ANZ Macro Daily(Beta Mode)

RBA Holds Rate as NZ GDP Misses Forecast

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,966.30 | +0.54% |

| NZX 50 | 13,363.31 | -0.22% |

| AUD/USD | 0.70 | -0.71% |

| NZD/USD | 0.58 | -1.29% |

| AUD/NZD | 1.22 | +0.57% |

| BHP | 65.04 | -0.84% |

| Gold | 4,235.80 | -2.82% |

| Brent Crude | 79.51 | -0.05% |

| Bitcoin | 63,041.63 | -3.90% |

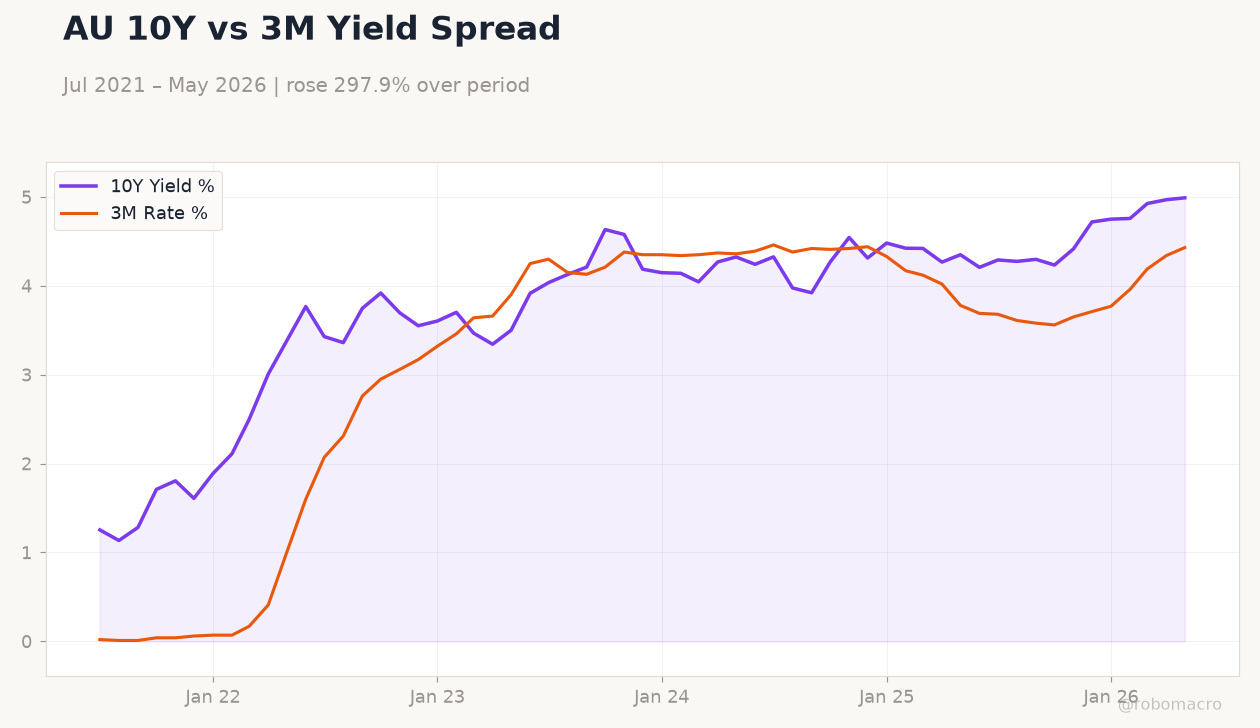

| Australia 10Y Govt Yield | 4.99% | +0.42% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| RBA Interest Rate Decision | 4.35 | 4.35 | 4.35 |

| RBA Press Conference | - | - | - |

| Current Account Balance | -5,640m | -1,030m | -1,010m |

| RBA Jones Speech | - | - | - |

| GDP Growth Quarter-over-Quarter | 0.50 | 0.90 | 0.80 |

| GDP Growth Year-over-Year | 1.50 | 1.10 | 1.50 |

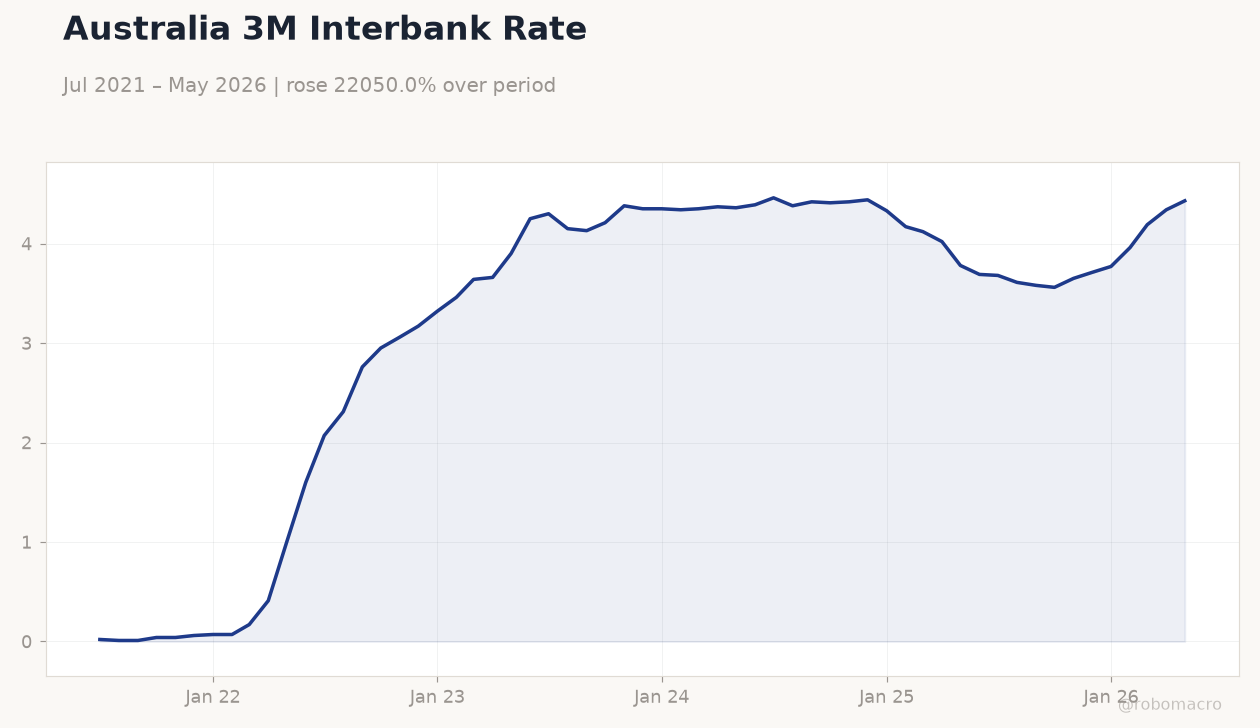

Australia 3M Interbank Rate | Type: macro_line | Rate %: 4.43 (2026-05-01) | Range: 0.01–4.46 | Trend(6pt): 0.02,2.76,4.38,4.33,4.19,4.43

Australia 3M Interbank Rate | Type: macro_line | Rate %: 4.43 (2026-05-01) | Range: 0.01–4.46 | Trend(6pt): 0.02,2.76,4.38,4.33,4.19,4.43

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Trade Balance | 1,920m | 875m | 14:45 |

- RBA holds cash rate at 4.31% as housing cools and inflation risks persist.

- NZ Q1 GDP rises 0.8% q/q while current account deficit narrows sharply.

- ASX 200 gains 0.54% but AUD/USD drops below 0.70 on Fed hawkishness.

Yesterday's Recap

The RBA left the cash rate unchanged at 4.31% and Governor Jones reiterated data dependence in the subsequent press conference and speech. Australian markets digested the hold with the ASX 200 advancing 0.54% to 8,966.30 while the 10-year government yield climbed 0.42% to 4.99%. In New Zealand, Q1 GDP expanded 0.8% q/q, slightly below consensus, and the current account deficit narrowed to NZD -1.01 billion.

The NZX 50 eased 0.22% to 13,363.31 and NZD/USD fell 1.29% to 0.58. AUD/NZD rose 0.57% to 1.22 as commodity prices offered limited support. BHP declined 0.84% despite firmer iron-ore futures, and bank stocks including Westpac and NAB fell on rate-uncertainty concerns.

The Day Ahead

New Zealand releases its May trade balance at 14:45 ET, with consensus pointing to a NZD 875 million surplus. Markets will monitor any revisions to prior months that could alter the external surplus narrative. Australian data are quiet, leaving focus on RBA communications and housing indicators already released.

China’s industrial production and retail sales figures tomorrow will provide the next external impulse for AUD and NZD. Local equity and currency traders remain attuned to Fed signals that continue to weigh on both currencies.

Other Economic Notes

Lower net migration is unlikely to ease Australia’s housing shortage given structural supply constraints and an ageing population. Bank equities face ongoing pressure from rate-hold expectations and potential margin compression. RBNZ consultations on revised crisis-management rules for deposit takers introduce regulatory uncertainty for New Zealand lenders.

Commodity export revenues remain the dominant swing factor for both economies, with China restocking activity the key variable.

Global Macro News

The Fed’s hawkish tilt pushed the dollar to multi-month highs, pressuring AUD/USD and NZD/USD. Yen weakness prompted fresh intervention warnings from Japanese officials, adding to global FX volatility. Brent crude held near US$79.51 while gold fell 2.82% to US$4,235.80, reflecting shifting safe-haven flows.

<i>↓ p.2</i>