ANZ Macro Daily(Beta Mode)

ASX Climbs on RBA Hold Bets, NZ PMI Weakens

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,804.00 | +1.98% |

| NZX 50 | 13,393.87 | +1.45% |

| AUD/USD | 0.70 | +0.01% |

| NZD/USD | 0.58 | +0.04% |

| AUD/NZD | 1.21 | -0.08% |

| BHP | 62.93 | +3.50% |

| Gold | 4,238.80 | +3.63% |

| Brent Crude | 87.33 | -3.37% |

| Bitcoin | 63,798.00 | -0.97% |

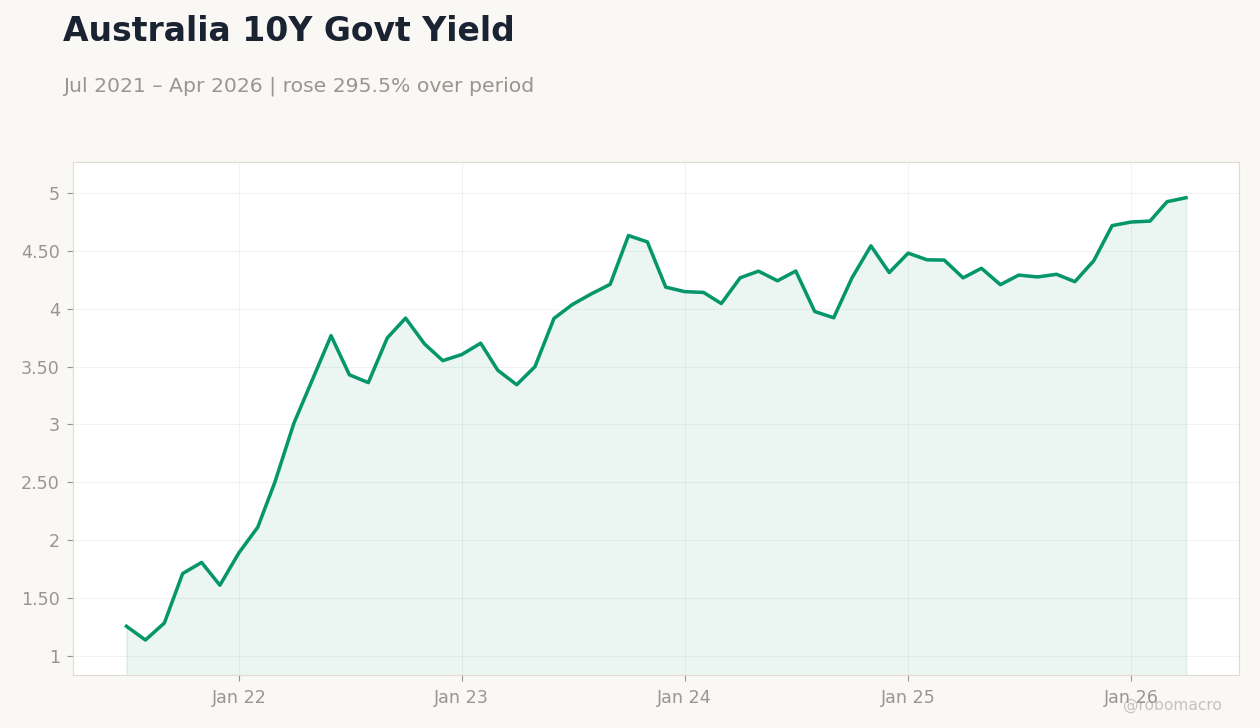

| Australia 10Y Govt Yield | 4.96% | +0.69% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

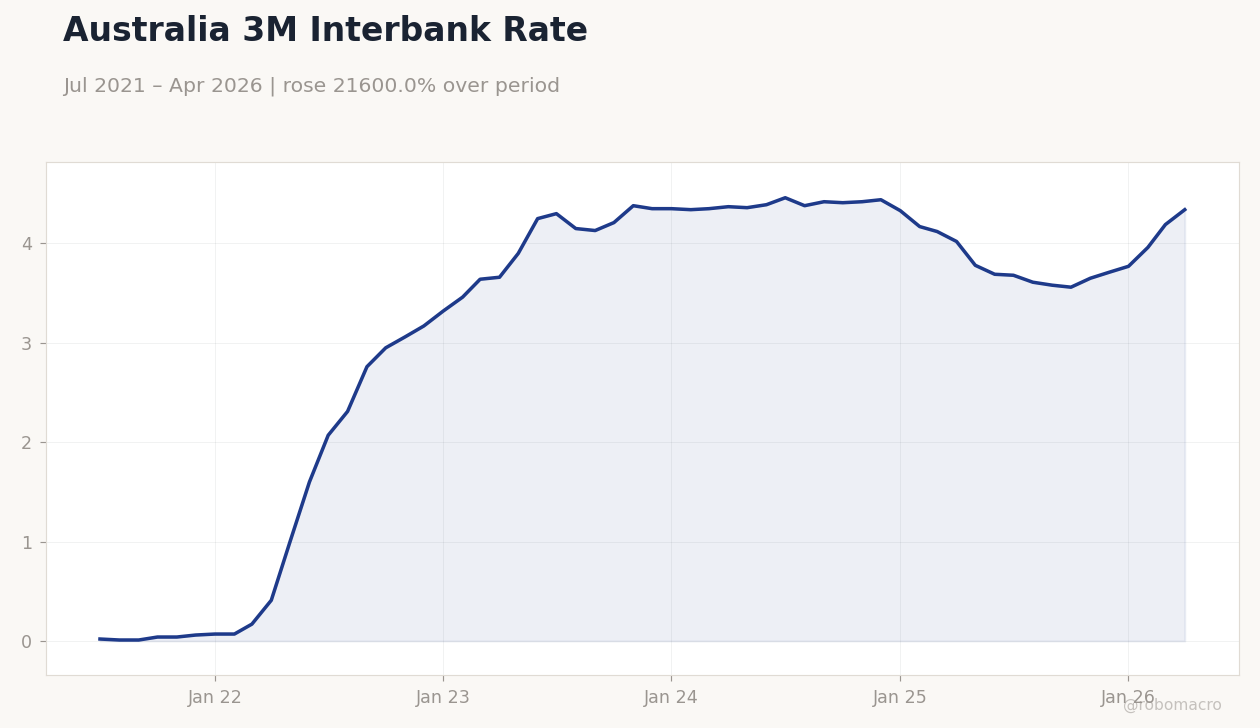

Australia 3M Interbank Rate | Type: macro_line | Percent: 4.34 (2026-04-01) | Range: 0.01–4.46 | Trend(6pt): 0.02,2.76,4.38,4.33,4.19,4.34

Australia 3M Interbank Rate | Type: macro_line | Percent: 4.34 (2026-04-01) | Range: 0.01–4.46 | Trend(6pt): 0.02,2.76,4.38,4.33,4.19,4.34

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| RBA Interest Rate Decision | 4.35 | 4.35 | 00:30 |

| RBA Press Conference | - | - | 01:30 |

| Current Account Balance | -5,980m | -1,190m | 18:45 |

| RBA Jones Speech | - | - | 21:30 |

| GDP Growth Quarter-over-Quarter | 0.20 | 0.90 | 18:45 |

| GDP Growth Year-over-Year | 1.30 | 1.10 | 18:45 |

| Trade Balance | 1,920m | 875m | 18:45 |

- ASX 200 jumped 1.98% to 8,804 as markets priced in RBA hold; NZX 50 gained 1.45% to 13,393.87.

- AUD/USD rose to 0.70 while NZD/USD climbed to 0.58; gold surged 3.63% to 4,238.80.

- RBA cash rate stands at 4.10%; upcoming June decision and NZ GDP prints dominate focus.

Yesterday's Recap

Australian equities rallied sharply with the ASX 200 adding 1.98% to close at 8,804, driven by BHP’s 3.50% gain amid firmer iron-ore prices. The NZX 50 advanced 1.45% to 13,393.87 on defensive buying. AUD/USD lifted 0.01% to 0.70 and NZD/USD rose 0.04% to 0.58, narrowing AUD/NZD by 0.08% to 1.21.

Australian 10-year yields climbed 0.69% to 4.96% while NZ short-term rates fell 9.60% to 4.33%. Brent crude dropped 3.37% to 87.33 and bitcoin eased 0.97% to 63,798. No major ANZ data releases occurred on 13 June, leaving market moves driven by positioning ahead of the RBA decision.

The Day Ahead

Markets await the RBA interest-rate decision and press conference on 16 June, with consensus pointing to a hold at 4.10%. The RBA Jones speech later that day will provide further guidance on inflation persistence. New Zealand releases the current-account balance on 16 June, followed by Q2 GDP prints on 17 June that are expected to show 0.9% quarter-over-quarter growth.

The NZ trade balance on 18 June completes the near-term calendar. China demand signals overnight will influence iron-ore and AUD direction.

Other Economic Notes

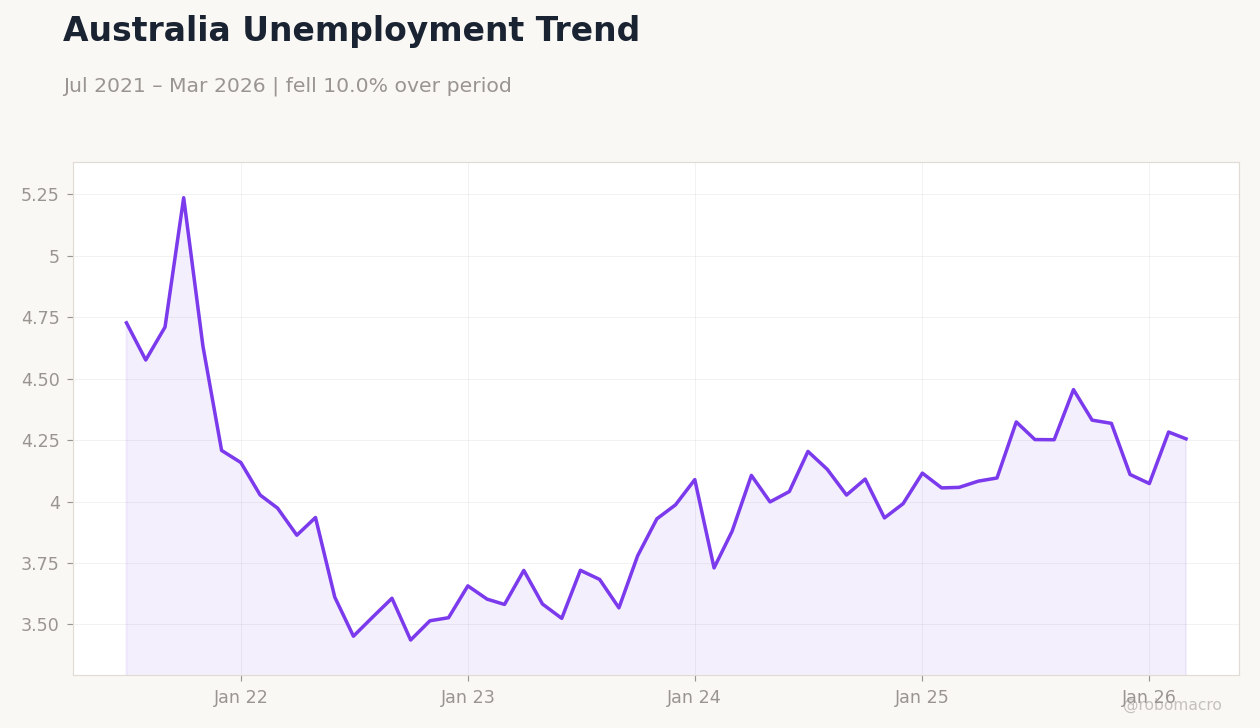

Australia’s commodity-export model remains tightly linked to Chinese stimulus expectations, with BHP serving as the key bellwether for mining sentiment. New Zealand’s dairy and tourism sectors face headwinds from softer global growth and a widening current-account gap. Housing markets in both countries continue to show resilience despite higher-for-longer rates, supporting household balance sheets.

Terms-of-trade gains from gold and iron ore continue to underpin AUD outperformance versus NZD.

Global Macro News

Hotter US PPI data lifted the dollar and pressured commodity currencies outside ANZ. Chinese stimulus speculation supported iron-ore futures and lifted Australian export forecasts. Global equity sentiment improved on expectations of a soft US landing, aiding risk assets in Australia and New Zealand.

<i>↓ p.2</i>