ANZ Macro Daily(Beta Mode)

AUD Slides as Regional Sentiment Weakens

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,625.10 | -0.70% |

| NZX 50 | 13,038.24 | -0.94% |

| AUD/USD | 0.70 | -1.18% |

| NZD/USD | 0.58 | -1.00% |

| AUD/NZD | 1.21 | -0.29% |

| BHP | 61.24 | -2.48% |

| Gold | 4,351.70 | +0.34% |

| Brent Crude | 94.22 | +1.21% |

| Bitcoin | 63,463.99 | +0.35% |

| Australia 10Y Govt Yield | 4.96% | +0.69% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Australia 10Y Govt Yield | Type: macro_line | Percent: 4.96 (2026-04-01) | Range: 1.135–4.96 | Trend(6pt): 1.254,3.747,4.578,4.481,4.926,4.96

Australia 10Y Govt Yield | Type: macro_line | Percent: 4.96 (2026-04-01) | Range: 1.135–4.96 | Trend(6pt): 1.254,3.747,4.578,4.481,4.926,4.96

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Westpac Consumer Confidence Change | 3.50 | - | 20:30 |

| Westpac Consumer Confidence Index | 83 | - | 20:30 |

| NAB Business Confidence Index | -24 | - | 21:30 |

| RBA Bulletin | - | - | 21:30 |

| Business NZ PMI | 50.50 | - | 18:30 |

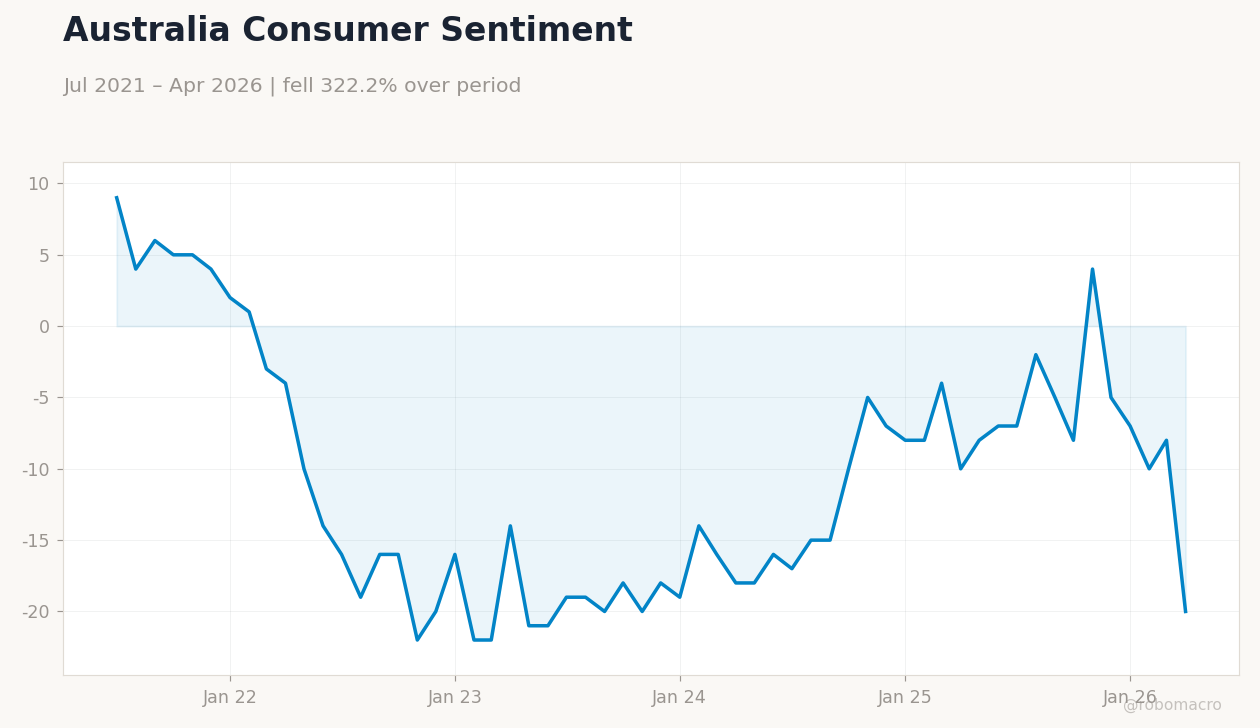

- Australian consumer and business surveys due today flag softening domestic demand

- AUD/USD drops 1.18% to 0.70 while ASX 200 and NZX 50 both decline

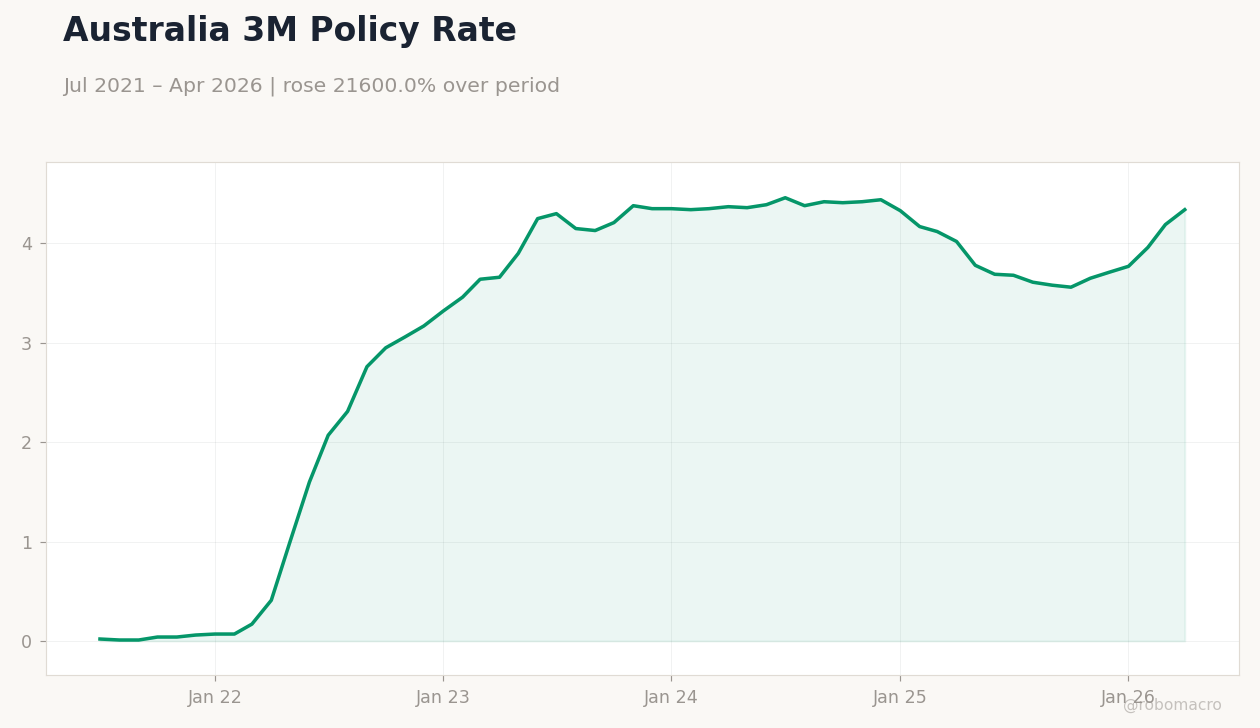

- RBA holds cash rate at 4.10% as RBNZ eyes possible August easing

Yesterday's Recap

No economic data releases were published in Australia or New Zealand on 7 June. Equity markets fell across the region, with the ASX 200 declining 0.70% to 8,625.10 and the NZX 50 retreating 0.94% to 13,038.24. The Australian dollar came under pressure, sending AUD/USD 1.18% lower to 0.70 and AUD/NZD 0.29% weaker to 1.21.

New Zealand’s short-term rate fell sharply to 4.33%. BHP shares dropped 2.48% to 61.24 amid softer commodity sentiment, while gold rose 0.34% to 4,351.70 and Brent crude gained 1.21% to 94.22. Australian 10-year government yields climbed 0.69% to 4.96%.

The Day Ahead

Australia will release the Westpac Consumer Confidence Change and Index at 20:30 ET, followed by the NAB Business Confidence Index and RBA Bulletin at 21:30 ET. These releases will update household and business sentiment readings after recent soft GDP and retail sales prints. New Zealand’s Business NZ PMI is scheduled for 11 June and will provide the next manufacturing gauge.

Markets will scrutinise the RBA Bulletin for any fresh guidance on the 4.10% cash rate. No other major ANZ events are listed for the immediate session.

Other Economic Notes

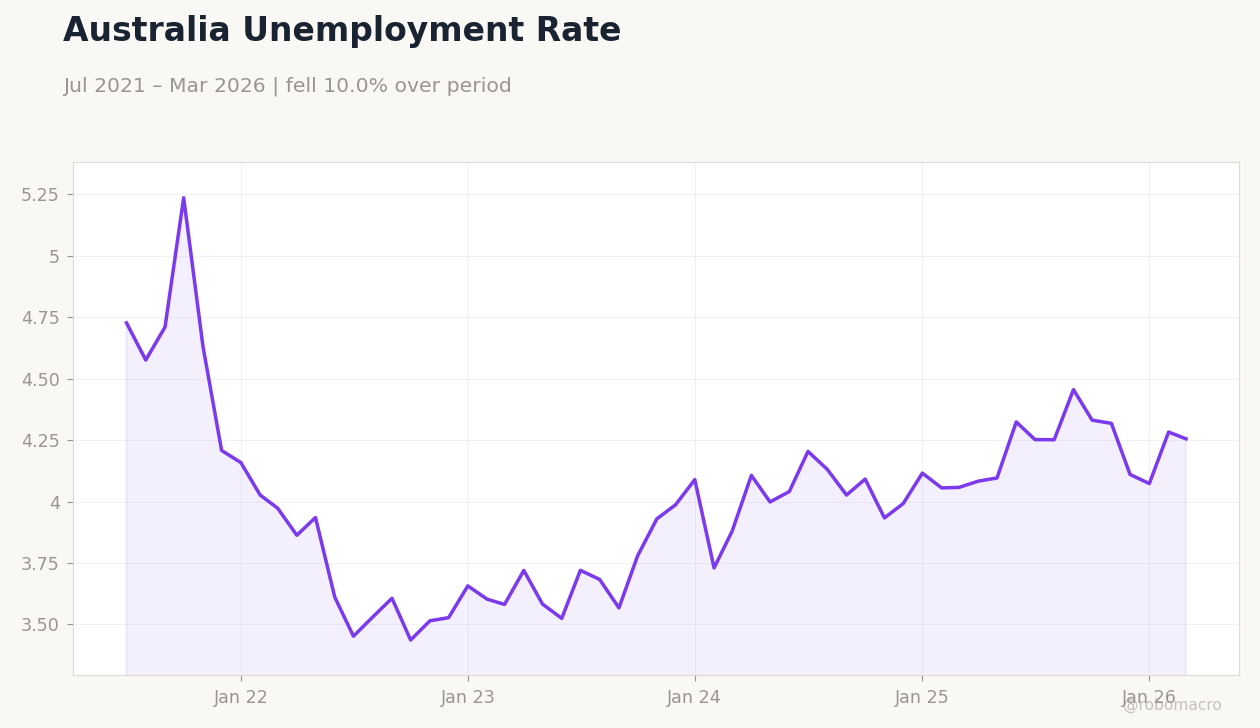

Australia’s Q1 GDP growth slowed amid higher borrowing costs and fuel-price pressures. Commodity export revenues remain the key swing factor for the trade balance and AUD. New Zealand continues to face softer dairy prices that widen the current-account deficit.

Housing credit growth in both countries has moderated in response to elevated policy rates. China demand signals stay the dominant external driver for Australian iron-ore and coal volumes.

Global Macro News

The US dollar climbed to a two-month high after strong US jobs data lifted Fed hike expectations and weighed on AUD and NZD. Renewed Chinese stimulus hopes lifted iron-ore futures, supporting Australian terms of trade. Brent crude rose 1.21% to 94.22, adding to domestic fuel-cost pressures.

South Korean won-dollar volatility highlighted regional currency stress. The Japanese yen remained under pressure despite a softer US dollar tone. These external moves reinforce downside risks to ANZ growth and inflation outlooks through trade and financial channels.