ANZ Macro Daily(Beta Mode)

RBA Holds at 4.35% as NZ Sales Rebound

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,914.00 | +1.25% |

| NZX 50 | 13,426.13 | +0.49% |

| AUD/USD | 0.71 | -0.09% |

| NZD/USD | 0.58 | -0.37% |

| AUD/NZD | 1.21 | +0.25% |

| BHP | 65.19 | +0.02% |

| Gold | 4,358.20 | +0.70% |

| Brent Crude | 79.73 | -4.14% |

| Bitcoin | 65,610.32 | -1.02% |

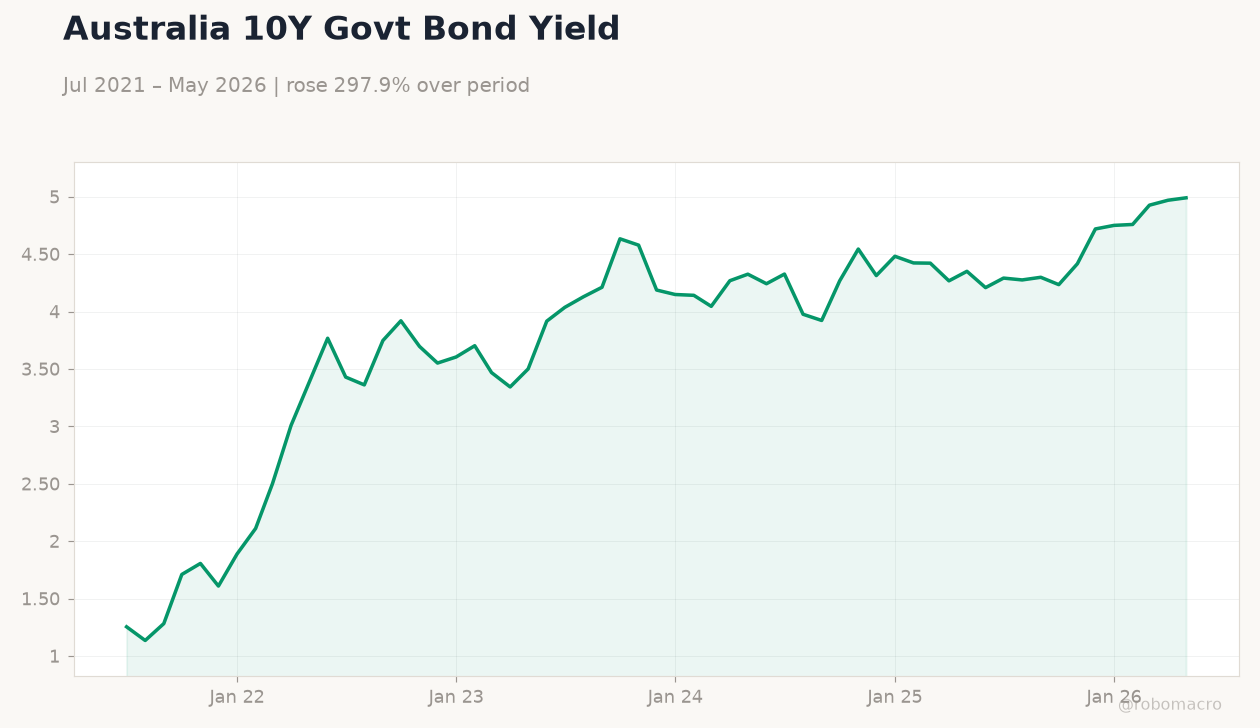

| Australia 10Y Govt Yield | 4.99% | +0.42% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| RBA Interest Rate Decision | 4.35 | 4.35 | 4.35 |

| RBA Press Conference | - | - | - |

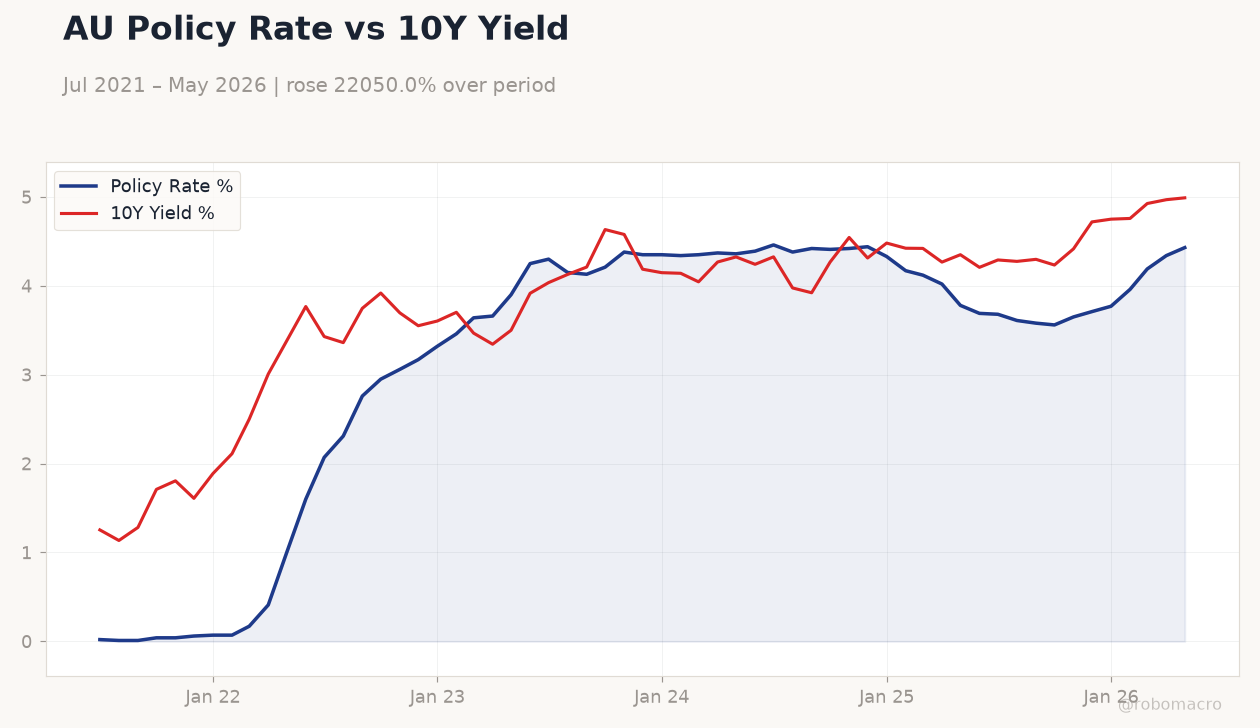

AU Policy Rate vs 10Y Yield | Type: macro_line | Policy Rate %: 4.43 (2026-05-01) | Range: 0.01–4.46 | Trend(6pt): 0.02,2.76,4.38,4.33,4.19,4.43 | 10Y Yield %: 4.99 (2026-05-01) | Range: 1.135–4.99 | Trend(6pt): 1.254,3.747,4.578,4.481,4.926,4.99

AU Policy Rate vs 10Y Yield | Type: macro_line | Policy Rate %: 4.43 (2026-05-01) | Range: 0.01–4.46 | Trend(6pt): 0.02,2.76,4.38,4.33,4.19,4.43 | 10Y Yield %: 4.99 (2026-05-01) | Range: 1.135–4.99 | Trend(6pt): 1.254,3.747,4.578,4.481,4.926,4.99

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Current Account Balance | -5,980m | -1,190m | 14:45 |

| RBA Jones Speech | - | - | 17:30 |

| GDP Growth Quarter-over-Quarter | 0.20 | 0.90 | 14:45 |

| GDP Growth Year-over-Year | 1.30 | 1.10 | 14:45 |

| Trade Balance | 1,920m | 875m | 14:45 |

- RBA kept the cash rate at 4.35% and flagged upside risks to inflation despite cooling growth signals.

- ASX 200 rose 1.25% while AUD/NZD climbed 0.25% as the RBA’s hawkish hold outpaced NZ data.

- NZ card spending accelerated in May, reinforcing RBNZ’s higher-for-longer stance ahead of Q2 GDP.

Yesterday's Recap

The RBA left the cash rate unchanged at 4.35% and warned that further hikes remain possible if inflation fails to moderate. Australian 10-year yields rose 0.42% to 4.99% on the hawkish tone. The ASX 200 gained 1.25% to 8,914 while BHP edged up 0.02%.

AUD/USD slipped 0.09% to 0.71 against a firmer USD, but AUD/NZD advanced 0.25% to 1.21 as NZD/USD fell 0.37%. NZX 50 added 0.49% to 13,426.13. Gold rose 0.70% while Brent crude dropped 4.14%.

NZ card retail sales growth accelerated in May, supporting expectations of a prolonged RBNZ pause.

The Day Ahead

NZ Current Account Balance prints at 14:45 ET today with consensus narrowing the deficit sharply. RBA’s Jones speaks at 17:30 ET, likely reiterating the cautious stance. Tomorrow NZ releases Q2 GDP, expected to show 0.9% q/q growth.

NZ Trade Balance follows on 18 June. Markets will watch for any fresh signals on RBA rate path divergence from the RBNZ.

Other Economic Notes

Australia’s commodity exports remain supported by iron-ore strength tied to China stimulus hopes, underpinning AUD resilience. Housing approvals have stabilised but credit growth stays modest amid high rates. NZ’s dairy-driven current account and tourism inflows continue to shape NZD sensitivity to global risk sentiment.

Both economies face China demand as the dominant external driver, with BHP serving as the key bellwether for Australian mining sentiment.

Global Macro News

Softer US inflation readings have eased global rate-hike fears, supporting risk assets and commodity prices relevant to ANZ. Chinese liquidity measures lifted iron-ore futures, directly aiding Australian export revenues and AUD. Brent’s sharp decline reduces NZ import costs but weighs on energy-related AUD flows.

Bitcoin’s 1.02% drop reflects broader risk-off moves that could pressure NZD more than AUD given NZ’s higher external financing needs. South Korean and Egyptian currency moves highlight ongoing EM volatility that indirectly affects ANZ carry-trade flows. Global bond yields remain elevated, capping further ANZ yield compression.