ANZ Macro Daily(Beta Mode)

Aussie PMIs Beat Forecasts as AUD Slides on Fed Bets

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,816.10 | -0.14% |

| NZX 50 | 13,435.77 | -0.08% |

| AUD/USD | 0.69 | -1.26% |

| NZD/USD | 0.57 | -1.17% |

| AUD/NZD | 1.22 | -0.11% |

| BHP | 62.03 | -4.63% |

| Gold | 4,137.20 | -1.07% |

| Brent Crude | 77.14 | -0.98% |

| Bitcoin | 62,433.94 | -2.37% |

| Australia 10Y Govt Yield | 4.99% | +0.42% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| S&P Global Manufacturing PMI Flash | 50.70 | - | 51.20 |

| S&P Global Services PMI Flash | 48.70 | - | 49.90 |

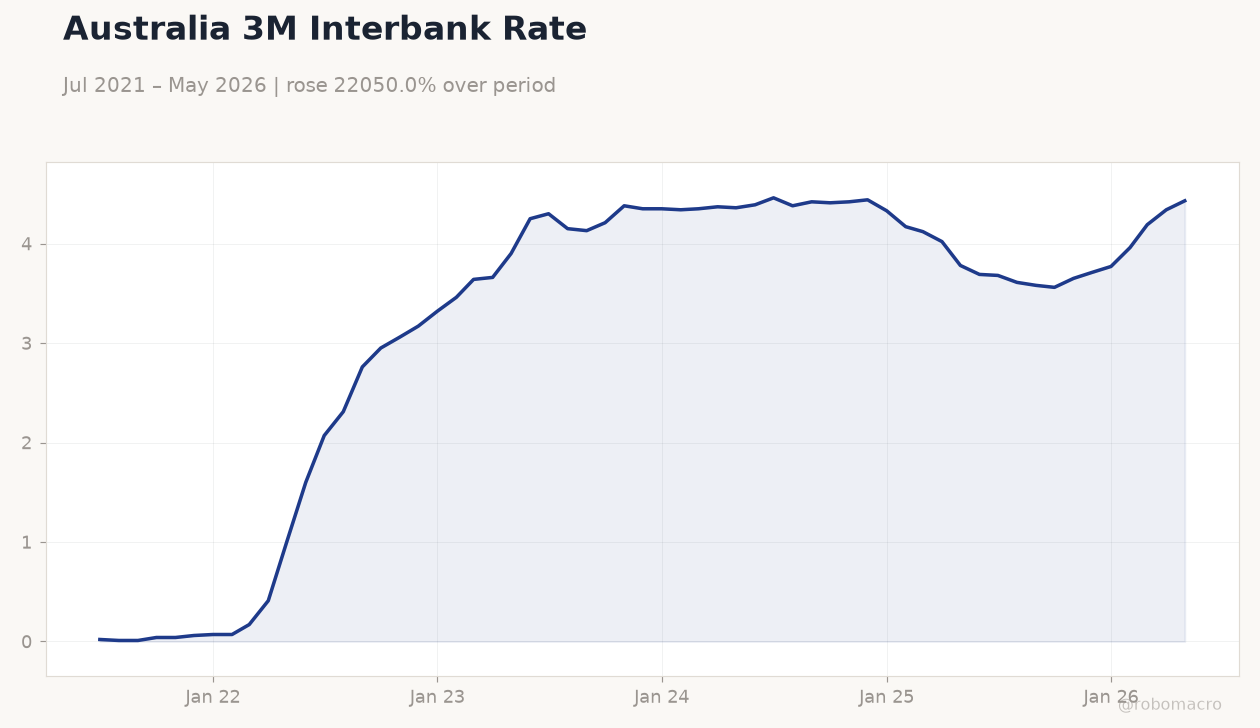

Australia 3M Interbank Rate | Type: macro_line | Policy Rate %: 4.43 (2026-05-01) | Range: 0.01–4.46 | Trend(6pt): 0.02,2.76,4.38,4.33,4.19,4.43

Australia 3M Interbank Rate | Type: macro_line | Policy Rate %: 4.43 (2026-05-01) | Range: 0.01–4.46 | Trend(6pt): 0.02,2.76,4.38,4.33,4.19,4.43

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Inflation Rate Month-over-Month | 0.40 | -0.30 | 17:30 |

| Inflation Rate Year-over-Year | 4.20 | 4.40 | 17:30 |

| RBA Trimmed Mean CPI Month-over-Month | 0.30 | 0.30 | 17:30 |

| RBA Trimmed Mean CPI Year-over-Year | 3.40 | 3.50 | 17:30 |

| RBA Hauser Speech | - | - | 22:30 |

| Employment Change | -18,600 | 25,000 | 17:30 |

| Full-Time Employment Change | -10,700 | - | 17:30 |

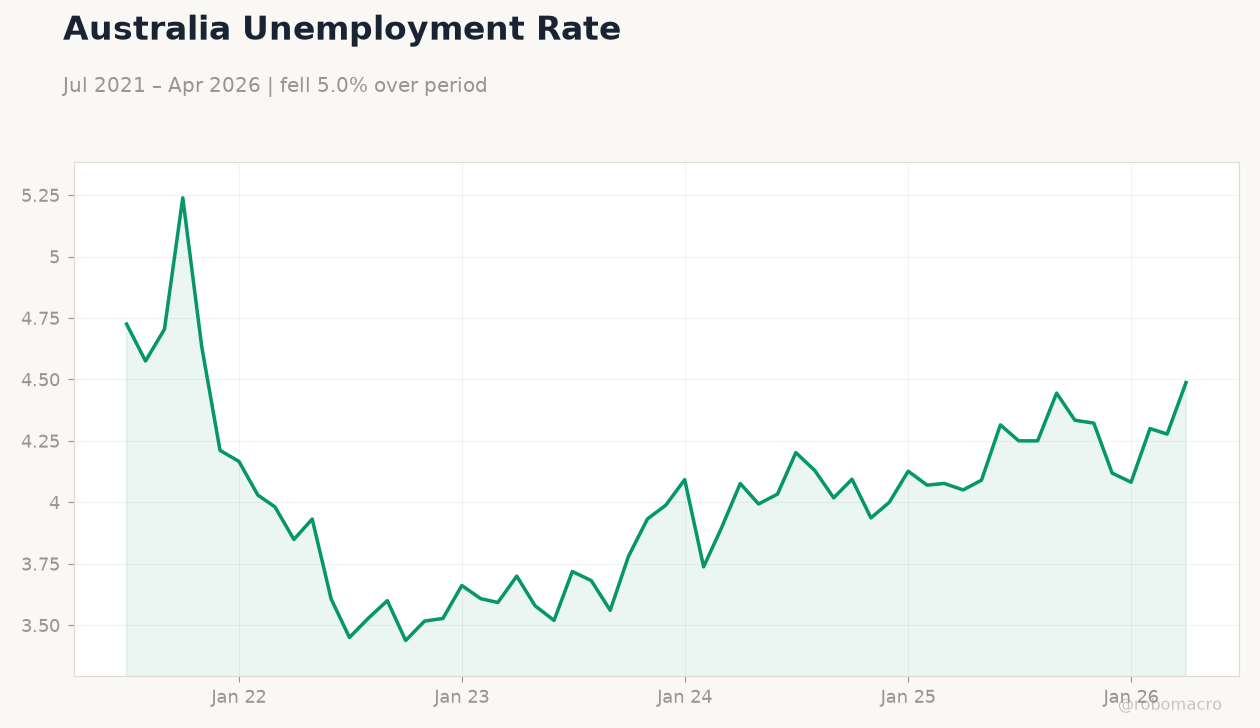

| Headline Unemployment Rate | 4.50 | 4.40 | 17:30 |

| RBA Gov Bullock Speech | - | - | 04:15 |

- Australian manufacturing and services PMIs both beat expectations in June, signaling modest expansion.

- AUD/USD fell below 0.70 as USD strengthened on Fed rate repricing, while ASX 200 edged down 0.14%.

- RBA maintains cash rate at 4.31% with committee keeping door open to further hikes amid persistent inflation.

Yesterday's Recap

Australian S&P Global manufacturing PMI rose to 51.2 from 50.7 while services PMI climbed to 49.9 from 48.7, both released at 15:00 ET on 22 June. Equity markets closed modestly lower with ASX 200 at 8,816.10, down 0.14%, and NZX 50 at 13,435.77, down 0.08%. AUD/USD dropped 1.26% to 0.69 and NZD/USD fell 1.17% to 0.57 amid broad USD strength.

Australian 10-year yields rose 0.42% to 4.99% while NZ short-term rates eased 9.60% to 4.33%. BHP shares declined 4.63% to 62.03, weighing on the broader index. Commodity prices also softened with gold down 1.07% and Brent crude off 0.98%.

News flow highlighted lingering RBA rate-rise bets supporting the Aussie dollar even as Fed repricing lifted the greenback. PBoC’s steady policy stance offered limited cross-rate relief for AUD/JPY.

The Day Ahead

Australian monthly CPI and trimmed-mean measures are due at 17:30 ET on 23 June, with year-over-year headline expected at 4.4% and trimmed-mean at 3.5%. RBA Assistant Governor Hauser will speak at 22:30 ET, likely addressing inflation persistence. Employment data follow on 24 June, including change in jobs and unemployment rate.

RBA Governor Bullock is scheduled to speak on 28 June. Markets will monitor any signals on the timing of potential rate adjustments.

Other Economic Notes

Australia’s commodity export profile continues to link growth directly to Chinese industrial demand, with iron ore and LNG remaining key revenue drivers. Housing markets in both countries stay sensitive to rate expectations, supporting household wealth but also exposing banks to credit risk. NZ’s dairy and tourism sectors provide a narrower growth base than Australia’s diversified mining and energy exports.

Persistent services inflation in Australia keeps pressure on the RBA to avoid premature easing.

Global Macro News

USD strength intensified on repriced Fed hike probabilities, pushing AUD/USD below 0.7000 and pressuring both ANZ currencies. Yen weakness near multi-decade lows reflected similar global rate differentials and safe-haven flows. <i>↓ p.2</i>