ANZ Macro Daily(Beta Mode)

AU Confidence Slips, RBA Rate-Cut Bets Rise

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,604.20 | -0.24% |

| NZX 50 | 13,204.08 | +1.27% |

| AUD/USD | 0.70 | -0.59% |

| NZD/USD | 0.58 | -0.15% |

| AUD/NZD | 1.21 | -0.18% |

| BHP | 60.20 | +0.20% |

| Gold | 4,094.10 | -3.89% |

| Brent Crude | 94.71 | +3.56% |

| Bitcoin | 61,271.25 | -0.60% |

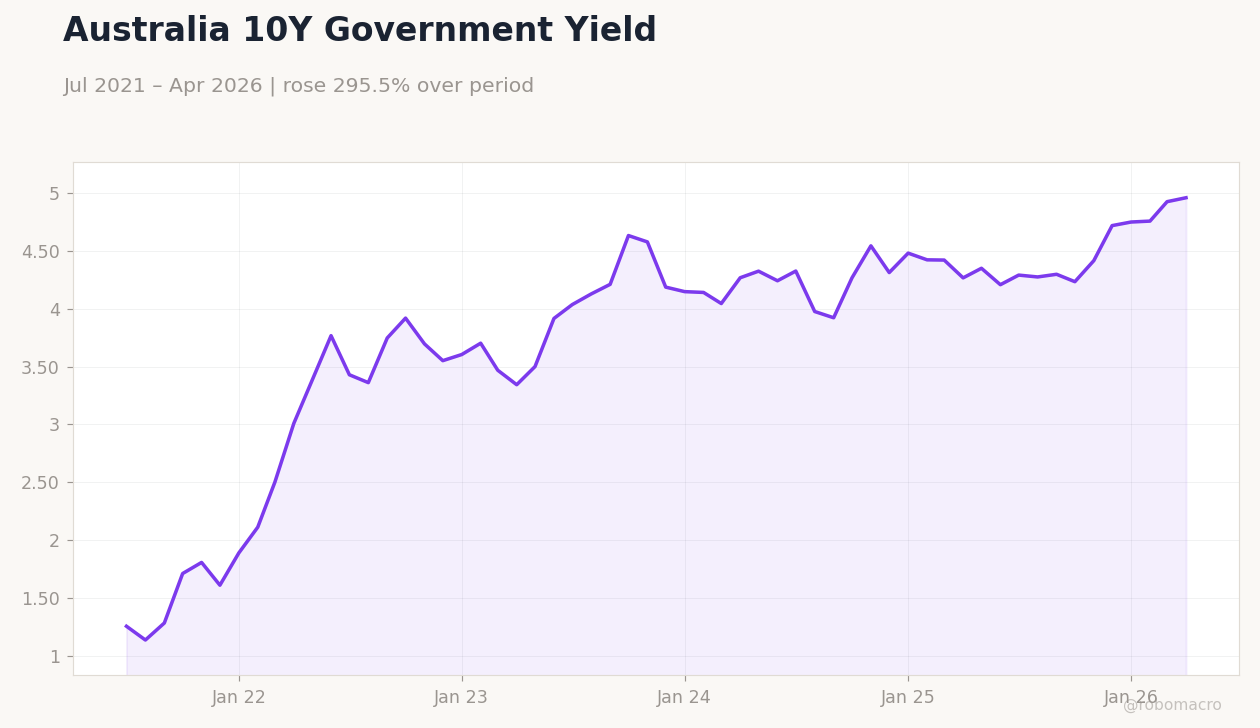

| Australia 10Y Govt Yield | 4.96% | +0.69% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

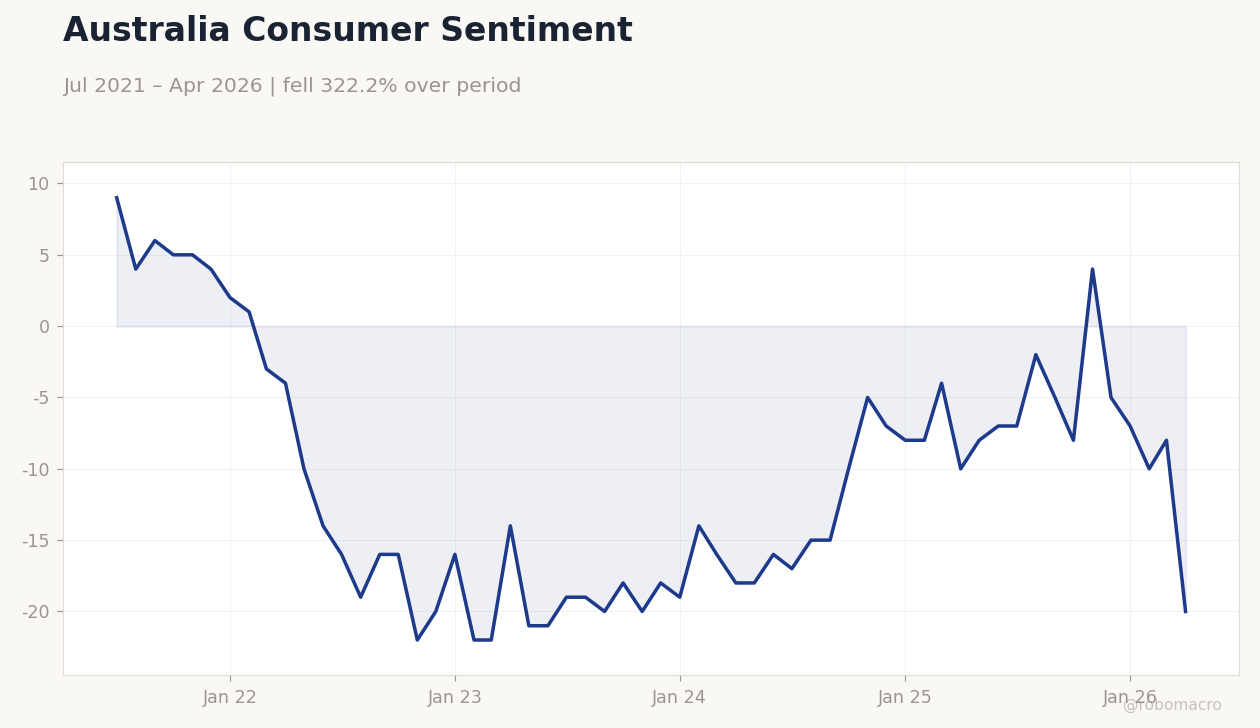

| Westpac Consumer Confidence Change | 3.50 | - | -2.90 |

| Westpac Consumer Confidence Index | 83 | - | 80.60 |

| NAB Business Confidence Index | -23 | - | -14 |

| RBA Bulletin | - | - | "" |

Australia Consumer Sentiment | Type: macro_line | Consumer Sentiment Index: -20 (2026-04-01) | Range: -22–9 | Trend(6pt): 9,-16,-20,-8,-8,-20

Australia Consumer Sentiment | Type: macro_line | Consumer Sentiment Index: -20 (2026-04-01) | Range: -22–9 | Trend(6pt): 9,-16,-20,-8,-8,-20

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Business NZ PMI | 50.50 | - | 14:30 |

| Thursday (2026-06-11) | |||

| Business NZ PMI | 50.50 | - | 14:30 |

- Australian consumer confidence fell to 80.6 in June while NAB business confidence improved to -14.

- Markets now price lower odds of further RBA hikes after NAB forecast a rate cut ahead.

- NZX 50 rose 1.27% as manufacturing sales strength clouds RBNZ easing prospects.

Yesterday's Recap

Australian data showed Westpac consumer confidence dropping 2.9 points to an index level of 80.6, reversing the prior 3.5-point gain and signalling weaker household sentiment. NAB business confidence rose to -14 from -23, indicating some stabilisation in corporate conditions. The RBA released its monthly Bulletin without new policy signals.

The ASX 200 closed at 8,604.20, down 0.24%, while the NZX 50 advanced 1.27% to 13,204.08. AUD/USD fell 0.59% to 0.70 amid reduced hike pricing, and Australian 10-year yields rose 0.69% to 4.96%. NZ short-term rates declined sharply.

News flow highlighted NAB joining peers in expecting RBA cuts rather than further tightening.

The Day Ahead

Markets await the Business NZ PMI release at 14:30 NZ time, which will provide the latest reading on manufacturing activity. The outcome will inform views on whether recent sales strength persists into June. No major Australian data prints are scheduled.

Attention will also turn to any follow-up commentary from RBA officials on the Bulletin. Positioning in AUD and NZD is expected to remain sensitive to shifts in rate-cut probabilities.

Other Economic Notes

European capital inflows continue to support Australian infrastructure and transition projects, widening the pipeline of investment. China demand signals remain the dominant external driver for Australian commodity exports including iron ore and LNG. Housing market softness is increasingly viewed as helpful for RBA policy calibration given its impact on household spending.

New Zealand’s terms of trade face ongoing pressure from softer dairy prices despite manufacturing resilience.

Global Macro News

Indonesia’s economy faces a confidence-driven doom loop that could spill into regional risk sentiment. Japan’s prime minister pledged to defend the yen through domestic growth measures rather than direct intervention. South Korea’s Q1 GDP was revised higher to 1.8%, showing resilient external demand.

<i>↓ p.2</i>