ANZ Macro Daily(Beta Mode)

RBA Holds as Inflation Concerns Linger

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,729.40 | -0.03% |

| NZX 50 | 13,170.71 | -0.56% |

| AUD/USD | 0.72 | +0.05% |

| NZD/USD | 0.59 | -0.90% |

| AUD/NZD | 1.21 | +0.94% |

| BHP | 63.37 | +1.42% |

| Gold | 4,516.60 | +0.93% |

| Brent Crude | 96.00 | +1.07% |

| Bitcoin | 67,089.62 | -5.93% |

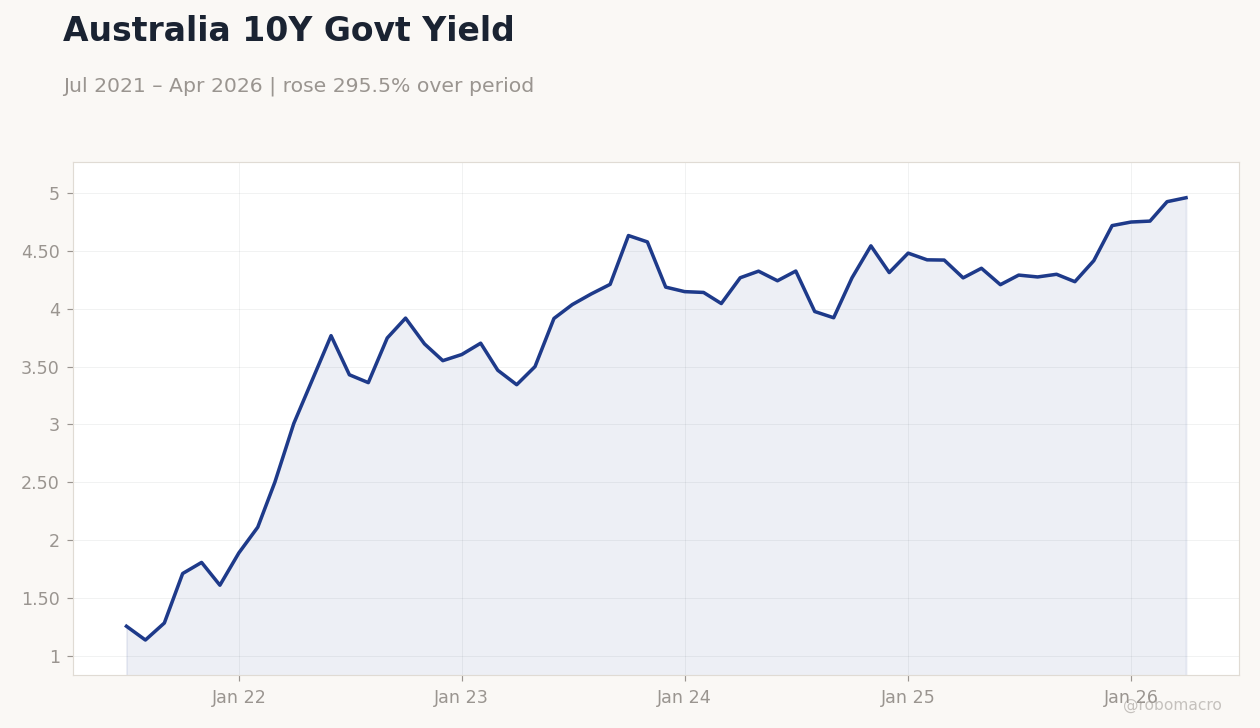

| Australia 10Y Govt Yield | 4.96% | +0.69% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Building Permits Month-over-Month Prel | -10.50 | -1.50 | -3.40 |

| Company Gross Profits Quarter-over-Quarter | 5.90 | - | -1.30 |

Australia 10Y Govt Yield | Type: macro_line | Yield %: 4.96 (2026-04-01) | Range: 1.135–4.96 | Trend(6pt): 1.254,3.747,4.578,4.481,4.926,4.96

Australia 10Y Govt Yield | Type: macro_line | Yield %: 4.96 (2026-04-01) | Range: 1.135–4.96 | Trend(6pt): 1.254,3.747,4.578,4.481,4.926,4.96

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Ai Group Industry Index | -24.40 | - | 19:00 |

| GDP Growth Quarter-over-Quarter | 0.80 | 0.50 | 21:30 |

| GDP Growth Year-over-Year | 2.60 | 2.70 | 21:30 |

| Trade Balance | -1,841m | -1,610m | 21:30 |

| RBA Gov Bullock Speech | - | - | 01:00 |

| RBA Kent Speech | - | - | 01:00 |

| RBA Hauser Speech | - | - | 00:30 |

| Westpac Consumer Confidence Change | 3.50 | - | 20:30 |

| Westpac Consumer Confidence Index | 83 | - | 20:30 |

| NAB Business Confidence Index | -24 | - | 21:30 |

- Australian building permits fell 3.4% MoM in April, less than consensus, while company gross profits dropped 1.3% QoQ.

- ASX 200 edged down 0.03% to 8,729.40; AUD/USD rose 0.05% to 0.72 amid firmer commodity prices.

- RBA signals persistent inflation risks, tempering near-term rate-cut expectations for both RBA and RBNZ.

Yesterday's Recap

Australian data showed building permits declining 3.4% month-over-month in April, beating the -1.5% consensus but remaining weak after March’s -10.5% drop. Company gross operating profits contracted 1.3% quarter-over-quarter, reversing the prior 5.9% gain and highlighting margin pressure in the resources sector. Markets reflected caution, with the ASX 200 closing at 8,729.40, down 0.03%, while the NZX 50 fell 0.56% to 13,170.71.

The Australian dollar firmed to 0.72 against the USD, supported by gold rising 0.93% to 4,516.60 and Brent crude up 1.07% at 96.00. Australian 10-year yields climbed 0.69% to 4.96%, and the NZ short-term rate eased sharply. News flow centred on RBA warnings that inflation persistence could delay easing, alongside concerns that recent pay rises risk stoking price pressures.

The Day Ahead

Australia releases GDP growth figures today, with quarter-over-quarter expected at 0.5% after 0.8% previously and year-over-year at 2.7%. The Ai Group Industry Index will also print at 19:00 AEST. RBA Governor Bullock and Deputy Governor Kent are scheduled to speak on 4 June, followed by Assistant Governor Hauser on 5 June.

Markets will watch for any fresh signals on the timing of rate cuts. New Zealand data remain light, though dairy auction results and inflation expectations near 5% continue to influence RBNZ positioning.

Other Economic Notes

Australia’s commodity export strength, led by iron ore and gold, continues to underpin the AUD despite softer domestic profit growth. Housing market weakness persists, with RBA and Treasury officials citing higher interest rates and tax settings as key drags on prices. New Zealand faces similar housing pressures alongside elevated inflation expectations that threaten the RBNZ’s easing path.

Broader China demand signals remain the dominant external driver for both economies through trade and royalty revenues.

Global Macro News

Global markets showed mixed risk sentiment, with Bitcoin falling 5.93% while gold and oil advanced on safe-haven flows. The US dollar edged higher ahead of central bank signals and Middle East developments. <i>↓ p.2</i>