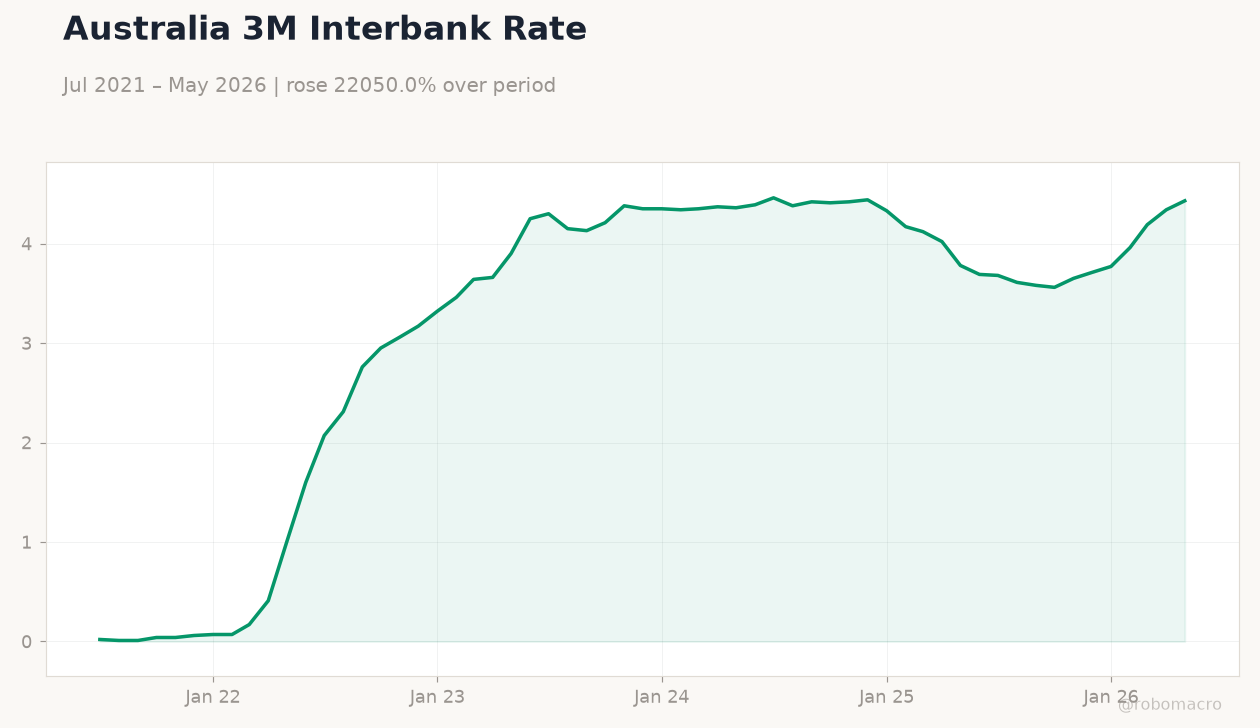

Yesterday's Recap

Australian S&P Global manufacturing PMI flash rose to 51.2 and services PMI improved to 49.9, pointing to modest expansion. Inflation data showed headline YoY falling to 4.0% against 4.4% consensus while MoM printed -0.7%, though RBA trimmed mean CPI edged up to 3.6% YoY. Employment change beat forecasts with a 40,300 gain and unemployment held at 4.4%.

RBA Governor Bullock and Hauser speeches reinforced data-dependent policy. ASX 200 advanced 0.18% to 8,764.20 while AUD/USD lifted 0.01% to 0.69. NZX 50 edged 0.02% higher and NZD/USD slipped 0.01% to 0.56.

Gold rose 1.63% and Brent crude fell 3.53%, reflecting softer energy prices. Australia's commodity exports continue to anchor the external balance, with iron ore and gold providing support despite softer Brent prices. Housing markets in both countries remain sensitive to rate paths, with cooling inflation potentially easing pressure on mortgage holders.

China demand outlook stays the dominant external variable for Australian miners including BHP and New Zealand dairy exporters. Broader risk-off moves lifted the US dollar and capped AUD/NZD gains near 1.22. US inflation data and potential Fed hike risks weighed on risk assets and supported the dollar, pressuring AUD/USD.

IMF commentary highlighted the dollar-centered global economy, limiting upside for commodity currencies. Lower crude prices eased some rate-hike concerns but added to volatility in energy-linked trades. Yen intervention fears kept Asian FX markets cautious and indirectly supported safe-haven flows into gold.

New Zealand dollar faces headwinds from subdued growth and RBNZ hold expectations. Overall global backdrop points to continued caution for ANZ currencies in the third quarter.

The Day Ahead

RBA Governor Bullock delivers a high-impact speech today that markets will parse for any shift in guidance. No major data releases are scheduled for Australia or New Zealand over the next two days. Focus will remain on external drivers including China PMI prints and global commodity trends.

<i>↓ p.2</i>

Australia 10Y Government Yield | Type: macro_line | Yield (%): 4.99 (2026-05-01) | Range: 1.135–4.99 | Trend(6pt): 1.254,3.747,4.578,4.481,4.926,4.99

Australia 10Y Government Yield | Type: macro_line | Yield (%): 4.99 (2026-05-01) | Range: 1.135–4.99 | Trend(6pt): 1.254,3.747,4.578,4.481,4.926,4.99