ANZ Macro Daily(Beta Mode)

RBA Holds as Ceasefire Lifts AUD

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,804.00 | +1.98% |

| NZX 50 | 13,360.59 | -0.25% |

| AUD/USD | 0.71 | +0.35% |

| NZD/USD | 0.58 | -0.15% |

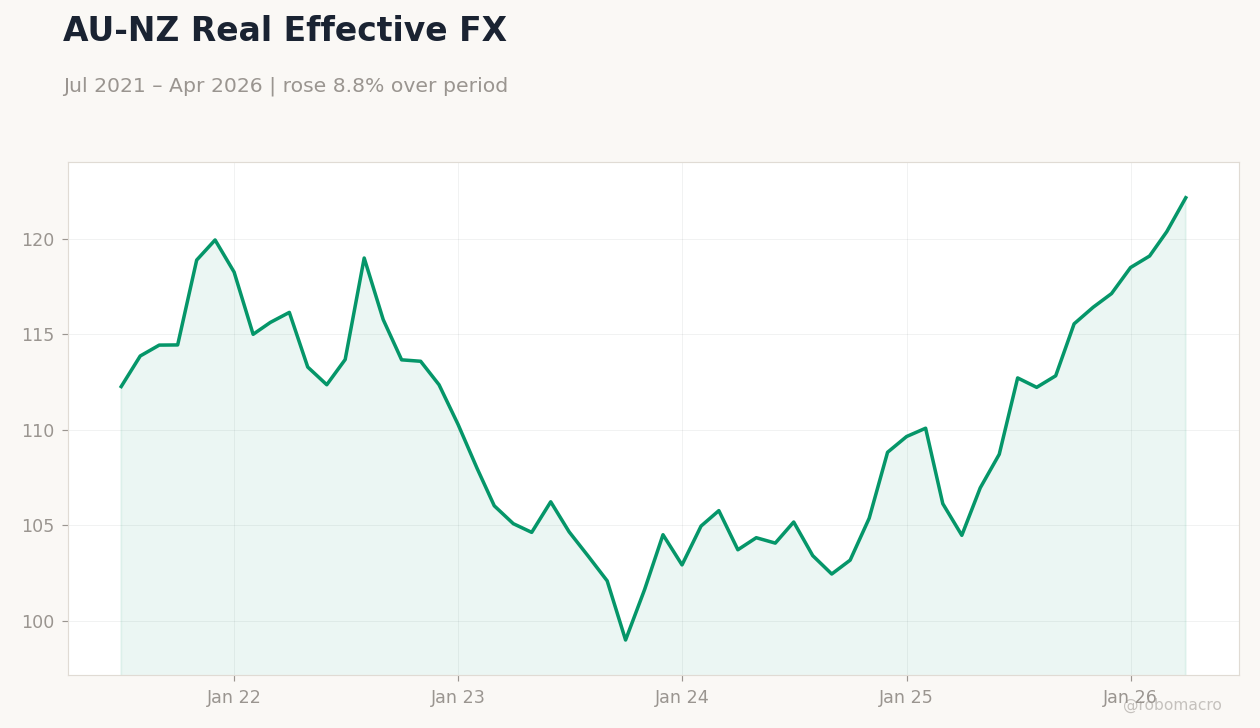

| AUD/NZD | 1.21 | +0.36% |

| BHP | 62.93 | +3.50% |

| Gold | 4,332.50 | +2.79% |

| Brent Crude | 83.51 | -4.37% |

| Bitcoin | 66,487.44 | +1.18% |

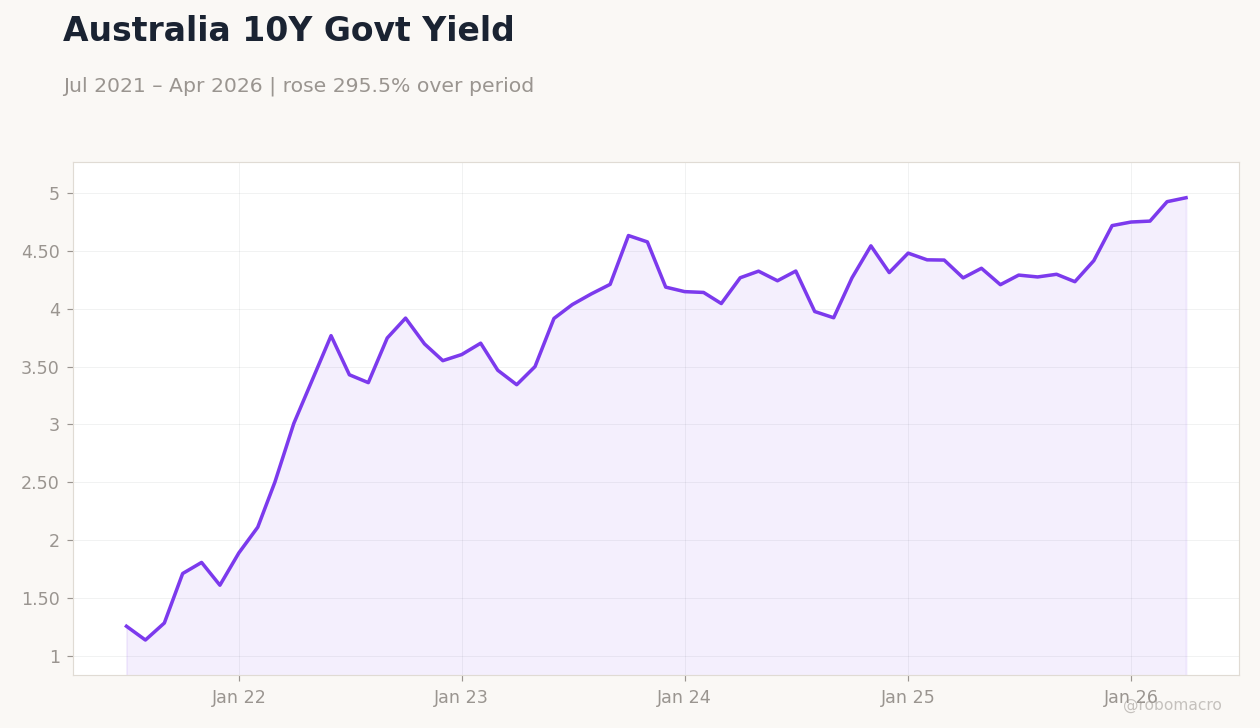

| Australia 10Y Govt Yield | 4.96% | +0.69% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

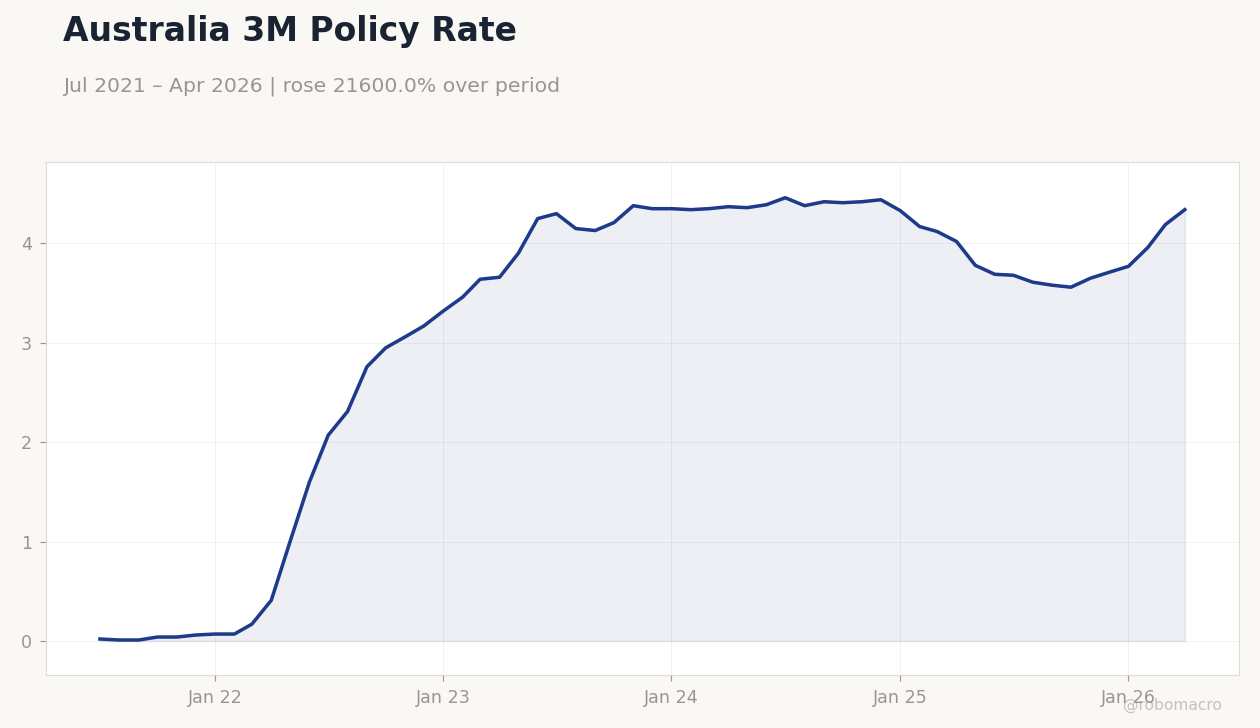

Australia 3M Policy Rate | Type: macro_line | Percent: 4.34 (2026-04-01) | Range: 0.01–4.46 | Trend(6pt): 0.02,2.76,4.38,4.33,4.19,4.34

Australia 3M Policy Rate | Type: macro_line | Percent: 4.34 (2026-04-01) | Range: 0.01–4.46 | Trend(6pt): 0.02,2.76,4.38,4.33,4.19,4.34

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| RBA Interest Rate Decision | 4.35 | 4.35 | 00:30 |

| RBA Press Conference | - | - | 01:30 |

| Current Account Balance | -5,980m | -1,190m | 18:45 |

| RBA Jones Speech | - | - | 21:30 |

| GDP Growth Quarter-over-Quarter | 0.20 | 0.90 | 18:45 |

| GDP Growth Year-over-Year | 1.30 | 1.10 | 18:45 |

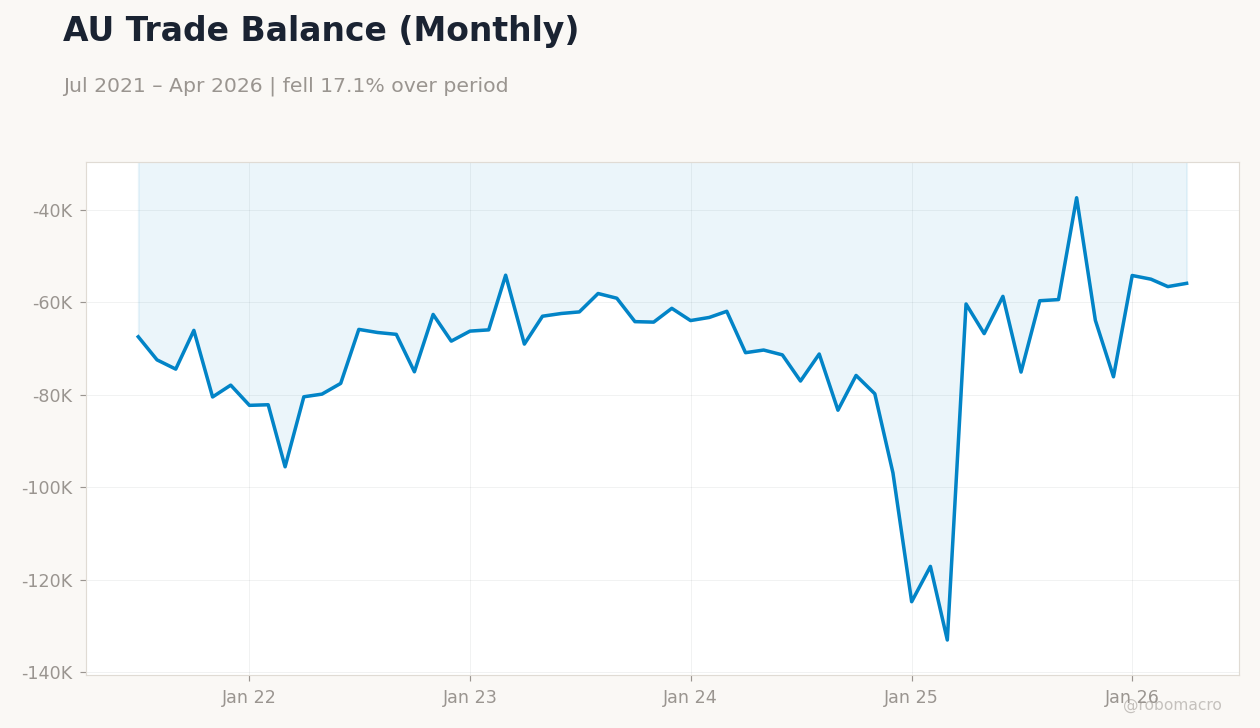

| Trade Balance | 1,920m | 875m | 18:45 |

| S&P Global Manufacturing PMI Flash | 50.70 | - | 19:00 |

| S&P Global Services PMI Flash | 48.70 | - | 19:00 |

- RBA holds cash rate at 4.10% with hawkish pause signalling data dependence ahead of CPI

- ASX 200 surges 1.98% to 8,804 while AUD/USD climbs to 0.71 on USD weakness

- NZ manufacturing PMI contracts and services PSI falls to 47.5, tilting RBNZ toward cuts

Yesterday's Recap

Australian markets rallied on the US-Iran ceasefire and firmer iron-ore prices, lifting the ASX 200 1.98% to 8,804 and BHP 3.50% to 62.93. The Australian dollar gained 0.35% to 0.71 against the USD as safe-haven demand eased. New Zealand equities slipped 0.25% to 13,360.59 with the NZX 50 pressured by softer domestic data.

NZD/USD fell 0.15% to 0.58 while the AUD/NZD cross rose 0.36% to 1.21. Australian 10-year yields rose 0.69% to 4.96% and NZ short-term rates dropped 9.60% to 4.33%. Gold advanced 2.79% to 4,332.50 on geopolitical relief flows, while Brent crude fell 4.37% to 83.51.

No major ANZ data releases occurred on 14 June.

The Day Ahead

The RBA will announce its interest-rate decision at 00:30 ET on 16 June with consensus pointing to a hold at 4.10% followed by Governor’s press conference. New Zealand releases its current-account balance at 18:45 ET, expected to narrow sharply to -1.19 billion NZD. RBA’s Jones is scheduled to speak at 21:30 ET, likely reinforcing the data-dependent stance.

Markets will also monitor any updates on Australian CPI prints due later in the week.

Other Economic Notes

Australia’s commodity-export model remains tightly linked to Chinese steel output and credit growth, with iron-ore strength directly supporting AUD terms of trade. New Zealand’s dairy and tourism sectors continue to face soft domestic demand, evident in the recent retail-sales contraction. Housing-finance approvals in Australia rose modestly while NZ house prices stayed flat, keeping both central banks focused on household balance-sheet risks.

Late business-payment delays hitting six-year highs add downside risk to Australian growth.

Global Macro News

The US-Iran ceasefire reduced safe-haven bids for the dollar, providing broad support to commodity currencies including the AUD. Hotter US PPI prints kept Treasury yields elevated and capped further AUD gains. Chinese industrial-production data surprised to the upside, bolstering iron-ore and Australian mining equities.

<i>↓ p.2</i>