ANZ Macro Daily(Beta Mode)

Soft Australian GDP Weighs on AUD as RBA Holds

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,785.70 | +0.70% |

| NZX 50 | 13,101.61 | -0.10% |

| AUD/USD | 0.71 | -0.51% |

| NZD/USD | 0.59 | -0.88% |

| AUD/NZD | 1.22 | +0.36% |

| BHP | 62.80 | -3.25% |

| Gold | 4,505.20 | +1.54% |

| Brent Crude | 95.25 | -2.62% |

| Bitcoin | 63,441.74 | -0.89% |

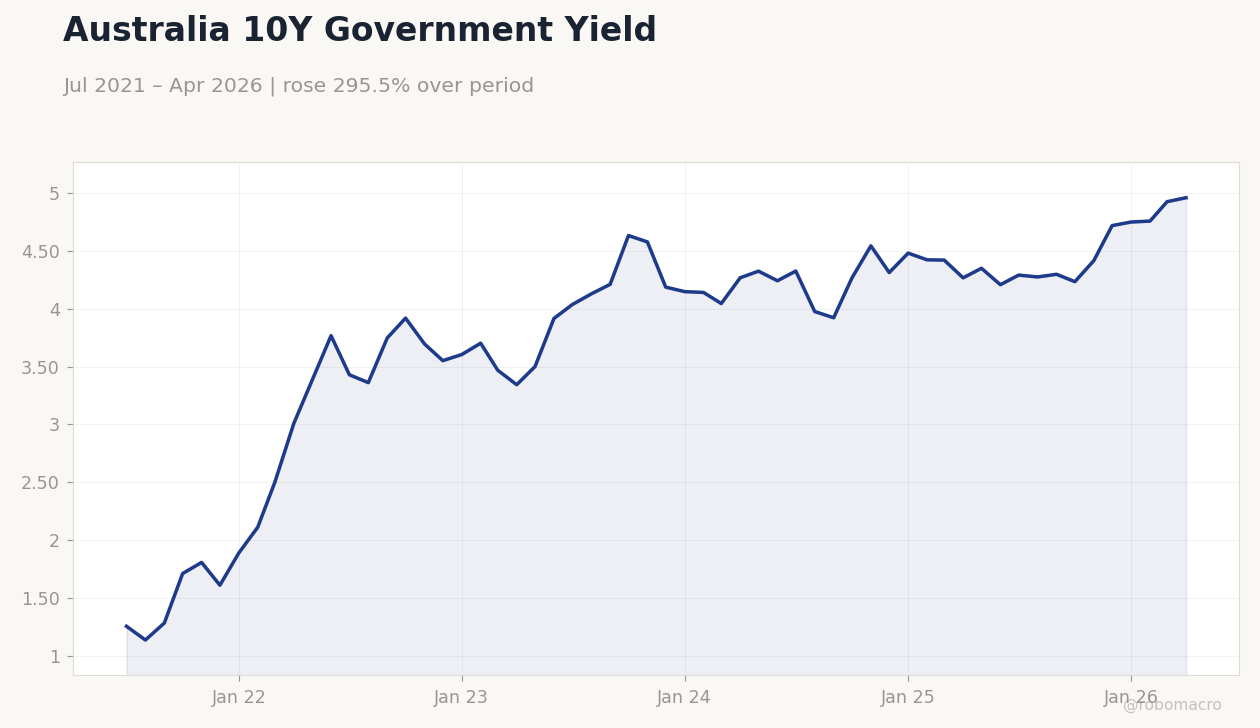

| Australia 10Y Govt Yield | 4.96% | +0.69% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| RBA Harper Speech | - | - | - |

| Building Permits Month-over-Month Prel | -10.50 | -1.50 | -3.40 |

| Company Gross Profits Quarter-over-Quarter | 5.90 | - | -1.30 |

| Ai Group Industry Index | -24.40 | - | -26.50 |

| GDP Growth Quarter-over-Quarter | 0.90 | 0.50 | 0.30 |

| GDP Growth Year-over-Year | 2.60 | 2.70 | 2.50 |

| Trade Balance | -1,024m | 1,800m | 1,791m |

| RBA Gov Bullock Speech | - | - | - |

| RBA Kent Speech | - | - | - |

Australia 10Y Government Yield | Type: macro_line | Yield (%): 4.96 (2026-04-01) | Range: 1.135–4.96 | Trend(6pt): 1.254,3.747,4.578,4.481,4.926,4.96

Australia 10Y Government Yield | Type: macro_line | Yield (%): 4.96 (2026-04-01) | Range: 1.135–4.96 | Trend(6pt): 1.254,3.747,4.578,4.481,4.926,4.96

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| RBA Hauser Speech | - | - | 20:30 |

| Friday (2026-06-05) | |||

| RBA Hauser Speech | - | - | 20:30 |

- Australian Q1 GDP slowed to 0.3% q/q and 2.5% y/y, below consensus, pressuring AUD/USD to 0.71.

- ASX 200 rose 0.7% while NZX 50 fell 0.1%; trade balance beat at A$1.791bn surplus.

- RBA holds cash rate at 4.10%; Bullock notes housing cooling and rules out recession risks.

Yesterday's Recap

Australian Q1 GDP printed 0.3% q/q versus 0.5% consensus and 2.5% y/y versus 2.7% expected, confirming the slowdown after prior 0.9% q/q. Building permits fell 3.4% m/m and company gross profits dropped 1.3% q/q, while the Ai Group index weakened to -26.5. The trade balance swung to a A$1.791bn surplus, matching the A$1.8bn consensus.

ASX 200 gained 0.70% to 8,785.70 on commodity support, but NZX 50 slipped 0.10% to 13,101.61. AUD/USD fell 0.51% to 0.71 and NZD/USD dropped 0.88% to 0.59 amid Gulf tensions. RBA Governor Bullock and Deputy Governor Kent both spoke, stressing no stagflation concerns and early signs of rate hikes cooling the housing market.

The Day Ahead

RBA Assistant Governor Hauser is scheduled to speak at 20:30 ET, likely reiterating the 4.10% cash rate stance. No major Australian data releases are due tomorrow. Markets will watch for any fresh signals on inflation persistence after the soft GDP print.

NZ data calendar remains quiet, leaving focus on RBNZ commentary and AUD/NZD cross at 1.22. Traders await US non-farm payrolls for direction on global yields.

Other Economic Notes

Weak Australian GDP reinforces China demand concerns, with iron ore and LNG exports facing downside risks. BHP shares fell 3.25% despite gold rising 1.54% to 4,505.20. Housing market linkages remain critical, as higher rates continue to weigh on both Australian and New Zealand buyer demand.

Commodity price volatility from Middle East tensions adds uncertainty to the AUD trade balance outlook.

Global Macro News

Gulf tensions lifted safe-haven flows into gold and the US dollar, pressuring both AUD and NZD lower. Hawkish Fed remarks boosted USD strength, contributing to NZD/USD weakness. Australian recession fears eased after RBA Governor Bullock stated the economy can weather oil shocks.

Global bodies continue to comment on RBA rate paths amid the slowdown. Yen weakness past 160 per dollar highlighted carry-trade support for AUD/JPY above 114.50. <i>↓ p.2</i>