ANZ Macro Daily(Beta Mode)

RBA Holds at 4.35%, AUD Falls on Hawkish Pause

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,917.70 | +0.04% |

| NZX 50 | 13,392.98 | -0.25% |

| AUD/USD | 0.70 | -0.84% |

| NZD/USD | 0.58 | -1.06% |

| AUD/NZD | 1.22 | +0.20% |

| BHP | 65.59 | +0.61% |

| Gold | 4,259.60 | -1.65% |

| Brent Crude | 79.12 | +0.20% |

| Bitcoin | 64,181.07 | -2.16% |

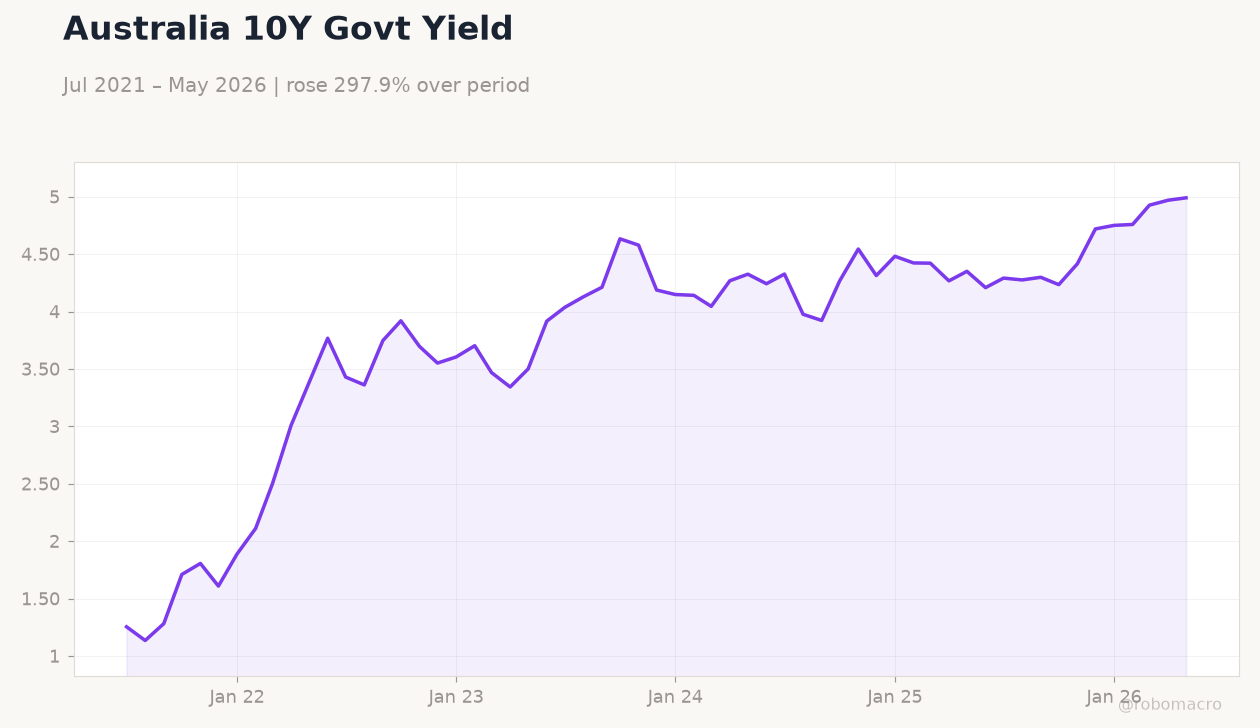

| Australia 10Y Govt Yield | 4.99% | +0.42% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

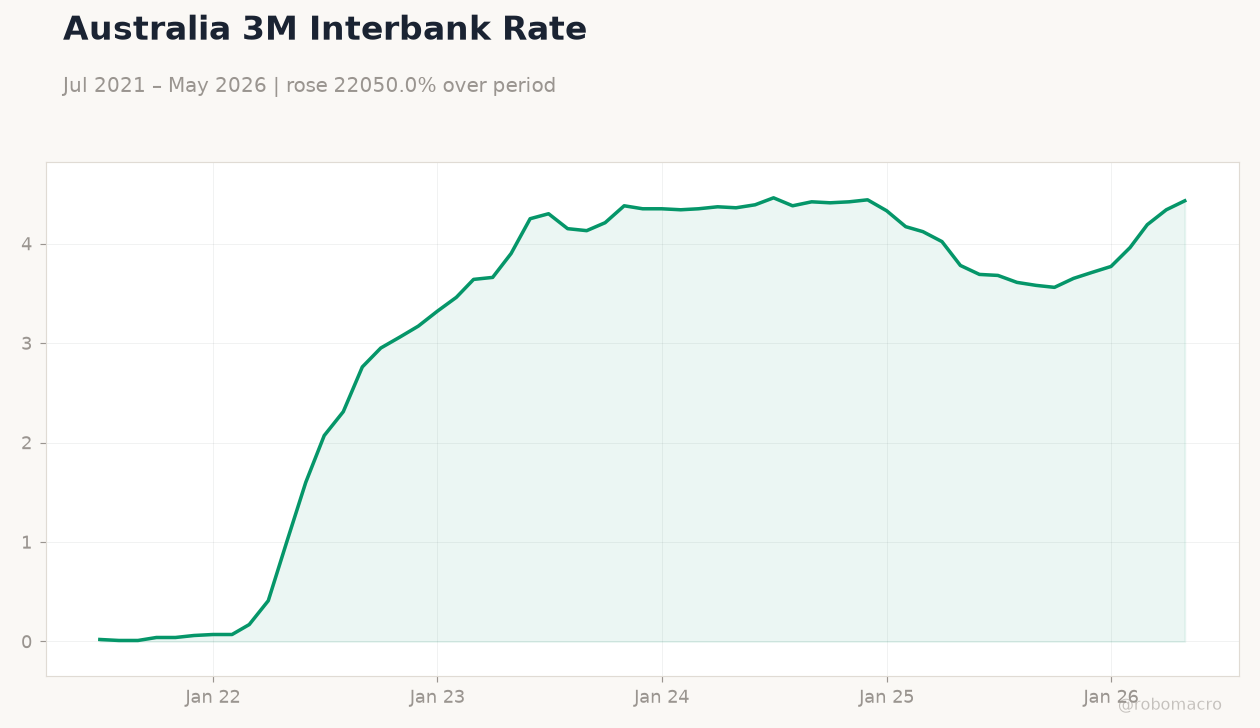

| RBA Interest Rate Decision | 4.35 | 4.35 | 4.35 |

| RBA Press Conference | - | - | - |

| Current Account Balance | -5,640m | -1,030m | -1,010m |

| RBA Jones Speech | - | - | - |

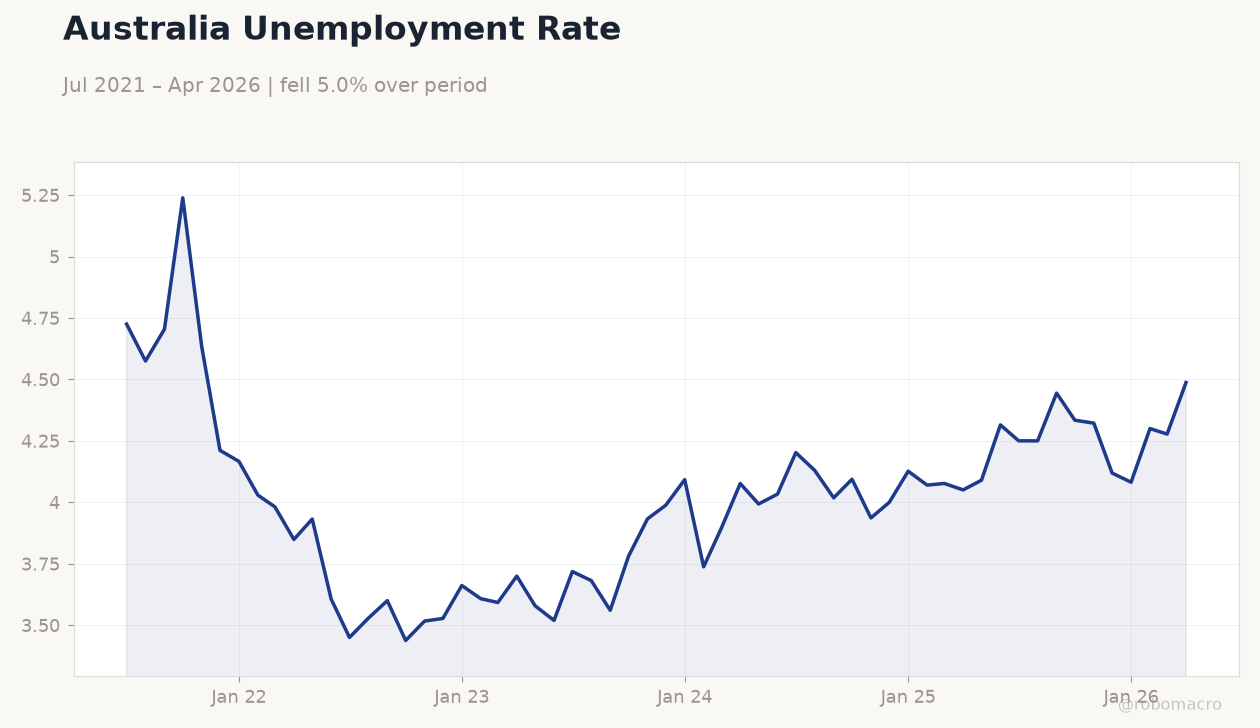

Australia Unemployment Rate | Type: macro_line | Percent: 4.488 (2026-04-01) | Range: 3.438–5.239 | Trend(6pt): 4.725,3.6,3.933,4.127,4.278,4.488

Australia Unemployment Rate | Type: macro_line | Percent: 4.488 (2026-04-01) | Range: 3.438–5.239 | Trend(6pt): 4.725,3.6,3.933,4.127,4.278,4.488

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| GDP Growth Quarter-over-Quarter | 0.20 | 0.90 | 14:45 |

| GDP Growth Year-over-Year | 1.30 | 1.10 | 14:45 |

| Trade Balance | 1,920m | 875m | 14:45 |

- RBA kept the cash rate at 4.35% and signalled further hikes remain possible despite slowing growth.

- NZ current account deficit narrowed to NZD -1.01 bn, beating consensus and supporting NZD relative to AUD.

- ASX 200 edged up 0.04% while AUD/USD dropped 0.84% to 0.70 on the RBA’s cautious stance.

Yesterday's Recap

The RBA held the cash rate at 4.35% and delivered a hawkish press conference that flagged upside risks to inflation. Governor Jones later reinforced that the board had not ruled out additional tightening. Australia’s 10-year government bond yield rose 0.42% to 4.99%.

The NZ current account deficit printed at NZD -1.01 bn, narrower than the NZD -1.03 bn consensus. NZ short-term rates fell 9.60% to 4.33%. AUD/USD fell 0.84% to 0.70 and NZD/USD dropped 1.06% to 0.58, pushing AUD/NZD up 0.20% to 1.22.

The ASX 200 gained 0.04% to 8,917.70 while the NZX 50 slipped 0.25% to 13,392.98. BHP rose 0.61% to 65.59 as iron-ore futures stayed firm. Gold fell 1.65% to 4,259.60 while Brent crude edged 0.20% higher to 79.12.

Bitcoin declined 2.16% to 64,181.07.

The Day Ahead

New Zealand will release Q2 GDP figures today, with quarter-on-quarter growth expected to rebound to 0.9% from 0.2%. Annual growth is forecast to ease to 1.1% from 1.3%. The NZ trade balance for May is also due tomorrow, with the surplus projected to narrow sharply to NZD 875 m from NZD 1.92 bn.

Markets will watch for any early signals on RBNZ policy ahead of the next OCR decision. No major Australian data releases are scheduled.

Other Economic Notes

Australia’s commodity exports remain supported by iron-ore and LNG demand from China, although recent stimulus signals have yet to lift volumes materially. Housing markets in both countries continue to show resilience, with dwelling prices holding near record levels and supporting household wealth. NZ’s dairy sector posted a modest GDT price gain last night, providing a small offset to softer tourism data.

Broader ANZ growth remains tied to China’s recovery trajectory and global commodity prices.