AUD per USD: 0.7132 (2026-05-22) | Range: 0.598–0.7765 | Trend(5pt): 0.7752,0.6909,0.6666,0.6323,0.7132

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Building Permits Month-over-Month Prel | -10.50 | -1.50 | 21:30 |

| Company Gross Profits Quarter-over-Quarter | 5.80 | - | 21:30 |

| Ai Group Industry Index | -24.40 | - | 19:00 |

| GDP Growth Quarter-over-Quarter | 0.80 | 0.50 | 21:30 |

| GDP Growth Year-over-Year | 2.60 | 2.70 | 21:30 |

| Trade Balance | -1,841m | -1,610m | 21:30 |

| RBA Gov Bullock Speech | - | - | 01:00 |

| RBA Kent Speech | - | - | 01:00 |

| RBA Hauser Speech | - | - | 00:30 |

- RBNZ signals earlier and steeper rate hikes, pushing NZD higher against AUD.

- ASX 200 rises 1.62% while Australia 10-year yields climb to 4.96%.

- RBA cash rate remains at 4.10% with markets pricing lower hike odds.

Yesterday's Recap

Markets focused on diverging central bank signals across ANZ. The NZ short-term rate reached 4.33% amid RBNZ comments on faster tightening. ASX 200 advanced 1.62% to 8,731.70, led by BHP which gained 2.91%.

AUD/USD held steady at 0.72 while NZD/USD eased 0.14% to 0.59. AUD/NZD rose 0.12% to 1.21 as hawkish RBNZ rhetoric supported the kiwi. Australia 10-year government yields increased 0.69% to 4.96%.

Brent crude climbed 3.55% to 95.32 while gold declined 1.05%. Bitcoin fell 2.88% to 71,457.13. NZX 50 gained 0.29% to 13,244.55.

News flow highlighted RBNZ divergence from the RBA, with Australian data showing cooling momentum via rising unemployment and softer inflation. NAB flagged further rate hikes despite RBA forecasts.

The Day Ahead

Australia releases Building Permits MoM Prel and Company Gross Profits QoQ at 21:30 ET. Ai Group Industry Index follows on 2 June. GDP growth QoQ and YoY prints are due the same day, with consensus at 0.5% and 2.7%.

Trade balance data arrives on 3 June. RBA Governor Bullock and Deputy Governor Kent speak on 4 June, followed by RBA Hauser on 5 June. Markets will watch for any fresh RBA guidance on the 4.10% cash rate.

Other Economic Notes

Australian data continue to show cooling momentum with rising unemployment and softer inflation. NAB has defied RBA forecasts by flagging further rate hikes. Commodity linkages remain critical as iron ore and LNG exports face China demand uncertainty.

Housing markets in both countries stay sensitive to rate paths. BHP performance continues to signal mining sector sentiment. Manufacturing PMI beat forecasts, tempering some RBA rate-cut bets.

Global Macro News

Global investors await further central bank signals amid Middle East developments. US dollar edges higher on policy uncertainty. China’s manufacturing indicators influence Australian commodity outlook.

Brent crude strength supports energy exporters while gold weakness reflects shifting safe-haven flows. AUD faces pressure from lower RBA hike probabilities. NZD benefits from RBNZ divergence versus regional peers.

<i>↓ p.2</i>