ANZ Macro Daily(Beta Mode)

Australia CPI Cools, Core Rises; AUD Slides

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,787.00 | -0.33% |

| NZX 50 | 13,400.66 | -0.26% |

| AUD/USD | 0.69 | -1.44% |

| NZD/USD | 0.56 | -1.17% |

| AUD/NZD | 1.22 | -0.29% |

| BHP | 62.03 | -4.63% |

| Gold | 3,999.10 | -3.17% |

| Brent Crude | 73.35 | -4.84% |

| Bitcoin | 59,926.08 | -4.38% |

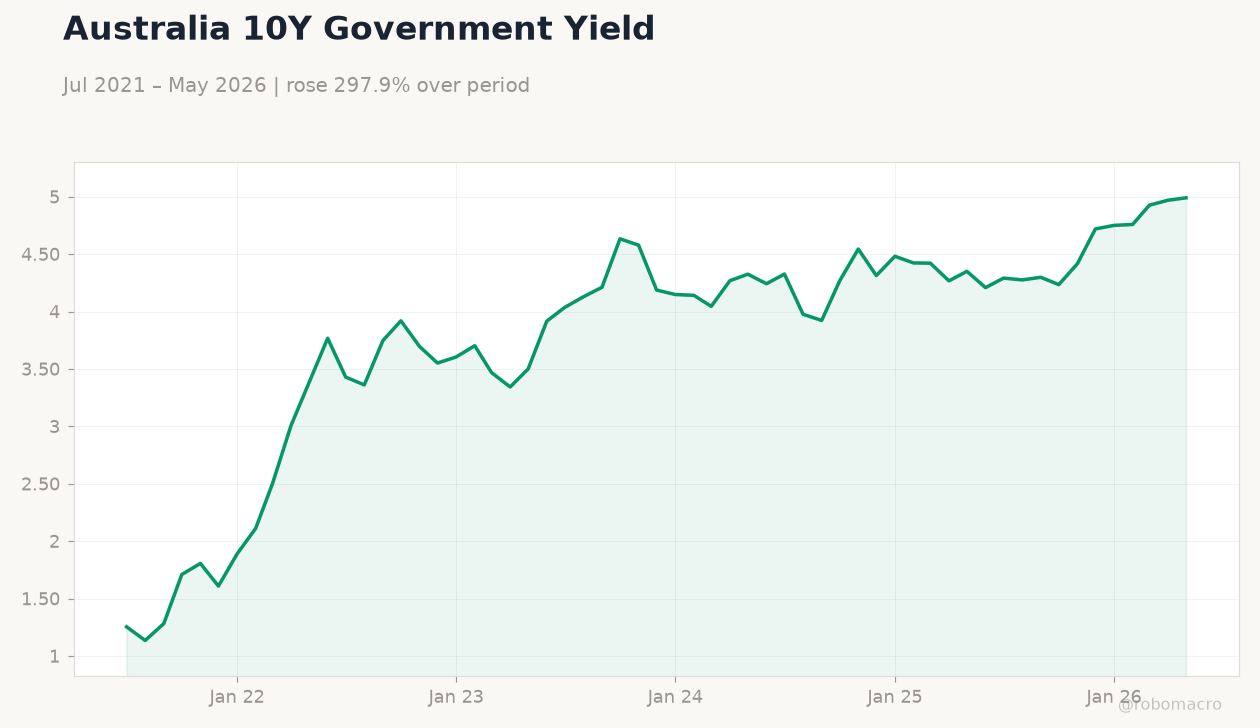

| Australia 10Y Govt Yield | 4.99% | +0.42% |

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| S&P Global Manufacturing PMI Flash | 50.70 | - | 51.20 |

| S&P Global Services PMI Flash | 48.70 | - | 49.90 |

| Inflation Rate Month-over-Month | 0.40 | -0.30 | -0.70 |

| Inflation Rate Year-over-Year | 4.20 | 4.40 | 4 |

| RBA Trimmed Mean CPI Month-over-Month | 0.30 | 0.30 | 0.40 |

| RBA Trimmed Mean CPI Year-over-Year | 3.40 | 3.50 | 3.60 |

| RBA Hauser Speech | - | - | - |

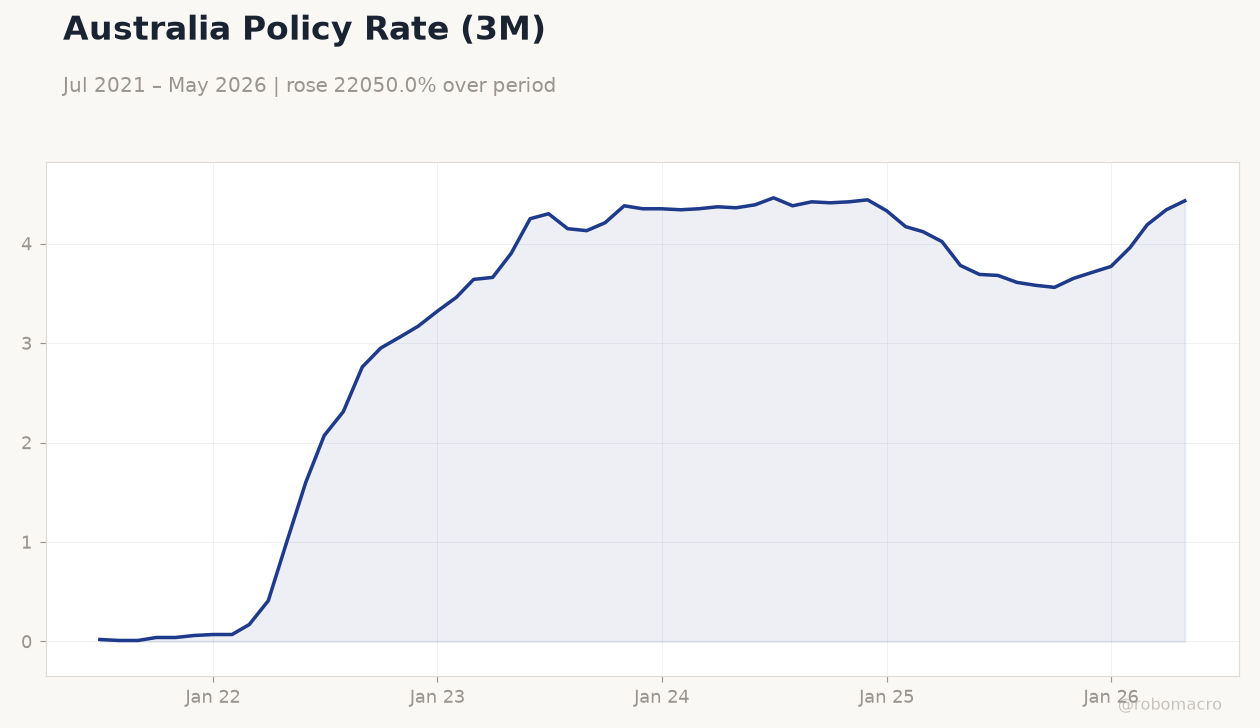

Australia Policy Rate (3M) | Type: macro_line | Interest Rate %: 4.43 (2026-05-01) | Range: 0.01–4.46 | Trend(6pt): 0.02,2.76,4.38,4.33,4.19,4.43

Australia Policy Rate (3M) | Type: macro_line | Interest Rate %: 4.43 (2026-05-01) | Range: 0.01–4.46 | Trend(6pt): 0.02,2.76,4.38,4.33,4.19,4.43

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Employment Change | -18,600 | 25,000 | 17:30 |

| Full-Time Employment Change | -10,700 | - | 17:30 |

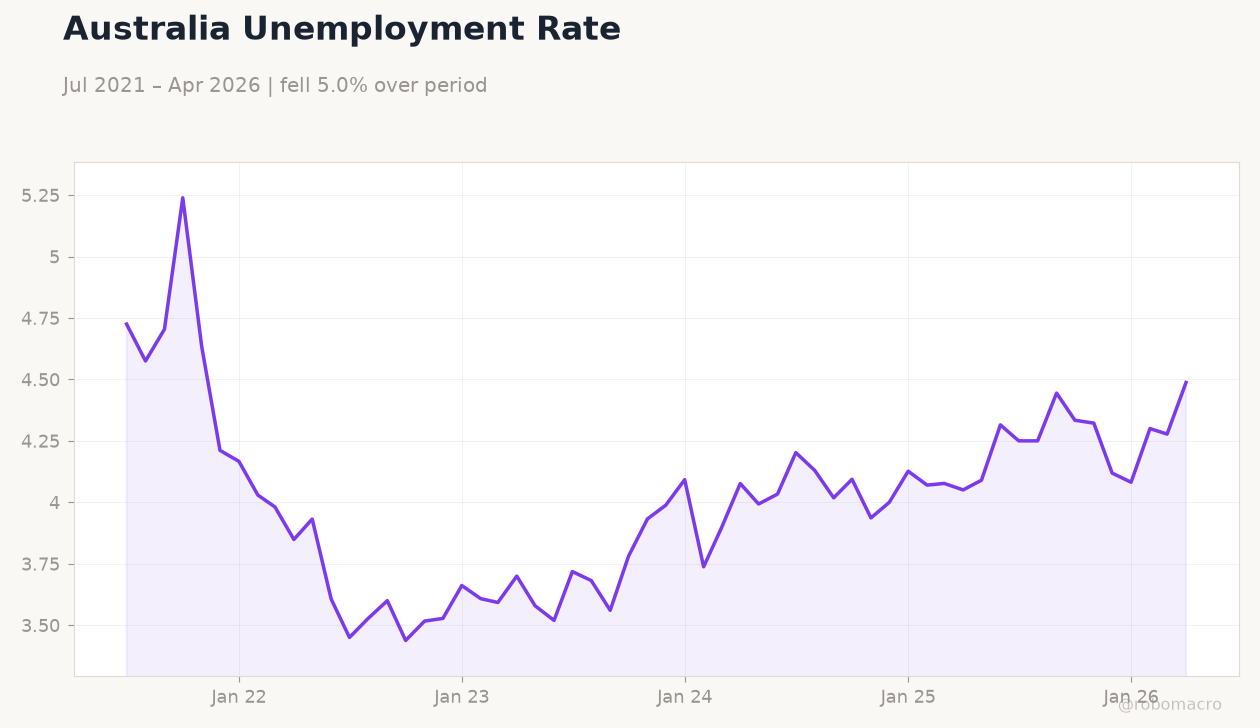

| Headline Unemployment Rate | 4.50 | 4.40 | 17:30 |

| RBA Gov Bullock Speech | - | - | 04:15 |

- Australia’s May headline CPI fell to 4.0% YoY while trimmed-mean inflation rose to 3.6% YoY, keeping RBA hike risks alive.

- ASX 200 fell 0.33% and AUD/USD dropped 1.44% to 0.69 as markets priced higher policy rates.

- Employment data due today will test labour-market strength ahead of potential RBA tightening.

Yesterday's Recap

Australian S&P Global manufacturing PMI rose to 51.2 and services PMI climbed to 49.9, signalling modest expansion. Headline CPI printed at -0.7% MoM and 4.0% YoY, both below consensus, yet RBA trimmed-mean measures lifted to 0.4% MoM and 3.6% YoY. RBA’s Hauser speech reinforced a resilient jobs market despite recent rate pressure.

ASX 200 closed 0.33% lower at 8,787 while NZX 50 slipped 0.26% to 13,400.66. AUD/USD plunged 1.44% to 0.69 and NZD/USD fell 1.17% to 0.56 amid higher Australian yields. The 10-year Australian government bond yield jumped 42 bp to 4.99%.

BHP shares dropped 4.63% to 62.03, tracking weaker commodity prices.

The Day Ahead

Australia releases May employment change, full-time jobs and unemployment rate at 17:30 ET, with markets expecting a 25k rebound in payrolls. RBA Governor Bullock speaks on 28 June, likely clarifying the inflation outlook. No major New Zealand data are scheduled until late next week.

China’s June industrial profits and PMI releases later in the month will influence commodity-linked AUD and NZD flows. Traders will monitor any reaction to today’s labour print for clues on RBA timing.

Other Economic Notes

Australia’s core inflation at 3.6% YoY keeps the RBA’s 4.31% cash rate under review for possible further hikes. Commodity exports remain the dominant growth driver, yet softer iron-ore and gold prices weighed on mining equities. New Zealand’s dairy and tourism sectors face headwinds from weaker global demand and a stronger USD.

Housing markets in both countries stay sensitive to any additional rate increases, with mortgage rates already elevated.

Global Macro News

The US dollar climbed to 13-month highs on bets for further Fed hikes, pressuring AUD and NZD. Yen hovered near 40-year lows, prompting intervention warnings from Japanese officials that could indirectly support risk sentiment. Brent crude fell 4.84% to 73.35 amid demand concerns, hurting Australia’s LNG and coal revenues.

Bitcoin dropped 4.38% to 59,926, reflecting broader risk-off flows. <i>↓ p.2</i>