ANZ Macro Daily(Beta Mode)

NAB Tips RBA Cuts as AU Confidence Slips

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,625.10 | -0.70% |

| NZX 50 | 13,204.08 | +1.27% |

| AUD/USD | 0.70 | -0.28% |

| NZD/USD | 0.58 | +0.30% |

| AUD/NZD | 1.21 | -0.64% |

| BHP | 60.08 | -1.89% |

| Gold | 4,284.80 | -1.18% |

| Brent Crude | 91.83 | -2.57% |

| Bitcoin | 61,862.44 | -1.95% |

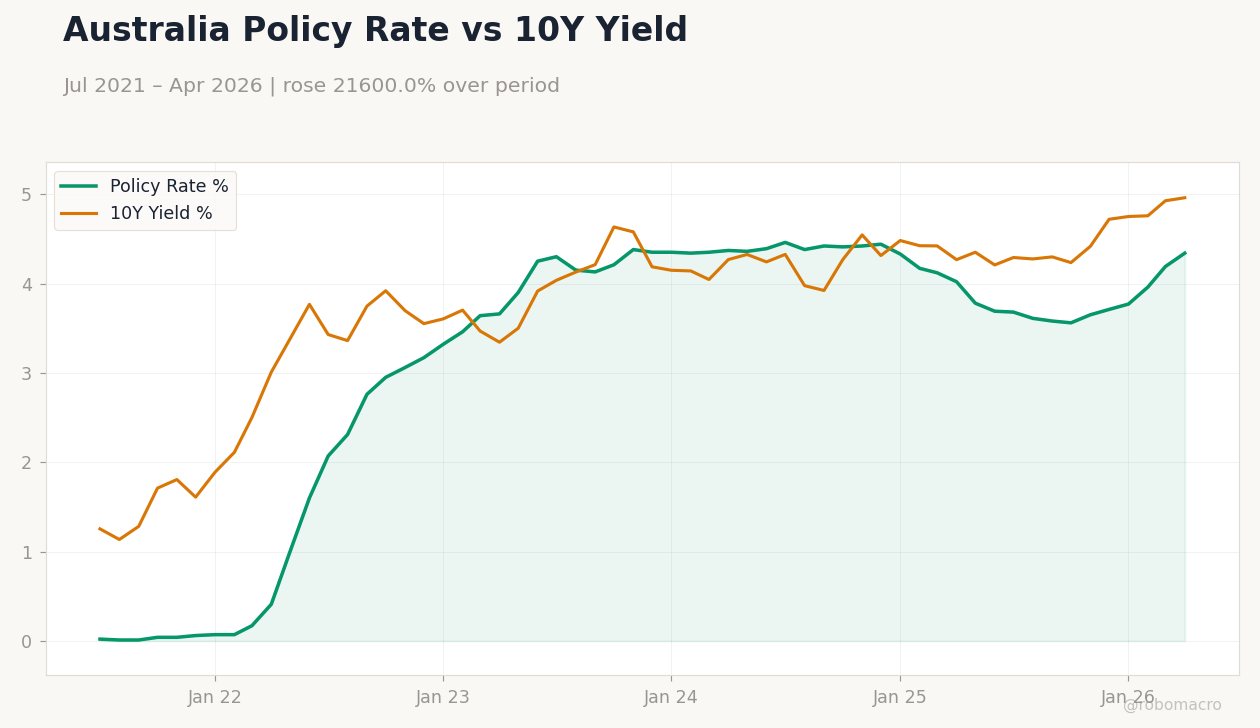

| Australia 10Y Govt Yield | 4.96% | +0.69% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

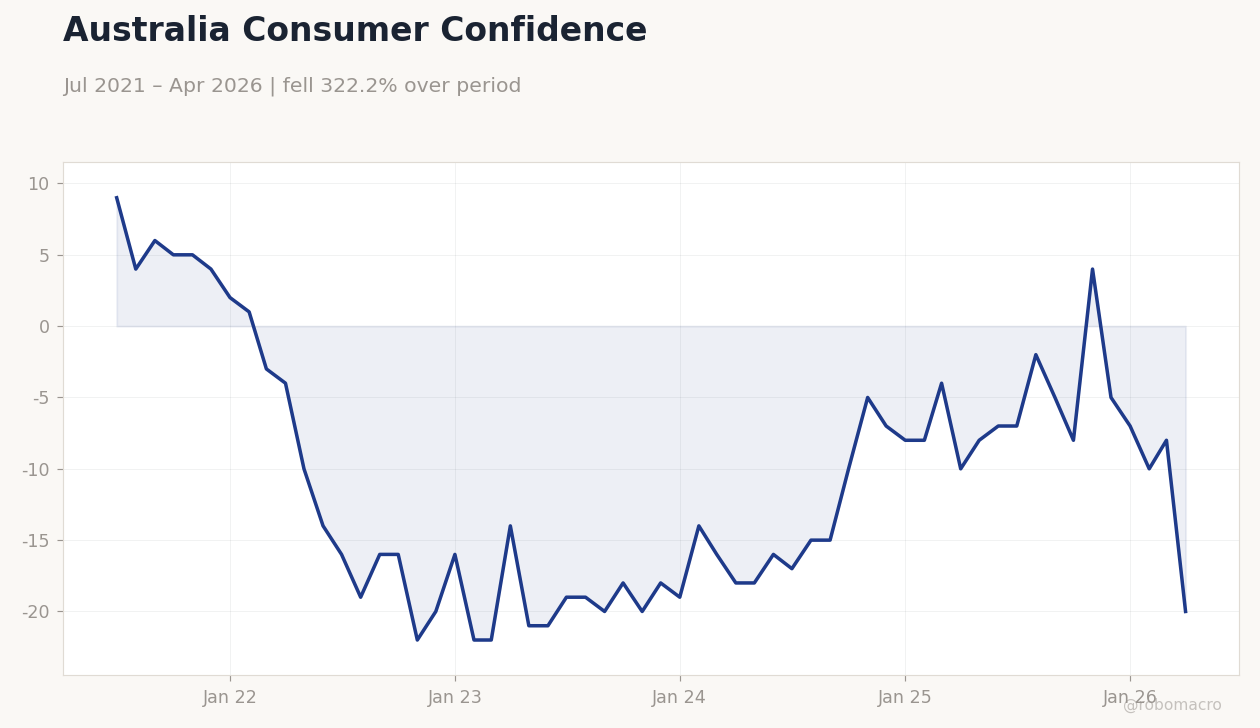

| Westpac Consumer Confidence Change | 3.50 | - | -2.90 |

| Westpac Consumer Confidence Index | 83 | - | 80.60 |

| NAB Business Confidence Index | -23 | - | -14 |

| RBA Bulletin | - | - | "" |

Australia Consumer Confidence | Type: macro_line | Index: -20 (2026-04-01) | Range: -22–9 | Trend(6pt): 9,-16,-20,-8,-8,-20

Australia Consumer Confidence | Type: macro_line | Index: -20 (2026-04-01) | Range: -22–9 | Trend(6pt): 9,-16,-20,-8,-8,-20

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Business NZ PMI | 50.50 | - | 14:30 |

- Westpac consumer confidence fell sharply in Australia while NAB business confidence improved, signalling uneven domestic momentum.

- NAB joined peers in forecasting RBA rate cuts as cooling cost pressures and weaker household sentiment point to policy easing ahead.

- NZD outperformed AUD on manufacturing resilience, while ASX 200 declined and NZX 50 rose amid divergent equity flows.

Yesterday's Recap

Australian data dominated 8 June releases. Westpac consumer confidence dropped 2.9 points to 80.6, its weakest reading in months, while the index itself fell from 83. NAB business confidence rose from -23 to -14, showing partial stabilisation in corporate sentiment.

The RBA Bulletin offered no new policy signals. Markets reacted with the ASX 200 falling 0.70% to 8,625.10 and AUD/USD slipping 0.28% to 0.70. In New Zealand the NZX 50 gained 1.27% to 13,204.08 and NZD/USD rose 0.30% to 0.58.

The RBA cash rate remained at 4.10%. Commodity prices weighed on sentiment, with BHP down 1.89% and Brent crude falling 2.57%.

The Day Ahead

Attention shifts to New Zealand with the Business NZ PMI scheduled for release on 11 June. The prior reading of 50.5 suggests manufacturing activity remains marginally expansionary. No major Australian data prints are listed for 9-10 June.

Markets will monitor AUD/NZD, currently at 1.21, for any further divergence driven by policy expectations. RBA speakers and any follow-up commentary on the Bulletin may provide incremental guidance. Equity and currency volatility is likely to stay contained ahead of the PMI.

Other Economic Notes

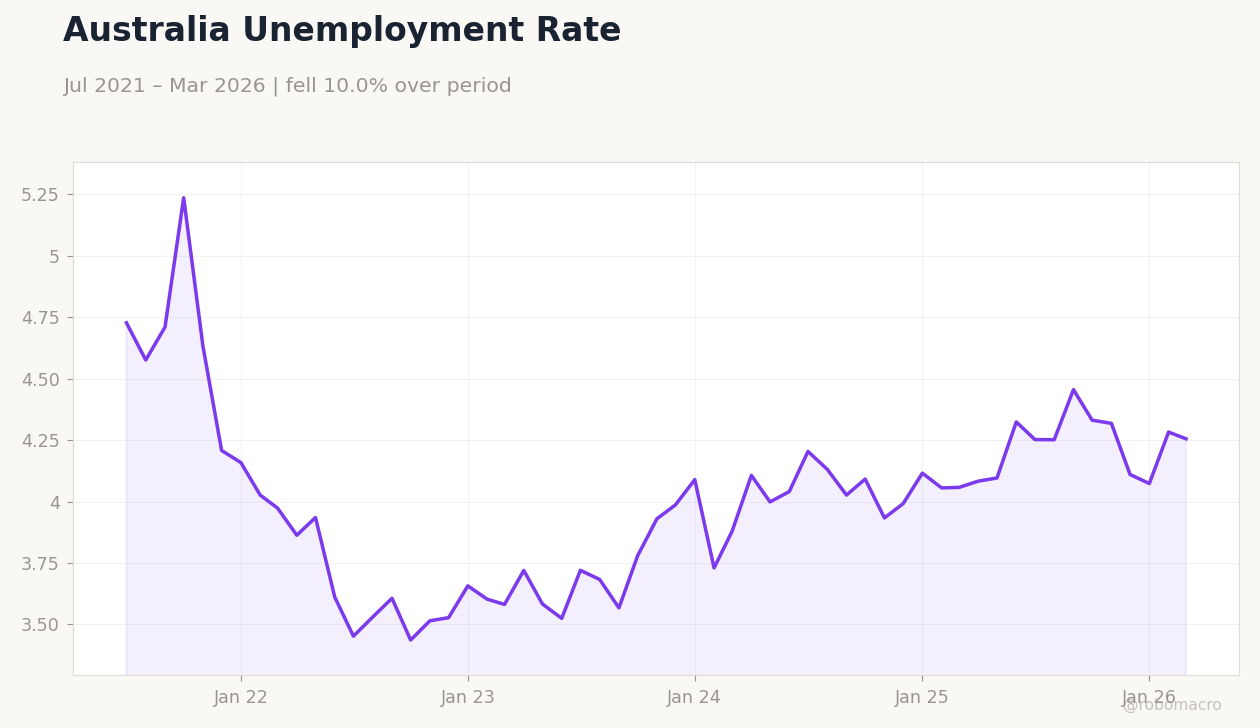

Australia's economy shows clear signs of cooling after successive rate hikes, with consumer weakness now more pronounced than business sentiment. NAB's shift toward expecting RBA cuts reflects easing cost pressures and slower growth momentum. New Zealand manufacturing sales have surged, supporting the NZD but potentially delaying RBNZ easing.

Both economies remain sensitive to China demand given Australia's commodity exports and New Zealand's dairy and tourism links. Housing markets in both countries continue to transmit policy effects through mortgage rates and credit availability.

Global Macro News

Global commodity markets eased, with gold down 1.18% and Brent crude falling sharply, pressuring Australian export revenues. Yen remained above 160 against the dollar ahead of the BOJ meeting, keeping carry-trade flows in focus for AUD and NZD. <i>↓ p.2</i>