ANZ Macro Daily(Beta Mode)

Australian Jobs Rebound Offsets CPI Miss

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| ASX 200 | 8,808.40 | +0.24% |

| NZX 50 | 13,493.05 | +0.69% |

| AUD/USD | 0.69 | -0.01% |

| NZD/USD | 0.57 | -0.24% |

| AUD/NZD | 1.22 | +0.22% |

| BHP | 59.50 | -0.70% |

| Gold | 4,037.90 | +1.19% |

| Brent Crude | 75.52 | +2.41% |

| Bitcoin | 59,468.00 | -2.50% |

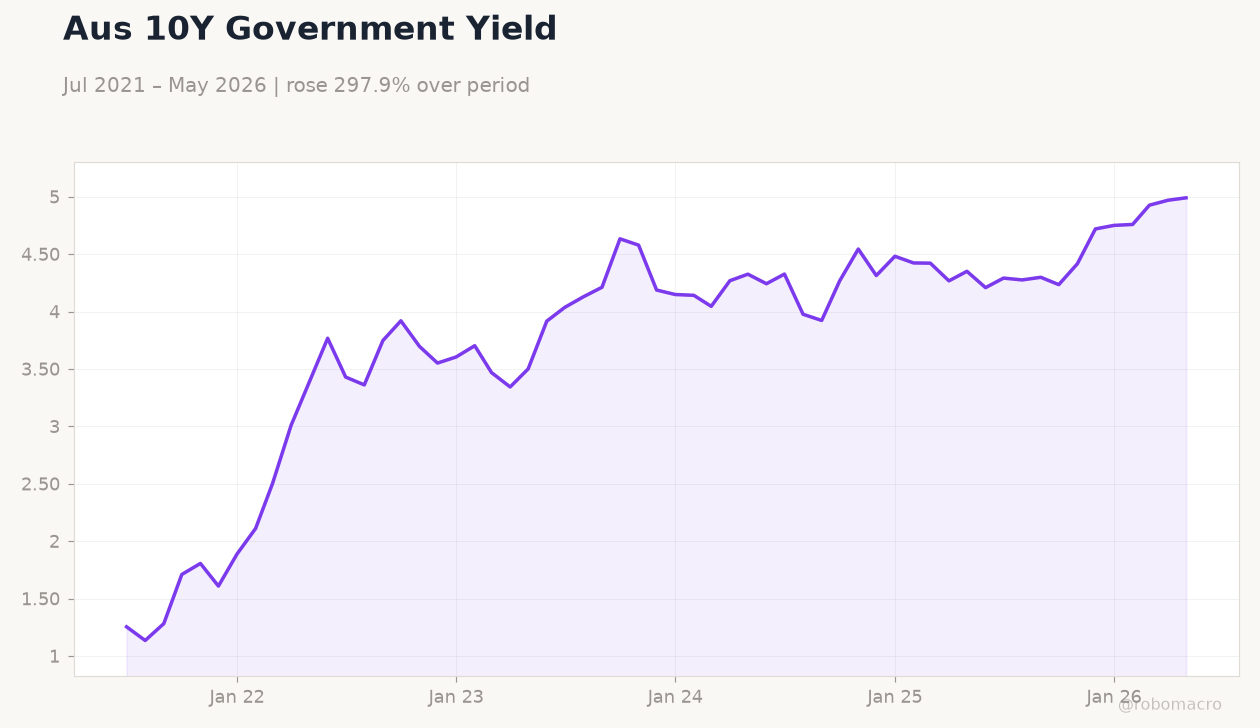

| Australia 10Y Govt Yield | 4.99% | +0.42% |

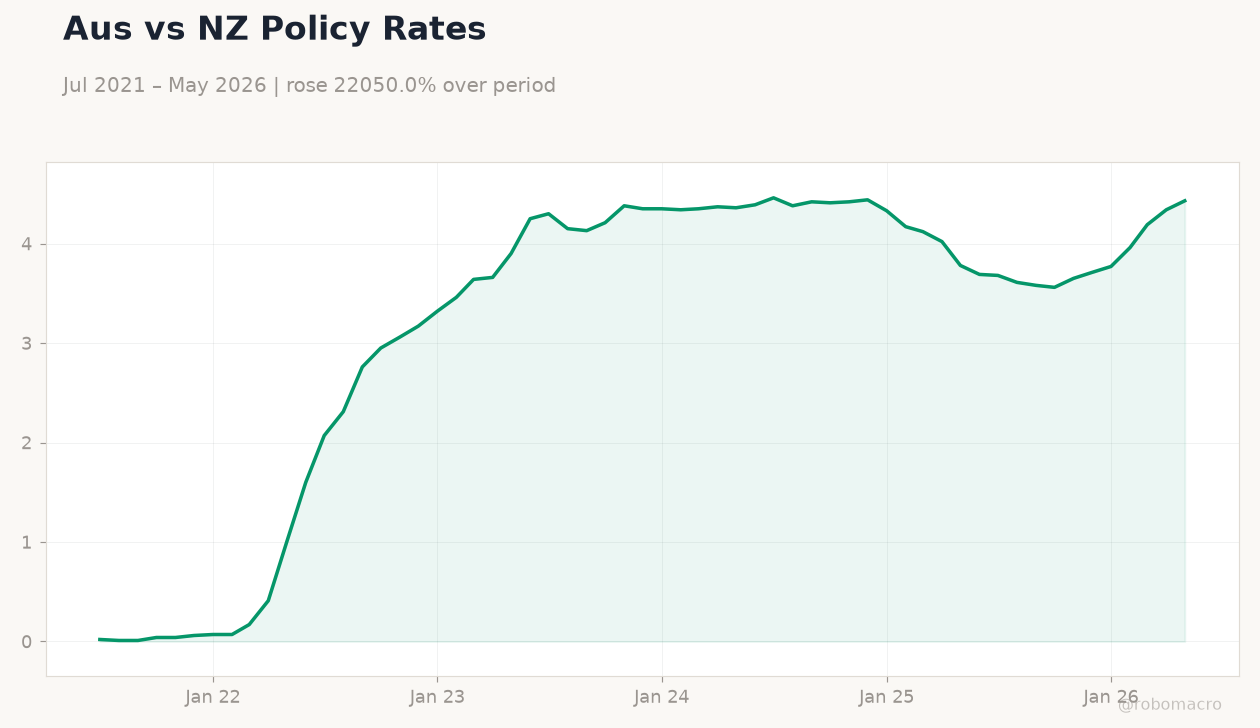

| NZ Short-term Rate | 4.33% | -9.60% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| S&P Global Manufacturing PMI Flash | 50.70 | - | 51.20 |

| S&P Global Services PMI Flash | 48.70 | - | 49.90 |

| Inflation Rate Month-over-Month | 0.40 | -0.30 | -0.70 |

| Inflation Rate Year-over-Year | 4.20 | 4.40 | 4 |

| RBA Trimmed Mean CPI Month-over-Month | 0.30 | 0.30 | 0.40 |

| RBA Trimmed Mean CPI Year-over-Year | 3.40 | 3.50 | 3.60 |

| RBA Hauser Speech | - | - | - |

| Employment Change | -40,700 | 30,000 | 40,300 |

| Full-Time Employment Change | -21,700 | - | 5,200 |

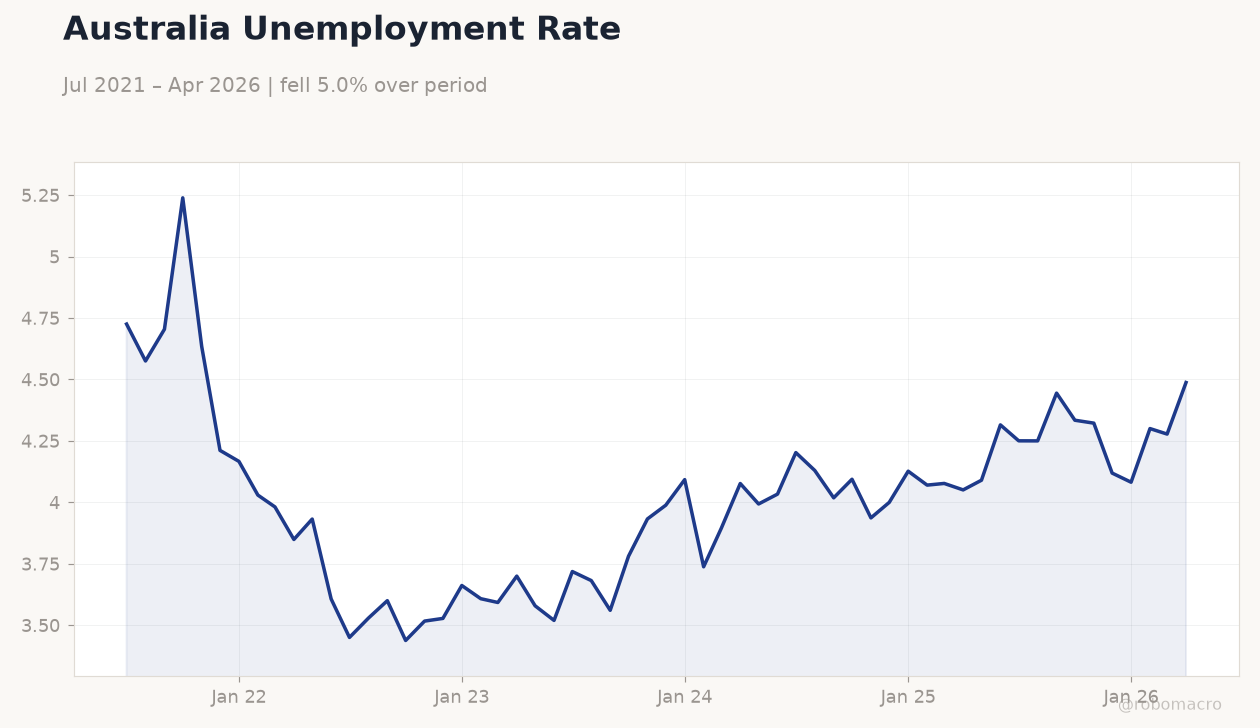

| Headline Unemployment Rate | 4.50 | 4.40 | 4.40 |

Australia Unemployment Rate | Type: macro_line | Unemployment %: 4.488 (2026-04-01) | Range: 3.438–5.239 | Trend(6pt): 4.725,3.6,3.933,4.127,4.278,4.488

Australia Unemployment Rate | Type: macro_line | Unemployment %: 4.488 (2026-04-01) | Range: 3.438–5.239 | Trend(6pt): 4.725,3.6,3.933,4.127,4.278,4.488

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| RBA Gov Bullock Speech | - | - | 04:15 |

- Australian employment surged 40,300 in May while unemployment held at 4.4%, tempering RBA easing bets despite softer headline CPI.

- Core trimmed-mean inflation rose to 3.6% y/y, keeping underlying price pressures elevated and supporting the 4.31% cash rate.

- ASX 200 gained 0.24% and AUD/USD steadied near 0.69 as commodity prices lifted on China stimulus hopes.

Yesterday's Recap

Australian S&P Global manufacturing PMI rose to 51.2 and services PMI climbed to 49.9 in June, signalling improving activity. May headline CPI fell 0.7% m/m and 4.0% y/y, missing consensus, while RBA trimmed-mean CPI edged up to 3.6% y/y. Employment rebounded sharply with a 40,300 gain and full-time jobs adding 5,200, leaving the unemployment rate at 4.4%.

The RBA Hauser speech offered no new policy signals. ASX 200 closed 0.24% higher at 8,808.40 while NZX 50 rose 0.69%. AUD/USD eased 0.01% to 0.69 and the 10-year government yield climbed 0.42% to 4.99%.

BHP fell 0.70% despite firmer iron-ore futures. Gold rose 1.19% to 4,037.90 and Brent crude gained 2.41% to 75.52.

The Day Ahead

RBA Governor Bullock speaks on 28 June, with markets watching for any shift in the hawkish tone. No major Australian or New Zealand data releases are scheduled for 26 June. Focus will remain on upcoming China industrial production figures due later in the week.

Traders will also monitor commodity price moves for further AUD and NZD direction. Housing credit and retail sales trends in New Zealand continue to signal softer momentum.

Other Economic Notes

Australia’s commodity export base continues to benefit from iron-ore and gold price gains linked to China policy expectations. New Zealand’s dairy auction results provided modest NZD support but retail sales weakness highlights divergent growth paths. Both economies remain sensitive to global risk sentiment and USD strength.

China demand remains the dominant external driver for ANZ trade balances.

Global Macro News

The US dollar reached a 13-month high on bets for further Fed rate hikes, pressuring AUD and NZD. Brent crude rose 2.41% to 75.52, adding to imported inflation concerns for both countries. Gold climbed 1.19% to 4,037.90, reinforcing Australia’s terms-of-trade advantage.

Bitcoin fell 2.50%, reflecting broader risk-off flows. Yen strength on intervention fears weighed on AUD/JPY cross rates. <i>↓ p.2</i>