ANZ Macro Daily(Beta Mode)

RBA Holds Amid Hawkish Signals and ASX Slide

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,828.70 | -0.92% |

| NZX 50 | 13,446.05 | -0.37% |

| AUD/USD | 0.70 | -0.15% |

| NZD/USD | 0.57 | -0.68% |

| AUD/NZD | 1.22 | +0.52% |

| BHP | 62.03 | -4.63% |

| Gold | 4,204.30 | -0.47% |

| Brent Crude | 78.32 | -1.92% |

| Bitcoin | 64,439.78 | +1.90% |

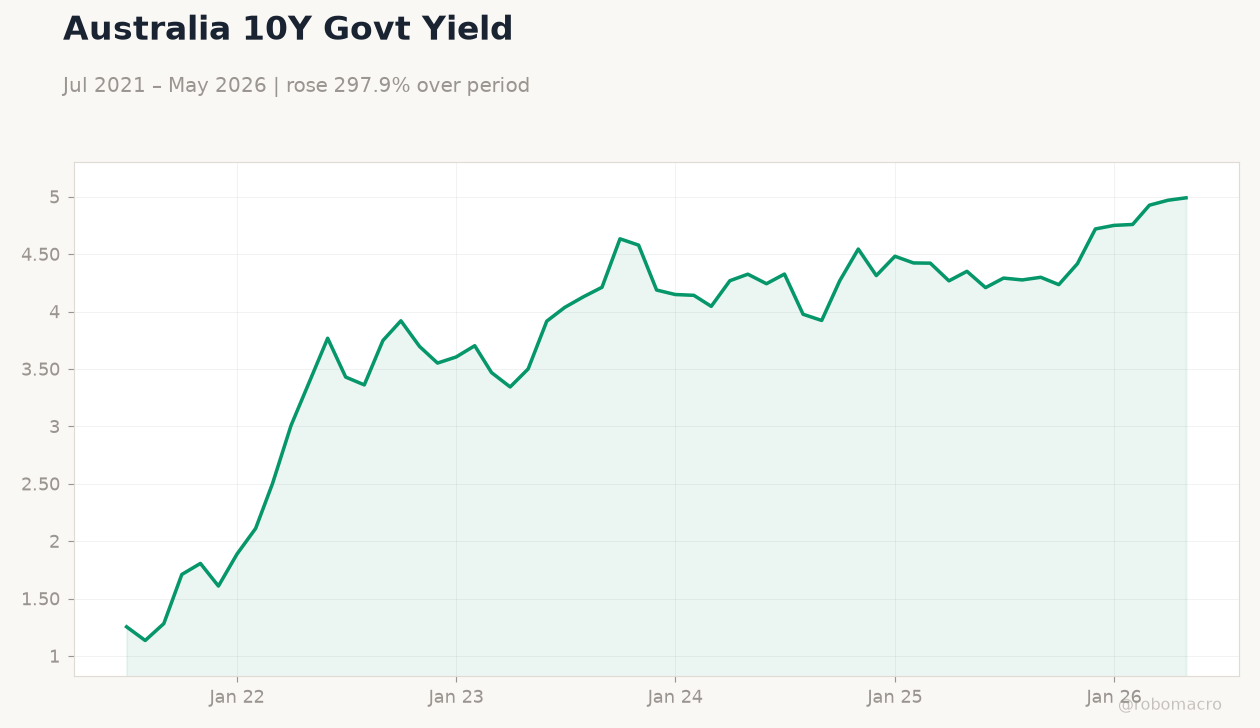

| Australia 10Y Govt Yield | 4.99% | +0.42% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

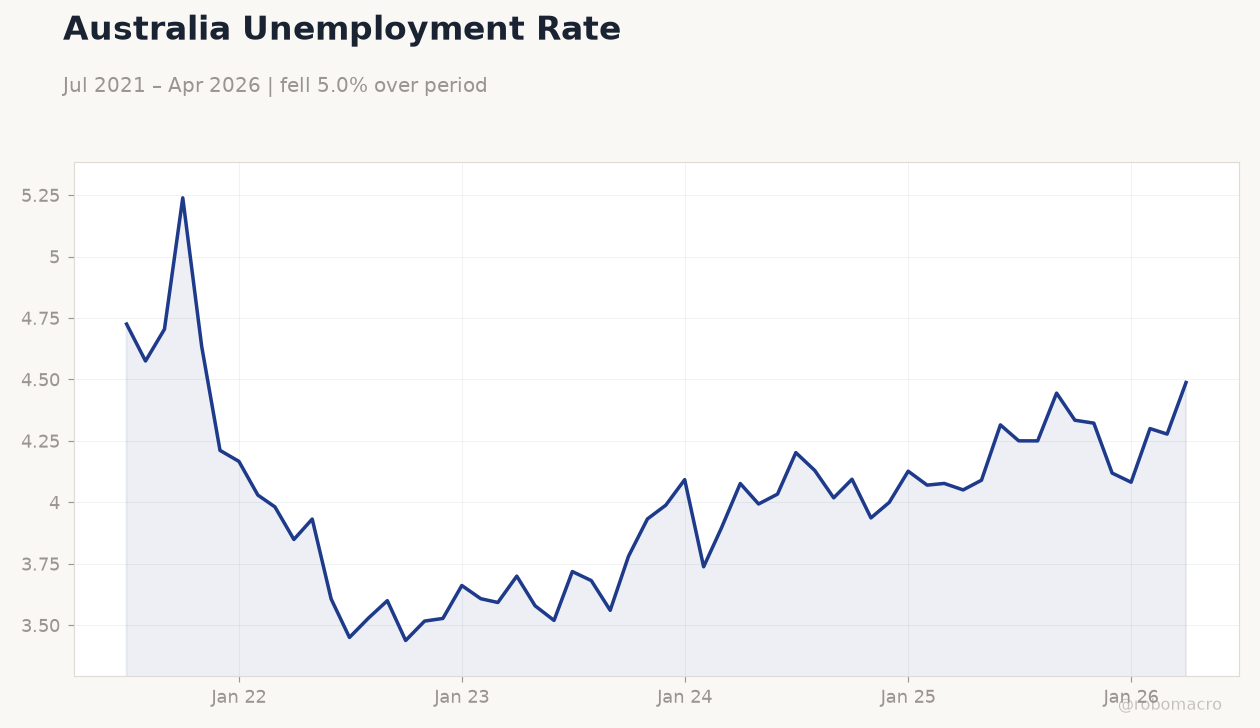

Australia Unemployment Rate | Type: macro_line | Percent: 4.488 (2026-04-01) | Range: 3.438–5.239 | Trend(6pt): 4.725,3.6,3.933,4.127,4.278,4.488

Australia Unemployment Rate | Type: macro_line | Percent: 4.488 (2026-04-01) | Range: 3.438–5.239 | Trend(6pt): 4.725,3.6,3.933,4.127,4.278,4.488

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| S&P Global Manufacturing PMI Flash | 50.70 | - | 15:00 |

| S&P Global Services PMI Flash | 48.70 | - | 15:00 |

| Inflation Rate Month-over-Month | 0.40 | -0.40 | 17:30 |

| Inflation Rate Year-over-Year | 4.20 | 4.30 | 17:30 |

| RBA Trimmed Mean CPI Month-over-Month | 0.30 | 0.30 | 17:30 |

| RBA Trimmed Mean CPI Year-over-Year | 3.40 | - | 17:30 |

| RBA Hauser Speech | - | - | 22:30 |

| Employment Change | -18,600 | 30,300 | 17:30 |

| Full-Time Employment Change | -10,700 | - | 17:30 |

| Headline Unemployment Rate | 4.50 | 4.40 | 17:30 |

- Australian PMIs due today with services sector still contracting while manufacturing holds near 50.

- RBA cash rate steady at 4.31% with committee keeping door open to further tightening amid persistent inflation.

- AUD/USD little changed near 0.70 as hawkish Fed and RBA outlooks offset each other; ASX 200 falls 0.92%.

Yesterday's Recap

Australian markets saw the ASX 200 drop 0.92% to 8,828.70, led by a 4.63% decline in BHP shares amid softer iron-ore sentiment. The NZX 50 eased 0.37% to 13,446.05 with limited local catalysts. AUD/USD traded little changed at 0.70 while NZD/USD fell 0.68% to 0.57.

Australian 10-year government yields rose 0.42% to 4.99% as investors priced in persistent RBA hawkishness. No major ANZ data releases occurred on 21 June, leaving price action driven by offshore flows and commodity moves. Brent crude slipped 1.92% to $78.32 per barrel, weighing on energy-related sentiment in Australia.

The Day Ahead

Australia releases S&P Global Manufacturing and Services PMI flashes at 15:00 ET today, with services expected to remain below 50. Tomorrow brings Australian inflation data including headline CPI and RBA trimmed-mean measures, with year-over-year CPI consensus at 4.3%. RBA Assistant Governor Hauser speaks at 22:30 ET tomorrow, likely reinforcing the bank’s data-dependent stance.

Employment figures follow on 24 June with unemployment rate consensus at 4.4%. Markets will also monitor any RBNZ commentary for signs of divergence from the RBA path.

Other Economic Notes

Australia’s commodity export base remains tightly linked to Chinese demand, with iron ore and LNG the dominant revenue drivers. Housing credit growth has slowed but prices continue to show resilience despite the 4.31% cash rate. New Zealand’s dairy sector faces softer GDT prices, pressuring the NZD and trade balance.

Both economies continue to feel the lagged effects of prior rate hikes through weaker consumption and slower credit expansion.

Global Macro News

The Fed’s hawkish tilt continues to support the USD, creating cross-currents for AUD and NZD carry trades. Yen weakness near 40-year lows has boosted AUD/JPY and supported Australian exporters with Japanese exposure. PBoC’s decision to hold rates steady provided modest support to AUD via improved risk sentiment toward China.

<i>↓ p.2</i>