ANZ Macro Daily(Beta Mode)

AUD Weakens as GDP Growth Slows Sharply

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,625.10 | -0.70% |

| NZX 50 | 13,161.97 | +0.46% |

| AUD/USD | 0.70 | -1.52% |

| NZD/USD | 0.58 | -1.50% |

| AUD/NZD | 1.21 | +0.03% |

| BHP | 61.24 | -2.48% |

| Gold | 4,365.30 | -2.47% |

| Brent Crude | 93.09 | -2.04% |

| Bitcoin | 61,207.14 | +0.56% |

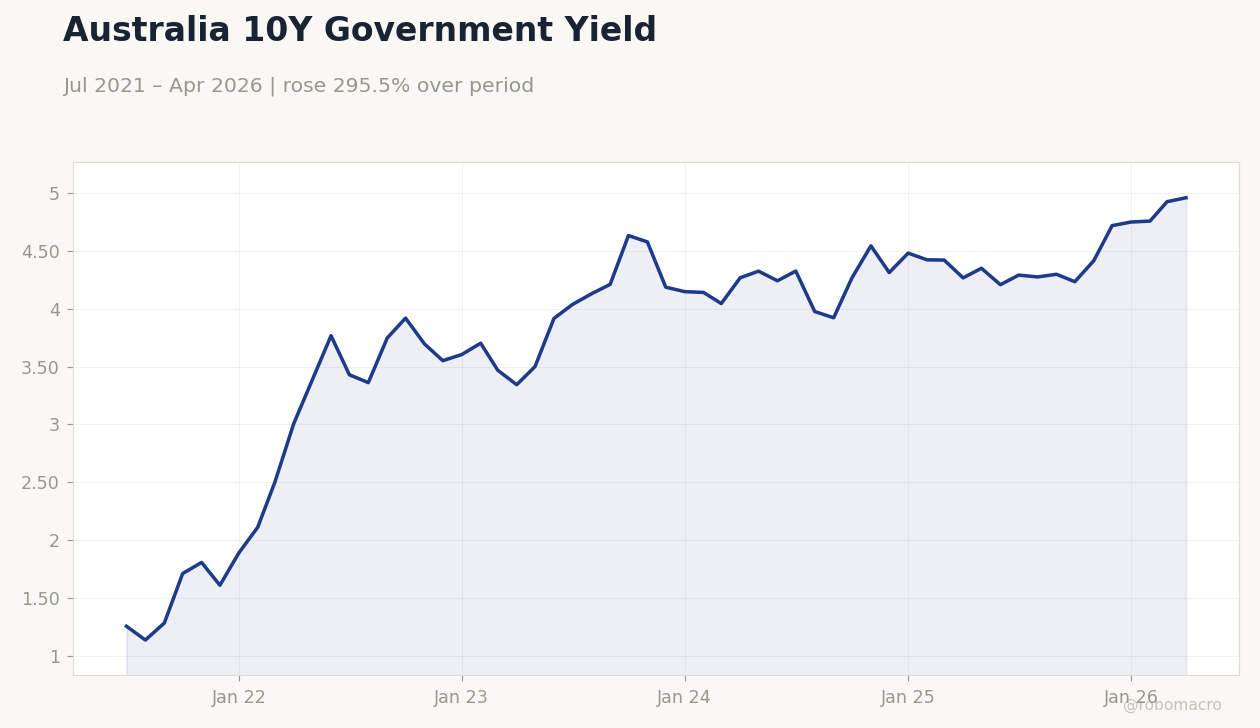

| Australia 10Y Govt Yield | 4.96% | +0.69% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Australia 10Y Government Yield | Type: macro_line | Yield %: 4.96 (2026-04-01) | Range: 1.135–4.96 | Trend(6pt): 1.254,3.747,4.578,4.481,4.926,4.96

Australia 10Y Government Yield | Type: macro_line | Yield %: 4.96 (2026-04-01) | Range: 1.135–4.96 | Trend(6pt): 1.254,3.747,4.578,4.481,4.926,4.96

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Westpac Consumer Confidence Change | 3.50 | - | 20:30 |

| Westpac Consumer Confidence Index | 83 | - | 20:30 |

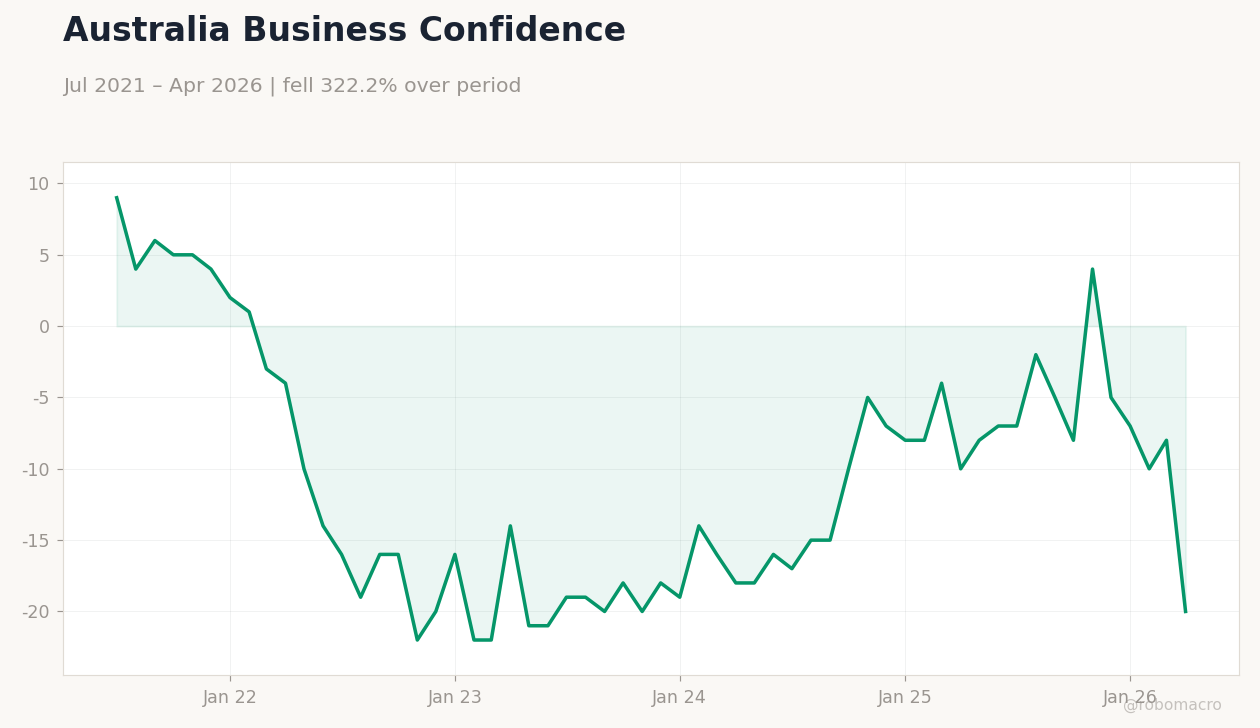

| NAB Business Confidence Index | -24 | - | 21:30 |

| Business NZ PMI | 50.50 | - | 18:30 |

- Australian Q1 GDP slowed to 0.3% q/q amid higher rates and fuel pressures, while inflation moderated.

- ASX 200 fell 0.70% and AUD/USD dropped 1.52% to 0.70; NZX 50 rose 0.46%.

- RBA cash rate steady at 4.10%; markets price earlier RBNZ hikes.

Yesterday's Recap

Australian equity and currency markets weakened on Friday as GDP growth slowed sharply to 0.3% in the March quarter. The ASX 200 closed at 8,625.10, down 0.70%, with BHP falling 2.48% to 61.24. AUD/USD declined 1.52% to 0.70 while NZD/USD fell 1.50% to 0.58.

The NZX 50 advanced 0.46% to 13,161.97, supported by dairy and utility names. Australian 10-year yields rose 0.69% to 4.96% and NZ short-term rates fell 9.60% to 4.33%. No major data releases occurred on 6 June.

Gold and Brent crude both declined more than 2%, weighing on commodity-linked AUD.

The Day Ahead

Westpac Consumer Confidence Change and Index for Australia are due at 20:30 ET on 8 June, followed by NAB Business Confidence at 21:30 ET. New Zealand releases Business NZ PMI at 18:30 ET on 11 June. Markets will monitor these sentiment gauges for signs of consumer and business resilience after the weak GDP print.

China trade data later in the week will influence iron-ore and AUD direction. No RBA or RBNZ policy meetings are scheduled this week.

Other Economic Notes

Australia’s economy is contracting under the weight of prior rate rises, elevated government spending and fuel costs. Commodity exports remain the key buffer, with iron ore and LNG prices still supportive of the trade balance. New Zealand’s dairy sector and tourism receipts continue to underpin NZD, though housing approvals data show only modest recovery.

Both economies remain tightly linked to Chinese steel output and consumer demand.

Global Macro News

China and New Zealand held bilateral trade talks in Beijing to deepen cooperation on goods and services flows. Japan’s prime minister pledged to defend the yen through domestic growth rather than direct intervention. Global risk sentiment stayed mixed as Bitcoin rose 0.56% while gold and oil fell.

Protectionism concerns prompted RBNZ’s Breman to note New Zealand is finding alternative supply solutions. Australian inflation moderation has not yet translated into clear RBA easing signals. Broader USD strength contributed to the 1.5% drop in both AUD and NZD.