ANZ Macro Daily(Beta Mode)

RBA Holds Rate, ASX Slides on Fed Caution

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,828.70 | -0.92% |

| NZX 50 | 13,495.63 | +0.99% |

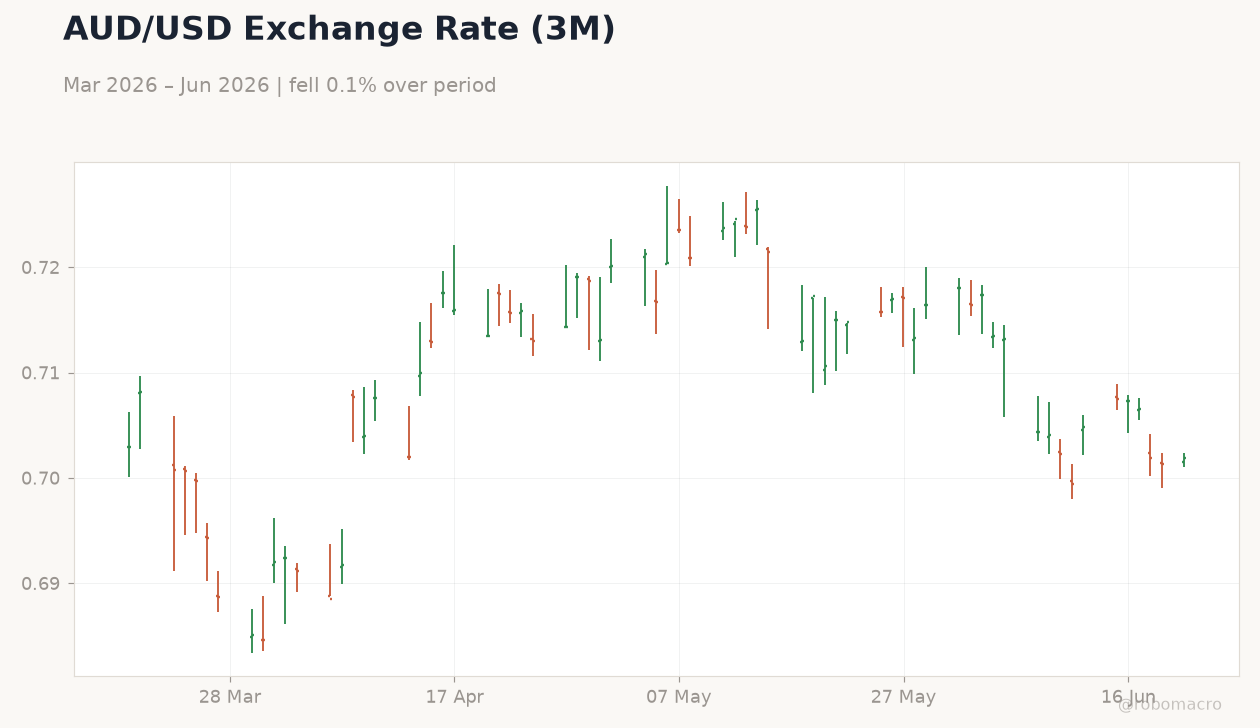

| AUD/USD | 0.70 | +0.01% |

| NZD/USD | 0.57 | -0.31% |

| AUD/NZD | 1.22 | +0.29% |

| BHP | 62.03 | -4.63% |

| Gold | 4,172.90 | -1.21% |

| Brent Crude | 80.59 | +0.93% |

| Bitcoin | 64,131.30 | -0.17% |

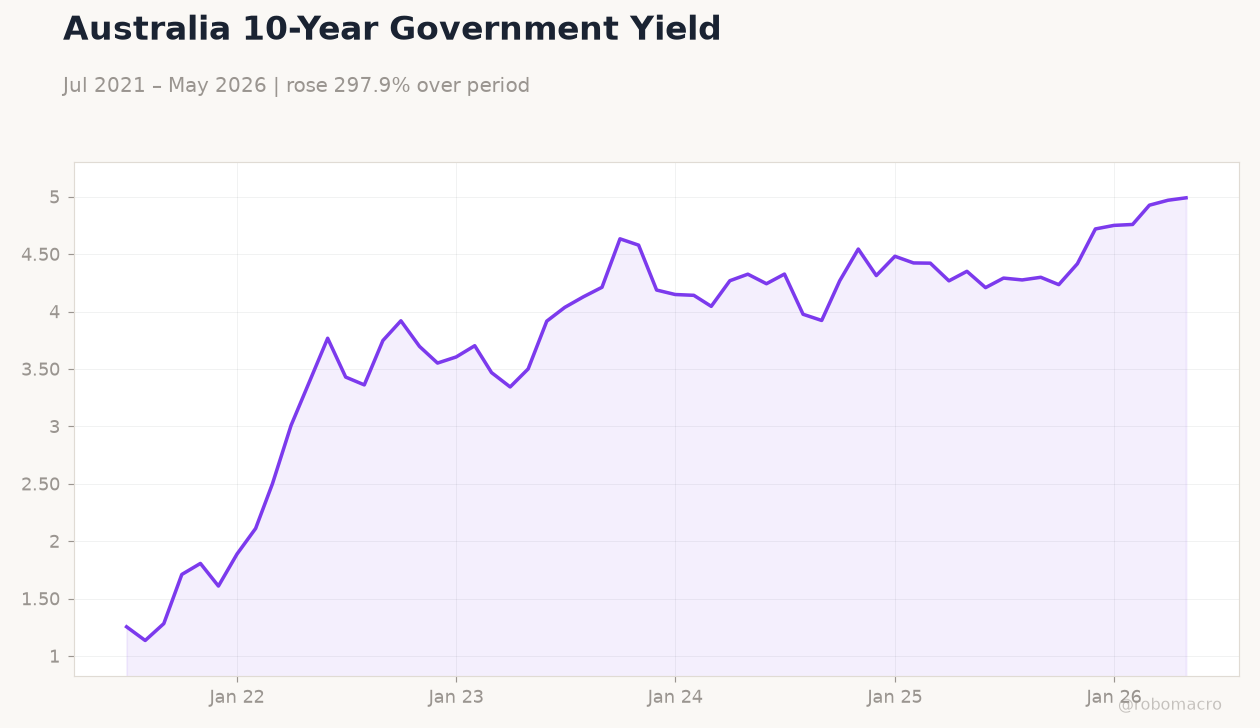

| Australia 10Y Govt Yield | 4.99% | +0.42% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

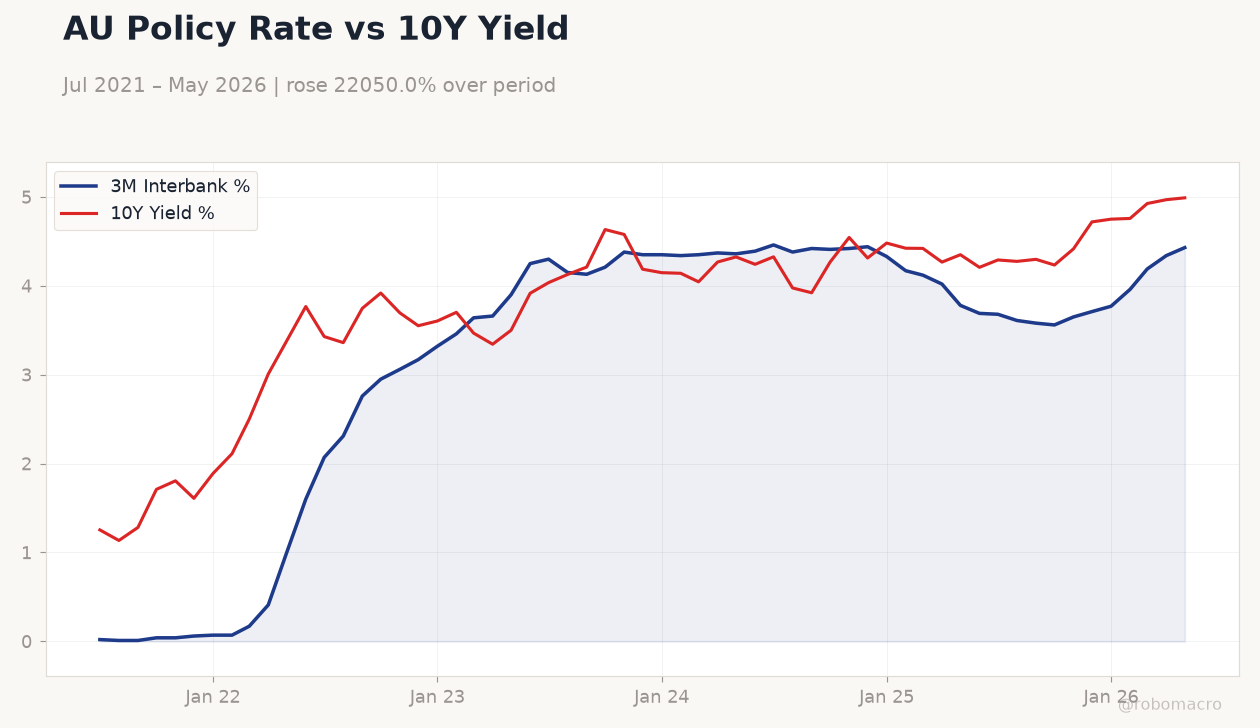

AU Policy Rate vs 10Y Yield | Type: macro_line | 3M Interbank %: 4.43 (2026-05-01) | Range: 0.01–4.46 | Trend(6pt): 0.02,2.76,4.38,4.33,4.19,4.43 | 10Y Yield %: 4.99 (2026-05-01) | Range: 1.135–4.99 | Trend(6pt): 1.254,3.747,4.578,4.481,4.926,4.99

AU Policy Rate vs 10Y Yield | Type: macro_line | 3M Interbank %: 4.43 (2026-05-01) | Range: 0.01–4.46 | Trend(6pt): 0.02,2.76,4.38,4.33,4.19,4.43 | 10Y Yield %: 4.99 (2026-05-01) | Range: 1.135–4.99 | Trend(6pt): 1.254,3.747,4.578,4.481,4.926,4.99

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| S&P Global Manufacturing PMI Flash | 50.70 | - | 19:00 |

| S&P Global Services PMI Flash | 48.70 | - | 19:00 |

| Inflation Rate Month-over-Month | 0.40 | -0.40 | 21:30 |

| Inflation Rate Year-over-Year | 4.20 | 4.30 | 21:30 |

| RBA Trimmed Mean CPI Month-over-Month | 0.30 | 0.30 | 21:30 |

| RBA Trimmed Mean CPI Year-over-Year | 3.40 | - | 21:30 |

| RBA Hauser Speech | - | - | 02:30 |

| Employment Change | -18,600 | 30,300 | 21:30 |

| Full-Time Employment Change | -10,700 | - | 21:30 |

| Headline Unemployment Rate | 4.50 | 4.40 | 21:30 |

- RBA kept the cash rate at 4.31% with guidance that further hikes remain possible if inflation persists.

- Australian equities fell while the NZX 50 advanced, reflecting divergent risk sentiment across the Tasman.

- AUD/USD held steady near 0.70 as hawkish Fed and RBA signals offset each other amid thin data flow.

Yesterday's Recap

No macroeconomic releases were published in Australia or New Zealand on 20 June. The ASX 200 declined 0.92% to 8,828.70, pressured by BHP’s 4.63% drop and warnings from US officials on Middle East tensions. The NZX 50 rose 0.99% to 13,495.63, supported by defensive names.

AUD/USD edged 0.01% higher to 0.70 while NZD/USD fell 0.31% to 0.57. Australia’s 10-year government bond yield climbed 0.42% to 4.99%. News flow centred on the RBA’s recent decision to hold rates steady at 4.31% and one major bank’s view that the tightening cycle has ended.

House-price forecasts showed potential 10% declines despite unchanged policy.

The Day Ahead

Australia releases S&P Global Manufacturing and Services PMI flashes at 19:00 ET on 22 June. CPI data and RBA trimmed-mean measures follow on 23 June, with markets expecting a 0.4% monthly decline and 4.3% annual rate. Employment figures on 24 June are projected to show a 30,300 gain and unemployment at 4.4%.

RBA Governor Bullock speaks on 28 June. No material New Zealand data are scheduled before month-end.

Other Economic Notes

Australia’s commodity exports remain the dominant AUD driver, with iron-ore prices sensitive to any fresh Chinese stimulus. New Zealand’s dairy and tourism receipts continue to lag, leaving the NZD more exposed to global risk sentiment. Housing markets in both countries face headwinds from elevated rates, though Australian price falls are now forecast even without further RBA tightening.

China’s credit data released overnight showed modest loan growth, offering limited support for ANZ terms of trade.

Global Macro News

The yen approached 40-year lows against the dollar despite verbal intervention, lifting USD funding costs for Australian banks. Sterling slipped after UK contraction data reinforced dollar strength. Korean won-dollar averages reached the highest levels since the financial crisis.

<i>↓ p.2</i>